Let’s mention about various risks in the market. Including long term risks:

- With BTC declines coming from BTC ETFs and reaching a point where the majority of ETFs bought will be in the negative, which could trigger a panic sell-off.

- Risk coming from Strategy. Since Strategy owns ~$43.3 billion worth of BTC and they are constantly issuing bonds to buy new BTC. And that there may come a point where they can’t service the debt. Will there be a liquidation or a big sale of assets?

It is the risk of Strategy that will be discussed in this post. How real is it? We will also touch on the real mechanics of Strategy’s business, as they try to present themselves as BTC fanatics, but there are many things that do not add up.

What is Strategy?

Strategy, formerly known as MicroStrategy, is a US-based technology company that has dramatically changed its profile in recent years. Founded in 1989 by Michael Saylor, the company originally specialized in business intelligence software to help companies analyze large amounts of data.

In 2020, however, the company made a sharp turnaround and began investing heavily in BTC, becoming the largest corporate holder of BTC in the world.

In February 2025, MicroStrategy changed its name to Strategy, underscoring its evolution from a traditional IT developer to a player whose strategy is closely tied to digital assets, particularly BTC. Today, Strategy owns hundreds of thousands of BTCs and continues to attract investor attention with its unique financial model.

Why has this question become of interest to many?

Strategy has become too big on BTC, the company owns over 499,000 BTC worth about $43.3 billion. In the summer of 2024, the federal government sold about 44,200 BTC worth $2.9 billion. BTC is down ~25% from its summer high. So what happens if Strategy takes over the sale?

With Strategy stock down more than 51% since November 2024. And that’s when the worries started.

They’ve been through a bear market before” is not a valid argument

Strataegy has been buying BTC since 2020, in various phases of the market, but harping on the fact that they experienced BTC at $15,000 and will do so again is a weak argument.

The company has been playing DCA all along, investing in various phases of the market, but the frequency and volume of investments has increased many times over in recent months. Look at how the average has increased since November 2024. The maximum downward deviation from the average purchase price they have experienced is less than 50% (drawdown).

If the current buying volume continues, the average will be in the neighborhood of $70,000 in less than six months.

The chart shows the frequency of your purchases.

Take notice how often they bought on localized highs, these guys are by no means masters of good entry points and they managed to make a 31% profit since 2020, i.e. we are not talking about some exorbitant returns.

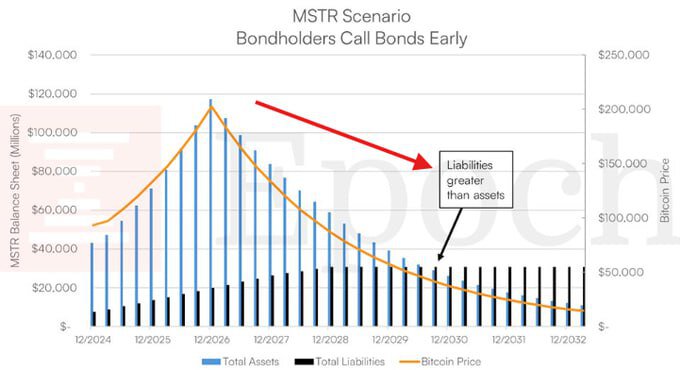

Possible scenarios and liability structure

Take a look at the chart “MSTR Scenario: Bondholders Call Bonds Early”. Hypothetical bad scenario, assuming they buy at such an aggressive pace.

Keep in mind that the strategy is borrowing money extremely cheaply, via convertible bonds. Convertible notes are fixed-rate bonds that can be exchanged for a company’s stock (common or preferred) under certain conditions.

This is a great program because convertible notes allow the company to raise capital without immediately increasing debt or diluting share capital. The interest rate on these notes is 0.625% per annum.

BTC falling below $70,000 could force Strategy to sell BTC

Strategy currently owns 499,000 BTC and their leverage is 19%. This means that some of their BTC are leveraged, which makes them vulnerable to sharp BTC corrections. But you should agree that as long as their leverage does not exceed 30%, it is hard to call their BTC position too vulnerable.

At the current rate of buying, your average BTC price will soon reach $70,000. This means that if there is a sharp drop below this level, your business plan may fail. They will have to sell BTCs, which will only exacerbate the market’s decline.

But here is a detail, Strategy is earning about $110 million per year not on BTC, i.e. cash flow, which can help with debt service and at least delay the sale of BTC and survive the bad times for a while.

The only question here is how much leverage they will get carried away with right now, all within reasonable limits.

This is not an accumulation of BTC, but a stock sale

Rather, the strategy is simply speculating on BTC’s reputation by raising capital through bonds, buying BTC, and then selling shares at high prices.

Look at this pattern again:

- Issue notes (bonds)

- Buying $1-2 billion worth of BTC with them over the course of a day with extensive press announcements

- BTC rises.

- Hence the growth of the strategy (MSTR) stock.

- Bonds can be converted into shares if an investor has just bought bonds with a potential 3-6% annualized return. And sees an opportunity in a few days to convert them into stocks with a 1-3% yield, some will not wait for their bond yield. They’ll just take the money off the table and be done with it.

- So the bonds are converted into stocks, which MSTR gives them at market value, and they are immediately sold into the market.

Here’s a mechanism that gives Strategy a much higher return than the 31% over 5 years of investing in BTC – this is Strategy’s result.

It took a combination of factors to realize this, and they got it:

– to be large enough BTC owners to influence the market.

– influence the community and the investment environment.

– to enter the NASDAQ100.

A logical question might be why buy MSTR when you can buy BTC or BTC ETF:

– In some jurisdictions, capital gains are taxed differently than direct ownership of cryptocurrency ETFs. MicroStrategy doesn’t just buy BTC, it uses leverage to grow positions. This gives investors indirect access to leverage on BTC that most ETFs don’t have; some can’t or won’t hold BTC or its ETFs for regulatory reasons, but can invest in stocks of companies, let alone the NASDAQ 100.

The icing on the cake: MSTR’s market capitalization as of March 6, 2025 is approximately $80.31 billion. The value of BTC on Strategy’s balance sheet is $45.13 billion. That is, the company is worth almost twice as much as BTC on its balance sheet, a pretty big premium for a BTC trading proxy.

Michael Saylor owns 48% of the stock and has only sold $370 million worth of shares. Saylor is under pressure, and if his stock sales become frequent or large, it could raise doubts among investors about his confidence in MSTR’s future.

He really isn’t selling his shares, which puts him in control of most of the company’s decisions and also shows that he himself is truly committed to the strategy of holding BTC. The issuance of shares has given him cheap leverage and increased his ability to influence the market, but so far it doesn’t look like he’s getting out of BTC himself.