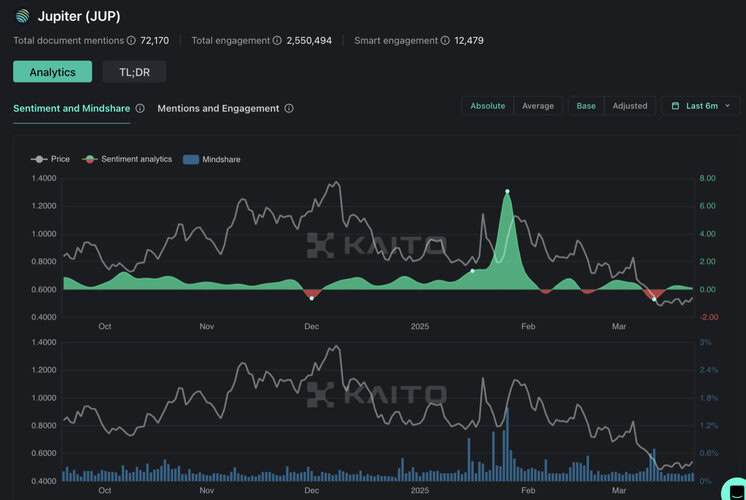

JUP is the best shoulder to play on $SOL, acting as the main proxy of its ecosystem. It is the most widely used, recognized and established protocol in Solana.

A combination of market conditions and negative sentiment surrounding the DAO vote to allocate $JUP to the team has caused the price of $JUP to drop to its lowest level ever.

With upcoming catalysts such as Jupiter’s omnichain Jupnet and the Solana ETF, now is a good time to position for the lows.

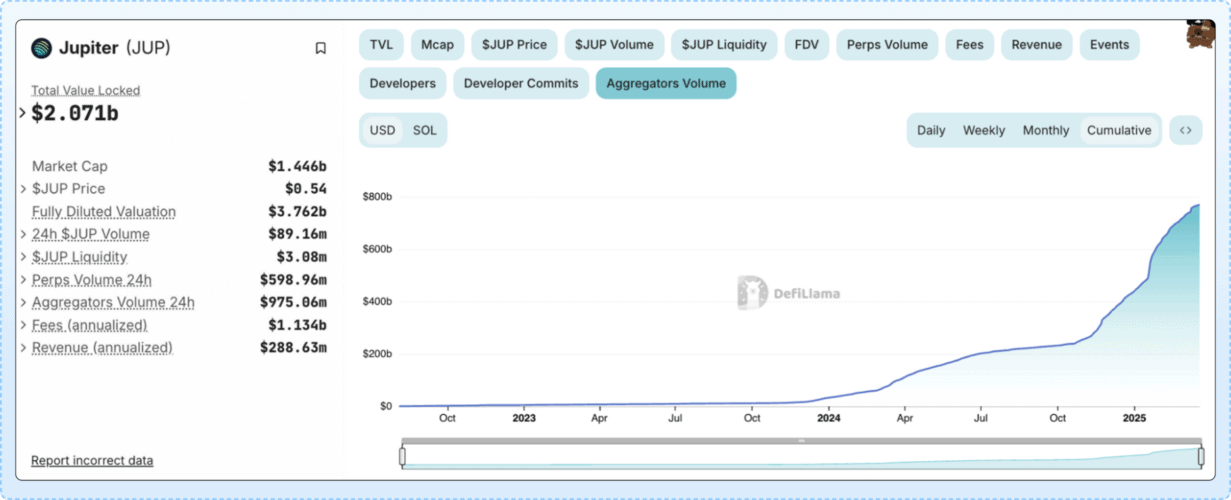

The current undervaluation of $JUP clearly does not reflect the broad user base that Jupiter has been able to build through its user-friendly interface and product development. With current annual commissions of over $1.2 billion, Jupiter’s commission generating capabilities exceed those of Pump.Fun ($547 million).

In addition, Jupiter has a liquid token and a buyback program that allocates ~$160 million annually to $JUP.

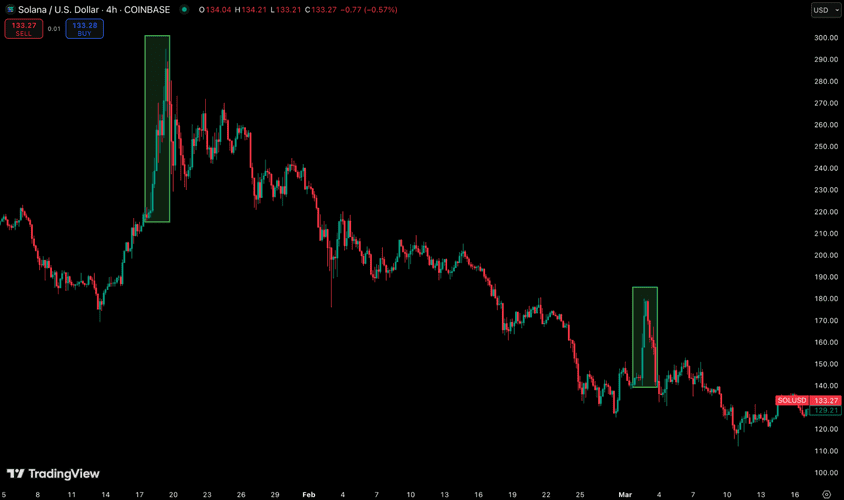

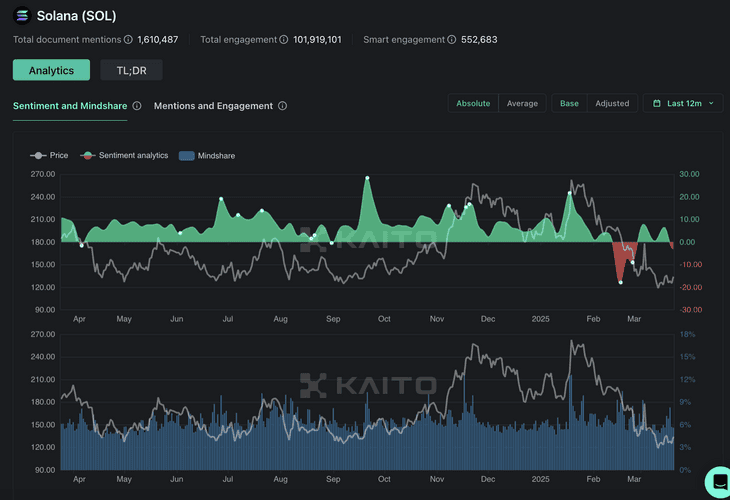

After the initial euphoria and launch of $TRUMP, $SOL suffered greatly during the market downturn in the first quarter, falling more than 55% from the highs. This is a timing mismatch that is currently inconsistent with Solana’s role in the on-chain market.

The Solana ecosystem is the place to bet on fast, speculative on-chain activity – one of the most coveted positions in all of cryptocurrency. With FTX unlocks no longer a concern and Solana ETFs to look forward to, $SOL has plenty of room to grow in the coming months/years. While $SOL may look attractive at these levels, Jupiter represents an even more lucrative opportunity.

While $JUP’s price has fallen, its positioning couldn’t be better. The Jupiter team, led by co-founder Meow, has grown to over 80 people in the past year – that’s several times larger than the average cryptocurrency team. Jupiter has also been very active on the mergers and acquisitions front, acquiring established protocols that can contribute to product offerings, including Moonshot, Sonar Watch and several others.

The team has built a brand with broad reach, becoming a key touchpoint for many when speculating on Solana’s growth and adoption. All of these successes have been built on a solid foundation: the core Jupiter team survived the FTX crash and emerged stronger from its aftermath.

Jupiter has fully embraced its role as an aggregator, expanding its distribution and creating a UX that Solana-based platforms cannot compete with. It is the most resilient protocol on Solana, but also the most vulnerable to negative price changes in $SOL itself. However, this may work in your favor right now, as the market seems poised to reward participants for leveraging $SOL exposure in the coming months.

Jupiter’s stellar leadership has been one of the protocol’s greatest strengths to date. Jupiter seems to be in good hands, with co-founder Meow acting as the face of the protocol and leading the team through various challenges, even deciding to burn some of its tokens and block distribution until 2030.

The main way the Jupiter team is incentivized to continue its string of strong performances is through token incentives, which could also be a negative if $JUP remains without new inflows for an extended period of time.

JUP remains a strong bet, especially in the current market. It is a powerful combination of positioning with leveraged $SOL and working with a high performing team.

Key takeaways

Rebound

$SOL was hit very hard in February, falling 55% to its low. The short to medium term outlook for $SOL now looks much more positive with the FTX release behind us and the Solana ETFs offering something to look forward to.

Positioning is everything

$JUP is ideally positioned to capitalize on the rejuvenation of $SOL, not only from a wealth effect perspective as $SOL liquidity flows into the token ecosystem, but also through its role as a key intermediary in the network that thrives as activity grows.

Back to the fundamentals

The lack of a clear catalyst or narrative makes it difficult to allocate funds between overly speculative protocols with questionable longevity in this market. Jupiter is the opposite of cryptocurrency “junk,” a proven, profitable protocol with a history of successful management through some of the most turbulent times in the space.

Evolving game

From the aftermath of the events surrounding $TRUMP and $LIBRA to the launch of Pump.Fun’s PumpSwap project, which caused $RAY’s valuation to plummet, the meme coin space is volatile to say the least. Fortunately, as an aggregator, Jupiter has not been affected by this chaos, and may even benefit from it. Jupiter may have an advantage thanks to Jupnet, an ambitious omnichain aggregator platform and token launchpad product.

One token rules all

With Raydium’s future uncertain, future flows into Solana’s productive assets are now much more likely to hit $JUP, especially as long as Pump.Fun doesn’t have a token.

Born in darkness

Jupiter was founded in the depths of a bear market, and was not yet a major player when it entered the Solana ecosystem in 2021. The team doubled down after the collapse of FTX, and quickly became a dominant force on the network when activity picked up in 2023.

Aiming for success

Jupiter is actively involved in mergers and acquisitions, using them as a tool to expand its portfolio and expand its reach.

Born in darkness

Jupiter is a pretty battle-hardened team that has been through all the trials and tribulations. Like most Solana teams that existed during the bear market, Jupiter had to survive the collapse of FTX. Jupiter’s co-founder, Meow, has shown no signs of indecision or desire to switch Solana chain, instead tweeting about the important issues arising in the Solana ecosystem in light of the chaos on the blockchain caused by the chain’s proximity to FTX.

Jupiter’s belief in Solana and its product allowed him to create a robust offering that became extremely popular with new or returning Solana users when momentum returned to the chain in mid-to-late 2023.

More recently, the Jupiter team has been criticized for what some believe was a poor handling of the situation surrounding $LIBRA, a memecoin that turned out to be a rug pull. Much of this FUD relates to Meteora, which was co-founded by Meow. While there are past connections here, this FUD is not something substantial or noteworthy that should affect the larger talking points for $JUP. In fact, this FUD simply provided another opportunity for Team Jupiter to demonstrate its commitment to protocol.

Team Jupiter has done everything possible to ensure that the protocol and even individual members are transparent, leaving no stone unturned.

It’s worth remembering that Jupiter plays a key role in facilitating significant events in the Solana ecosystem. This includes high-profile launches such as the $TRUMP launch. Jupiter has gone beyond the traditional responsibilities of a decentralized protocol by taking on some responsibilities more associated with CEX, such as verified listings, assisting with token launches, and promoting ecosystem development.

While not part of the clan of the original Ethereum-based OG protocols like Aave, Uniswap, etc., Jupiter is firmly in the next generation of UX-centric, for-profit protocols. One could argue that Jupiter is the most CEX-like of its peers, an example of what an endgame role for decentralized protocols can look like. It’s a privileged position that not every protocol has, but it also comes with a level of responsibility and trust that the Jupiter team must maintain.

So far, Meow and the Jupiter team have handled objections and allegations of misconduct related to high-profile token launches and listings quite well, as one would expect from a team of this size and caliber.

Another important point to note is that Solana ETFs are likely to be launched this year. Grayscale and other issuer applications will be decided at the end of the year, in October. Because of this delay, the markets may not appreciate the catalysts that far out. The October deadline for these ETFs is also just a deadline.

As with Ethereum, the actual approval could come much sooner. It’s likely that there will be rumors related to the filing that may give more indication as to when the $SOL ETFs may be approved soon.

The launch of the $TRUMP memcoin (left), followed by the announcement of a U.S. crypto reserve, shows how Solana can be prone to rapid upward moves that are almost impossible to predict.

Whether the Solana ETFs will be able to attract the same or more inflows than the Ethereum ETFs doesn’t matter much right now. The markets will likely wait for the ETFs to be approved by the SEC’s new cryptocurrency commission before that happens. At this point, positioning in $SOL or its ecosystem, with continued exposure post-approval depending on expectations and the outcome of inflows, would be optimal.

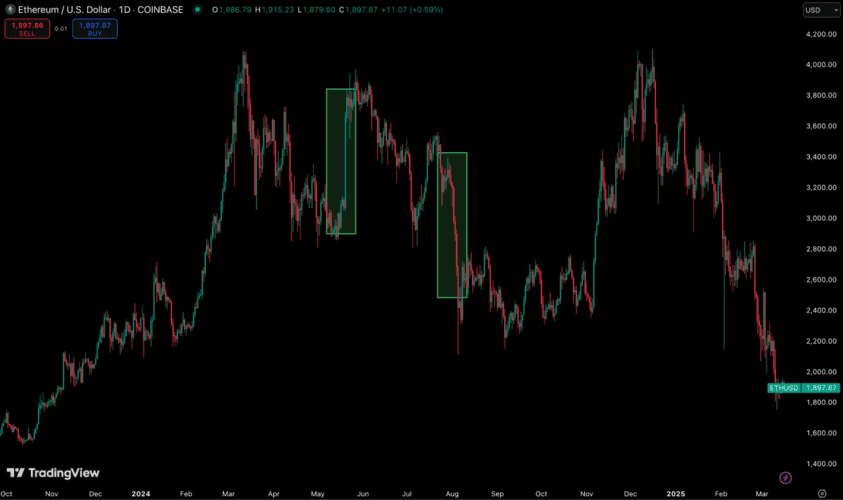

Rumors that surfaced a few days before the surprise approval of the $ETH ETF led to a big price spike (left) and a price crash (right) shortly after its actual trading debut.

All of this suggests that $SOL has probably bottomed, unless $BTC follows US stocks lower. The FTX unlock occurred recently, and whatever range was support for $SOL prior to that needs to be revisited to account for this event.

The fundamentals remain strong and the Solana ecosystem remains intact, ready to be reactivated when market conditions stabilize. Solana ETFs may remain under the radar; markets may begin to price in this catalyst a few months before the start of the second quarter.

While there is little reason to believe that ATHs are imminent, investors may not benefit much from waiting longer before positioning. As market participants slowly return to $SOL, the entire Solana ecosystem will only benefit.

JUP: Memecoins House

Solana has many players controlling different parts of the memecoin trading stack, from Pump.Fun, where tokens are created, to DEX and even trading terminals. As an aggregator that has expanded its offerings, Jupiter is the closest thing to a one-stop shop for speculating on Solana, perhaps more comparable to CEX due to its moat and distribution power. This is all part of the overall trend of decentralized protocols undermining CEX’s role in cryptocurrencies.

When it comes to the idea of crypto casinos, there are a few key areas that can be thought of as different floors in a casino. Token trading is what most cryptocurrencies do, the most common way to speculate. Memecoins are a game with an implied component of chance and luck that players take in the hope of beating the odds. There is much less retail activity in the perps trade, with most of the profits going to a small group of institutions and sophisticated individuals.

Jupiter is present in every area of cryptocurrency speculation known to date: spot aggregators: This is Jupiter’s bread and butter, its first product since 2021, and the driver of most of the protocol’s revenue.

Spot Aggregator

This is Jupiter’s bread and butter, its first product starting in 2021, and the driver of most of the protocol’s revenue.

Trenches

Trenches is Jupiter’s answer to Pump.fun’s user interface and various trading terminals. Users can screen new tokens and consume information instead of just using Jupiter as a means to make trades. Combining token trading and screening into one platform is a powerful combination in the memecoin space, and it definitely makes sense for Jupiter to try and get a foothold in it.

Perps Exchange

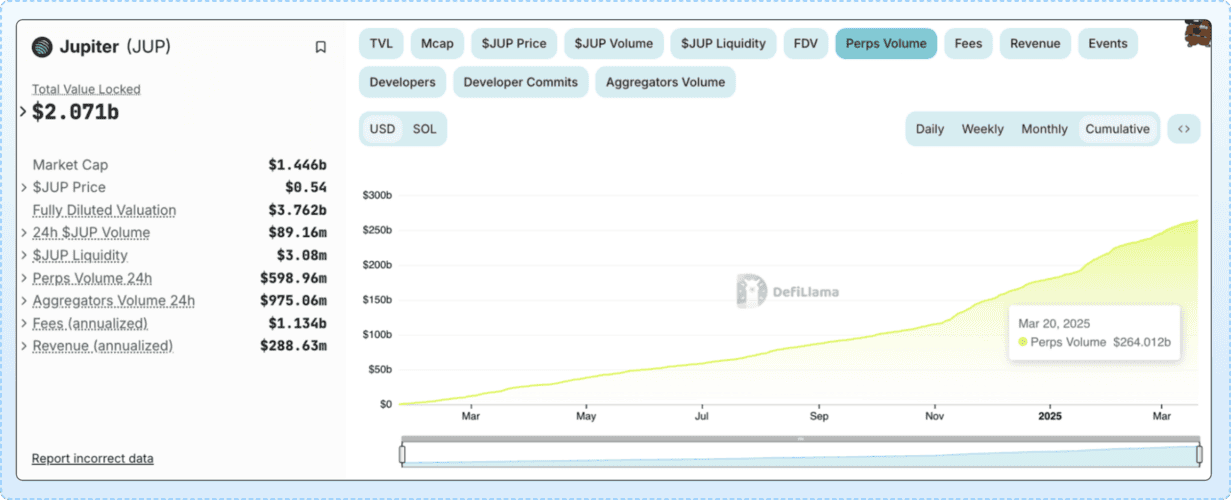

Launching in late 2023, the Jupiter Perps Exchange still only includes 3 markets – $SOL, $ETH and $WBTC. However, the product has already grown to a significant volume. This could be an area where Jupiter could benefit from expanding its offerings, especially during a drought for the Solana ecosystem compared to the peak of the mania.

In addition to its core areas of speculation, Jupiter also has a passive $JLP vault containing over $1.4 billion in TVL. JLP serves as the liquidity backbone for Jupiter’s proprietary markets. JLP denominates deposits for all assets for which Jupiter offers a perps market: $SOL, $WBTC and $ETH, as well as stables. This can serve as an index of sorts, returning 75% of the Perps trading commission to depositors. In addition, the Jupiter Launchpad platform will be launched soon, which could be a key offering of the protocol.

The main difference between Jupiter and CEX in the proposals is that Jupiter only runs on Solana. At this point, this is fine – there is already a consensus that Solana is the place for protocols that facilitate trading activity, as this is the chain where most hot money is found. Jupiter seems content to dominate Solana for now, and doesn’t want to make the mistake that top DEXs like Uniswap and Sushi have made in the past of running multiple chains, many of which simply weren’t worth the effort in the end.

There is also no question about how speculative activity on $JUP is affecting the value of the token for holders. Last month, the $JUP buyback program was launched, with 50% of the protocol’s revenue going toward the buyback. There are more applications generating serious revenue today than there were a few years ago. Many of these protocols, including Hyperliquid, Raydium, Aerodrome, and others, include buybacks or other ways to generate revenue.

Perhaps the buyback is becoming less of a differentiator and more of an expected qualifier for those seeking access to leading revenue-generating protocols.

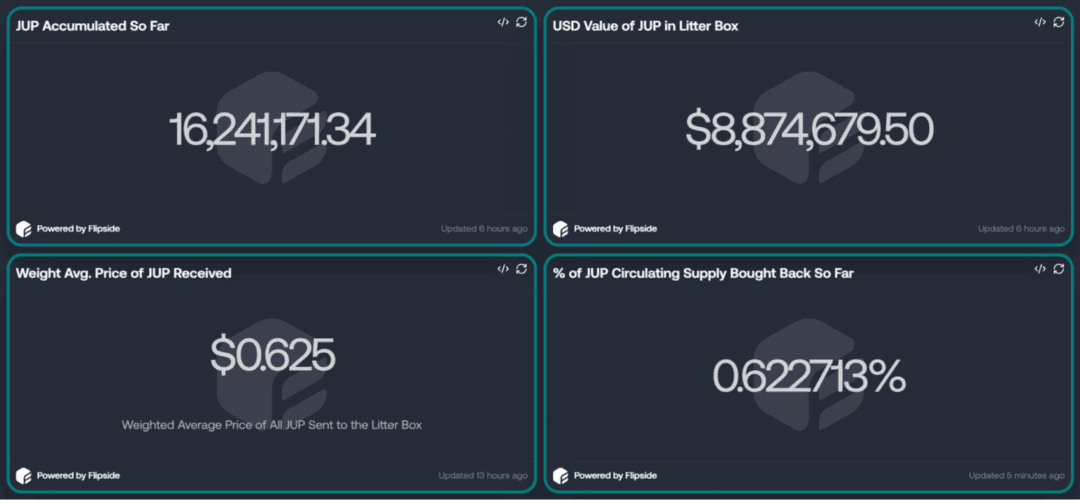

Looking specifically at the Solana ecosystem, the Jupiter ransomware program claims $JUP as the ultimate token for exposure to $SOL. $JUP will be redeemed and held in escrow for at least 3 years, which is likely longer than most other buyers in the market.

This is something that can serve as a buffer against unlocks. On net, the supply of tokens in circulation will still increase, and there will be additional selling pressure on the token in the long run. Market participants shouldn’t overreact: the narrative is still the primary driver of all tokens, whether they have redemptions or not. But these redemptions definitely help keep the demand for $JUPs steady.

Jupiter is able to generate increased revenues even during market drawdowns, thanks to a certain amount of backup demand (“emergency buying”) and an implicit price floor for the token.

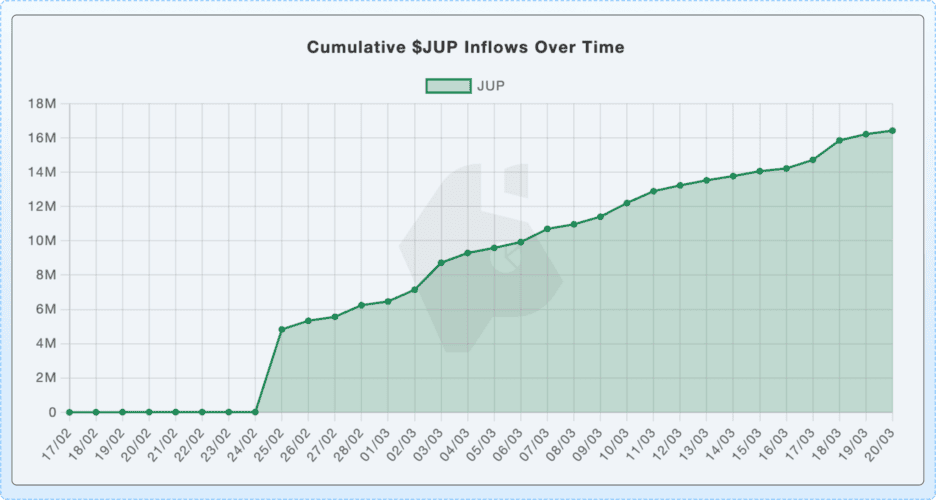

At this point, these buybacks are simply not enough to move the price of $JUP. However, if trading activity returns to the highs, these transactions could certainly become a much more fundamental driver of price movement, separate from anything related to the narrative. Since trading began on February 18th, approximately 9.5 million $JUP tokens have been redeemed for approximately $6 million, which is certainly small compared to $JUP’s market value of $1.7 billion, but it’s a good start.

Like all buybacks, this scheme aligns incentives between the team and the community. More importantly, it creates a link between protocol performance and token price, which is one of the hardest things to do for most protocols. There is a more structural price behind $JUP that simply runs in the background, rewarding token holders when the team releases updates to increase trading volume, or simply when market conditions dictate more activity.

Evolving Game

The all-encompassing nature of Jupiter as an app provides a true one-stop shop for speculating on Solana. The main piece of the pie that Jupiter lacks in terms of user experience is the actual creation of tokens, which is dominated by Pump.fun. This imbalance is extremely significant considering that despite all of Jupiter’s offerings and developments, its extensive product suite has generated roughly the same amount of earned commissions (not including $JUP incentives) as Pump.Fun, which has a much simpler interface and a seemingly much less complex product.

Jupiter has its own launchpad, but it’s used for high-profile token launches, including $TRUMP and $JUP, rather than creating tokens without permission like on Pump.fun. For the most part, Jupiter is sticking to what it does best, ensuring that trading on the platform is seamless and that the necessary options are available for more sophisticated users.

From DCA and limit orders to maximizing slippage, Jupiter has implemented all of the aggregator’s features to provide the best user experience.

Analyzing the numbers

While Jupiter doesn’t necessarily compete with Pump.Fun or Raydium at the protocol level, it does compete with them in terms of token valuations. In cryptocurrency, valuations typically fall short of reasonable revenue expectations. But that doesn’t mean that revenue metrics should be discarded, especially when it comes to high-end protocols like Jupiter.

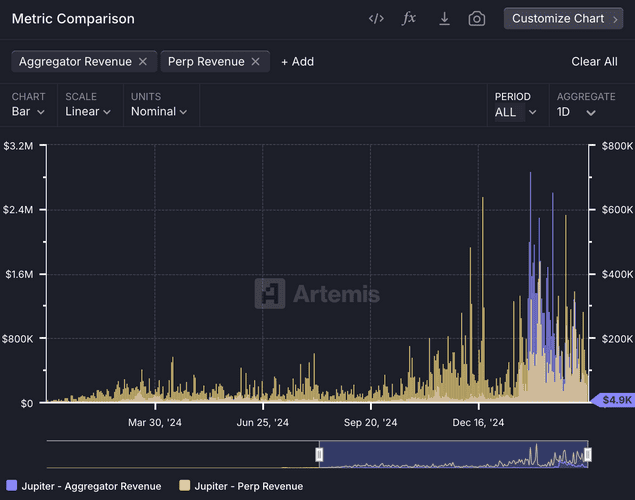

One way to assess the relative value of $JUP is to analyze its commissions compared to its peers. On any given day, Jupiter could be one of the highest earning protocols in cryptocurrency, often ranking in the top 5 in terms of commissions earned. During the recent market downturn, its profit margins have been much more stable than Pump.Fun’s. This was hard to believe just a few weeks ago.

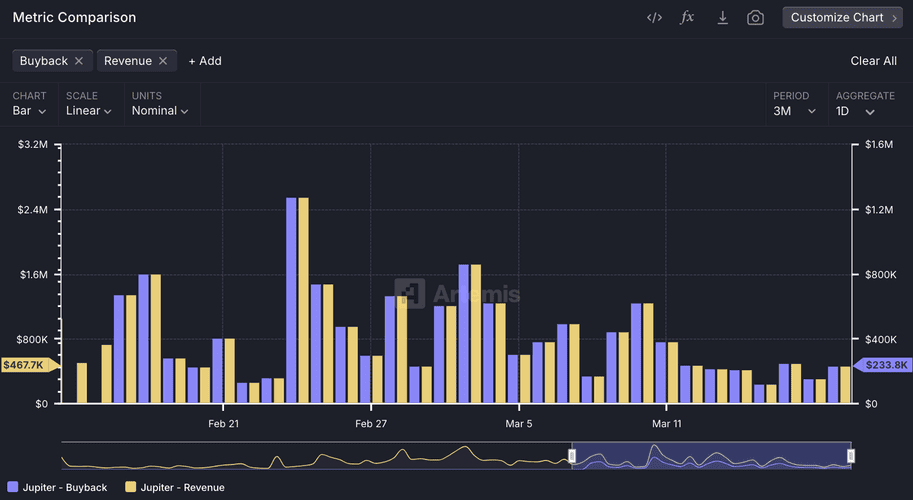

Since almost all of Jupiter’s fees come from perps and the Jupiter aggregator, it is important to understand how these products can generate revenue for $JUP. The structural way in which the success of the protocol fundamentally affects the price of $JUP is through token redemptions made less than a month ago.

Revenue from the Jupiter aggregator is distributed as follows

- 50%: $JUP buybacks

- 50%: Protocol revenue

Jupiter Perps have a separate commission split:

- 75%: Distributed to $JLP contributors

- 12.5%: $JUP buybacks

- 12.5%: Protocol Revenue

Some may be surprised to learn that Jupiter Perps account for the vast majority of protocol fees. However, perps and spot swaps are about equally important to $JUP redemptions. The share of redemptions in Jupiter aggregator commissions is 4 times higher than perps (50% vs. 12.5%), which makes up for the much smaller nominal amount of commissions earned.

After ~3 weeks, Jupiter bought back ~14 million $JUP tokens worth ~$7.5 million. That’s not too much considering $JUP’s large market cap ($1.4 billion). Note that these redemptions occurred at a time when the price of $JUP was falling. Still, this is a decent start at a time when protocol activity is low compared to a few weeks ago when the buybacks began.

Based on last month’s data, Jupiter’s projected annualized revenue is ~$320M. If we assume roughly the same revenue split between perps and aggregators, then ~50% of the projected revenue will go to buyouts, resulting in ~$160M of buying pressure for $JUP.

This is a somewhat conservative figure, and it is reasonable to assume that an annualized repurchase volume of $160 million is an appropriate benchmark for repurchases. The actual number could be much higher as activity increases. As seen with $TRUMP, Jupiter can work directly with teams that could be powerful catalysts for Solana’s trading activity.

At the current $JUP price and protocol revenue metrics, annual buybacks will account for more than 10% of supply. As the $JUP price stabilizes and increases, this percentage of buyout supply will decrease. This is likely because the $JUP price is more sensitive than protocol revenue. In some ways, a negative price trend could be positive for the long term, as it means that more of the $JUP supply will be purchased and taken offline within 3 years.

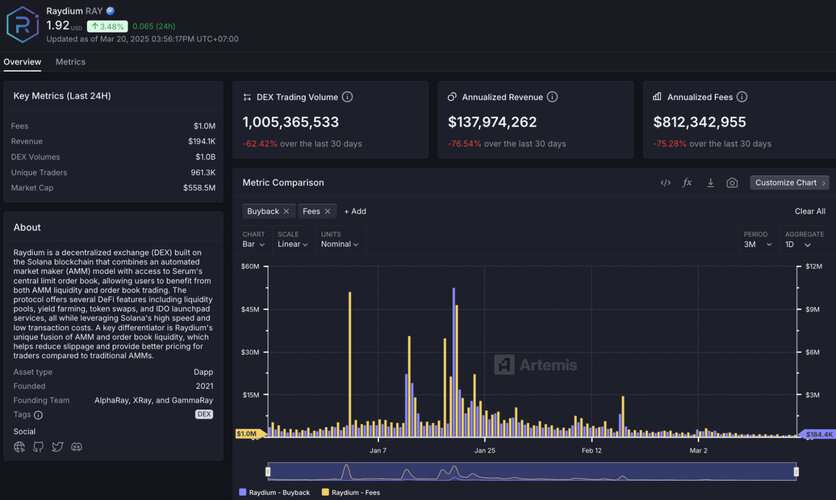

Another way to measure the value of the $JUP buyback is to compare the buying pressure to that of Raydium $RAY. At the current price of $JUP ($0.51) and protocol revenues (~$320M per year, of which about half goes to buybacks), Jupiter’s P/E is 8.64. Raydium, on the other hand, has a forward P/E multiple of 3.49, less than twice as high. These multiples only reflect the amount of earnings going to buybacks.

From a P/E perspective, $JUP is valued much higher than $RAY, and rightly so. But compared to some of the other top revenue-generating protocols, $JUP’s valuation remains low. Take Uniswap, for example: assuming a 20% redemption fee, $UNI’s forward P/E is 23.8. Ultimately, P/Es should be viewed as a benchmark in cryptocurrency, regardless of whether they are positive or negative for a particular protocol.

A gateway to the Solana ecosystem

As a front-end, Jupiter primarily serves as a user hub for speculating on Solana. This gives Jupiter an advantage in some ways, as it is not overly dependent on a single niche like Pump.Fun.

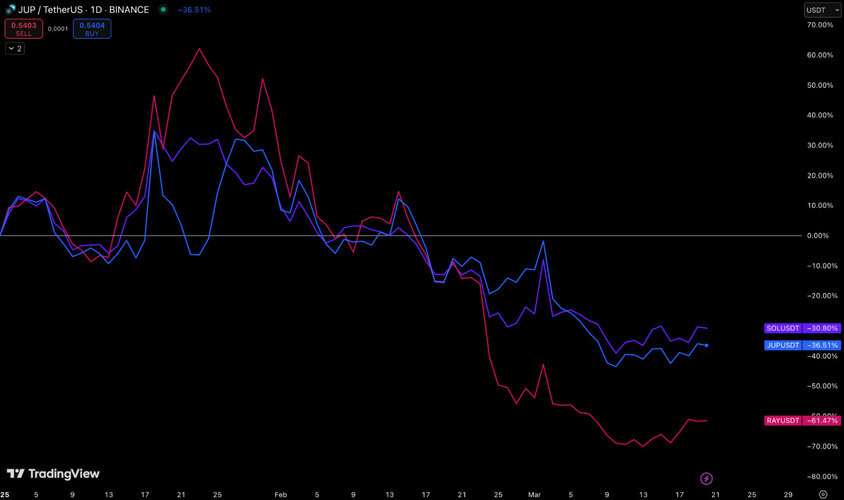

When analyzing $JUP against the other tokens in the Solana ecosystem that are most associated with blockchain trading activity, there is one major competitor: $RAY.

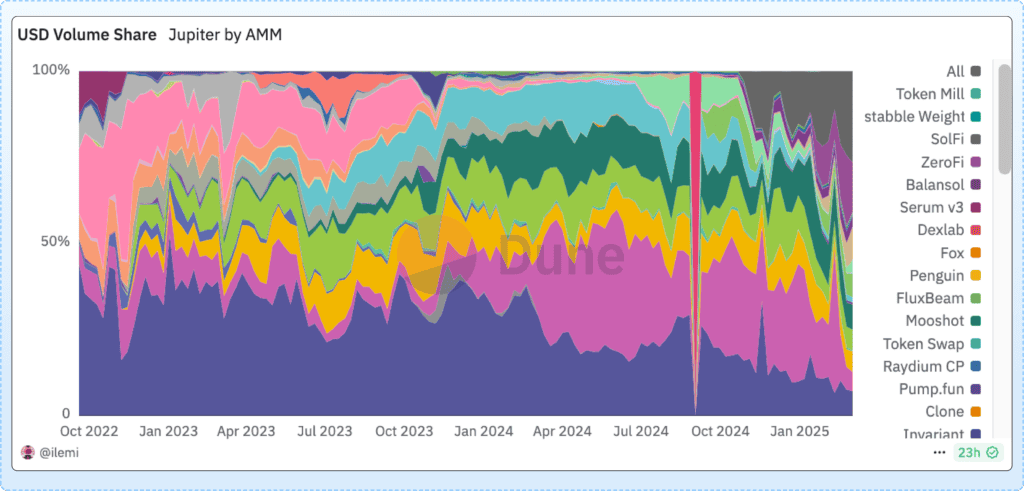

Raydium ($RAY) has, until recently, been considered the other main avenue for exposure to Solana. Raydium is the leading DEX in terms of total DEX volume. Raydium has a much less polished UX than Jupiter; in many ways, Raydium used to win when Jupiter improved its UX and expanded features, as some of the swap increases those improvements would create would find their way into Raydium AMM.

A major factor in $RAY’s dominance last year was its integration with Pump.Fun, which resulted in tokens issued on the platform being linked to the Raydium AMM pool. This is a structural reason for Raydium’s dominance in 2024. DEX had the inherent advantage and ability to guarantee the closest position to the trading flows of Pump.Fun tokens.

$RAY is one of the best deals of 2024 to get the most out of the memcoin sector.

After it was revealed that Pump.Fun was developing PumpSwap, $RAY began to capitulate. This would be extremely detrimental to Raydium’s business model; during the memcoin craze, Raydium regularly accounted for 30-40% of Jupiter’s AMM volume share.

Now that Pump.Fun has decided to withdraw tokens to its own AMM, the argument for using Raydium pools instead of another DEX becomes much less clear. Prior to Pump.Fun, Raydium’s market share was often in the single digits, with $ORCA being the main leader. This has not helped Raydium’s confidence in any way; $ORCA’s market capitalization today is only ~$90M. The impact of all these events has caused $RAY to drop nearly 75% to a market value of ~$640M, although some of this drop is simply due to the price action of $SOL and general market conditions.

More recently, it was announced that Raydium would be building its own version of Pump.Fun. It’s not all rosy – Pump.Fun completely dominates memecoin creation on Solana; it’s not a given that Raydium will get enough attention. It’s easier for an application like Pump.Fun to create an AMM infrastructure than the other way around. This tug-of-war between Pump.Fun and Raydium makes $JUP even more attractive because Jupiter benefits from any trading activity – no matter which side it comes from.

As an aggregator, Jupiter won’t necessarily be affected by either Pump.Fun’s or Raydium’s developments, though it’s worth noting that the launch of PumpSwap allows Pump.Fun to capture a larger portion of the memcoin stack, just as Jupiter has expanded its operations into other areas of trading over time rather than focusing on one thing. Jupiter will integrate Pump.Fun’s AMM, though Pump.Fun’s role in tokenization makes it more attractive for users to bypass aggregators and trade directly on the DEX itself, more so than Raydium or Orca.

In general, Raydium continues to receive a lot of “structured” volume from Pump.Fun – i.e. the traffic flows on its own, even if Raydium doesn’t do much of anything. At the same time, Jupiter can be seen as a platform that handles higher quality, “earned” volume – not dependent on a single integration. Instead, its strengths lie in its thoughtful interface (UX) and now even broader reach (distribution).

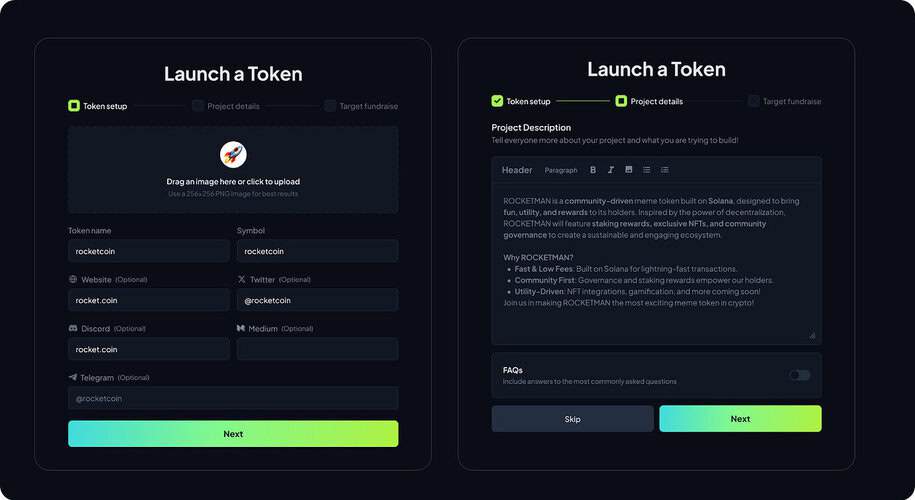

As an aggregator, Jupiter relies on the volume of Pump.Fun and Raydium rather than competing directly with them. However, Jupiter is looking to enter the launchpad market, which could lead to a collision with Pump.Fun. The current iteration of Jupiter’s launchpad is designed for high-profile token launches, such as $TRUMP, and does not emphasize the protocol over its other products. This will change with the introduction of CATPad.

CATPad is a permissionless token launch platform originally modeled after Kickstarter. Users can fundraise for their token for a set period of time, with a minimum amount of funds that must be raised for a token sale to take place. The maximum fundraising period is relatively short – only two days. If the sale is successful, the creator receives almost 90% of the token supply with a vesting period of 2 years. This is the first way of generating tokens on Launchpad, others may be introduced in the future. More details will be announced next month.

It is difficult to predict how widespread CATPad will become and whether it can become a viable alternative to Pump.Fun. There is a gap in the market when it comes to being able to seamlessly launch tokens while providing some price stability for early buyers and automatically allocating supply to the token creator. Pump.Fun in its current form is not up to the task and there is room for new players.

Onchain conglomerate Jupiter’s business model as an aggregator depends on its ability to attract attention, so it puts a lot of focus on UX and distribution optimization to give users a reason to choose Jupiter over mainstream DEX. When it comes to token creation and liquidity management, not much depends on Jupiter, and the protocol serves to maximize what already exists on the blockchain. Jupiter needs to stay current and extend its services to the widest possible user base. This could include existing cryptocurrency users, both in Solana and outside of Solana, or even attract new users to cryptocurrencies altogether.

We’ve seen CEXs like Binance, Coinbase and others expand their offerings beyond their core business over the years. As price action moves to the blockchain and decentralized protocols begin to generate massive revenues, it’s only natural that they begin to take steps to invest in their future success.

Jupiter is expanding its business on the blockchain in a new way that’s different from what we’ve seen before with Ethereum protocols that have reached juggernaut size. Jupiter is purposefully engaging in mergers and acquisitions, which is responsible for the new products they have been able to release.

ApePro – September 20, 2024

Jupiter acquires Coinhall, a leading DEX aggregator on Cosmos, primarily interested in the ape.pro product. This product, which was integrated into the Jupiter platform as a proprietary terminal, has now partnered with Jupiter to create “Trenches”, a revamped interface for trading memcoins.

Moonshot – January 25, 2025

Jupiter acquired Moonshot shortly after the launch of the $TRUMP token, which brought 200,000 new users to the app in a single day.

Both of these acquisitions are important because they allow Jupiter to control a portion of the memcoin and trading stack that was otherwise inaccessible to centralized or semi-centralized applications and trading terminal platforms. Although Jupiter is a decentralized protocol, acquisitions of this nature push Jupiter towards CEX status when it comes to distribution.

Other acquisitions include:

Ultimate Wallet

April 23, 2024: This acquisition was actually incredibly important: it allowed Jupiter to launch its mobile app, which climbed to #5 in the app store rankings right after the launch of $TRUMP.

Buying Sonar Watch was a strategic move

It helped us quickly release our own portfolio tracker (Jupiter Portfolio).

SolanaFM

September 20, 2024: This acquisition expanded Jupiter’s internal data infrastructure and analytics capabilities.

No other decentralized protocol in cryptocurrency has been as active in the M&A market as Jupiter. More importantly, no other protocol has made numerous acquisitions and successfully used them to expand offerings in areas that are productive for the underlying protocol.

Some examples of questionable acquisitions include Uniswap’s purchase of Genie in an attempt to expand its presence in the NFT space. This ultimately failed, as did Uniswap’s acquisition of Crypto: The Game, a crypto-themed on-chain survival game. Then there’s Polygon, which spent hundreds of millions acquiring a number of crypto-related protocols and solutions that remain largely unrecognized by the market today.

Jupiter is filling gaps in its product stack by any means necessary. The team has also made a deep shift toward “public building” and marketing, which was not a priority in the early days of the protocol. The results of Jupiter’s mergers and acquisitions have definitely paid off in terms of gaining momentum and attention for Jupiter’s product suite. It is evident that the Jupiter team will leave their comfort zone when there is an opportunity to expand their sphere of influence.

New Horizons

Jupiter is a prime example of a protocol that knows its niche and doubles down on it. Fortunately for Jupiter, they can’t find a better niche than speculative activity on Solana. But that doesn’t mean the team doesn’t have room to grow their product. Jupiter now has a team of ~80 people, 65 of whom were hired last year. This provides enough resources to gradually expand Jupiter’s reach, in addition to the hundreds of millions of dollars in revenue from the protocol.

Jupnet is perhaps the most ambitious Jupiter move we know of. Not yet launched, Jupnet will act as an omni-chain aggregator. There is a lot of liquidity flowing in and out of Solana. Jupnet is Jupiter’s attempt to keep much of that value in its ecosystem, even after it leaves Solana.

But Jupnet goes beyond being an aggregator that can do inter-chain routing; this initiative is best understood as an attempt to create the closest thing to an on-chain CEX. What Jupnet is trying to accomplish from a user perspective is in some ways similar to Particle Network and other protocols under the banner of network abstraction.

Not many details about Jupnet are available at this time. More information is expected to be released in April, which could be a bit of a catalyst for $JUP in the short term. Jupnet offers a degree of diversification and independence compared to $SOL. This makes $JUP potentially viable even for those who are pessimistic about Solana as a whole and compare the ecosystem to a large casino that has already run dry.

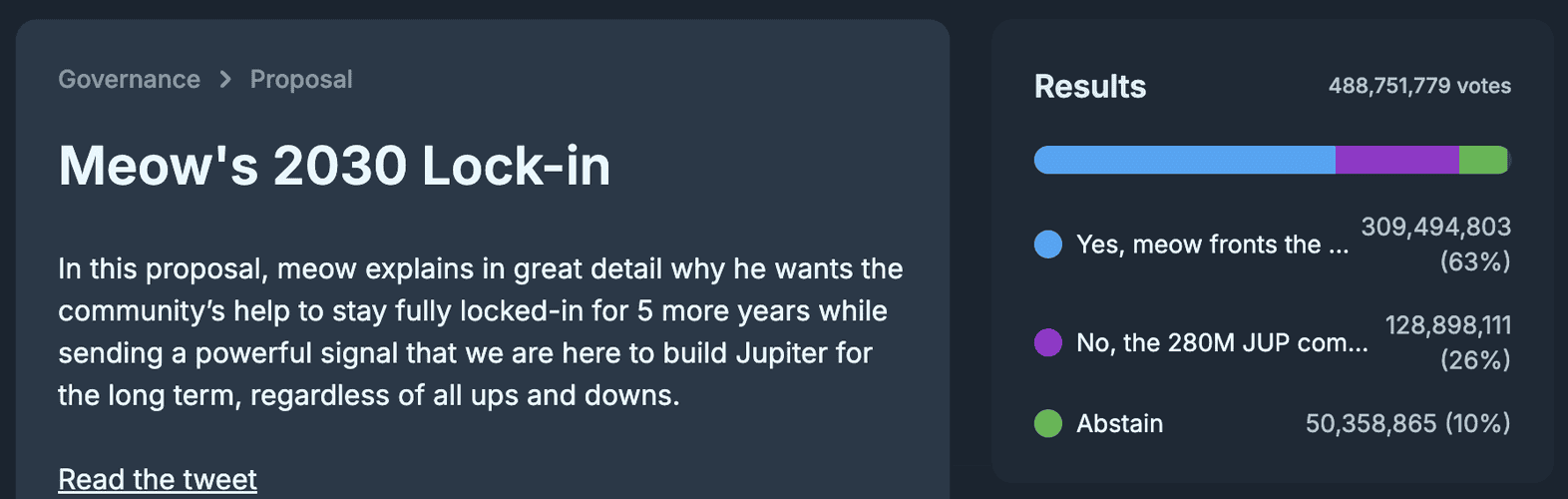

Locked in

The Jupiter DAO recently had a successful (63%) vote regarding team allocations. It had already been decided that non-core Jupiter members would be rewarded with 2.8% of the $JUP. The controversy was that Jupiter co-founder Meow proposed to fund this initiative with all of his $JUP instead of Jupiter’s strategic reserve. In exchange, Meow would receive his original allocation with an additional 80% bonus in 2030. This change significantly increases Meow’s share, but locks it in for several more years than would otherwise be possible.

While this DAO controversy drew criticism from those outside the Jupiter community, it was later resolved positively. Ultimately, 2.8% of the maximum $JUP offer is at stake, and Meow’s 2.2% bonus is locked in until 2030.

Depending on how you look at it, this offer could leave tokenomics and unlocks in better shape than they were before. Instead of unlocking ~$280M $JUP in June 2026, an equal amount will be distributed to dozens of team members over 3-4 years. There will likely be more pressure to sell before June 2026, but less after, assuming Meow would have sold some of the $JUPs soon after they became available to him.

With the DAO vote finalized, there is greater certainty about the dynamics of $JUP supply and release. Resolving this issue and reaching a final outcome also enhances Jupiter’s reputation by showing that it can easily resolve disputes within its community.

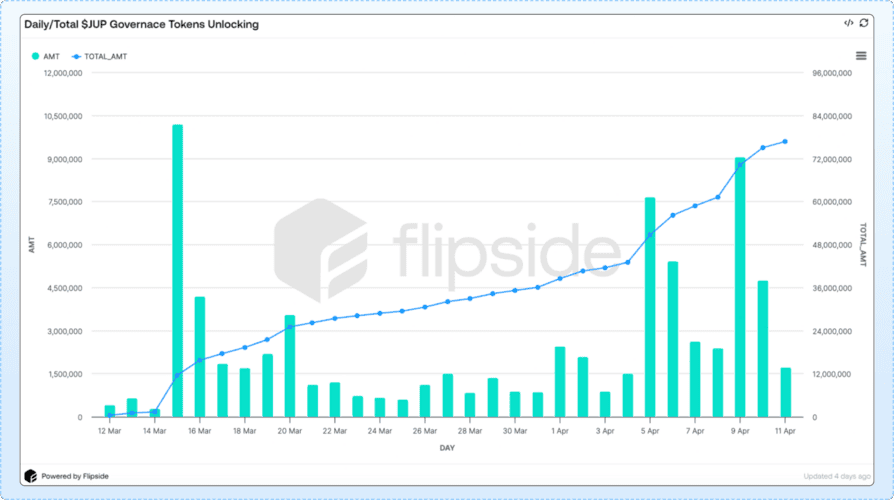

Unlocks

Unlike the buying pressure of $JUP redemptions, not all token unlocks result in selling pressure. Jupiter also has a history of changing the unlock schedule, which can result in tokens being locked for much longer than originally planned. However, it is important to monitor these unlocks for entry and exit positions.

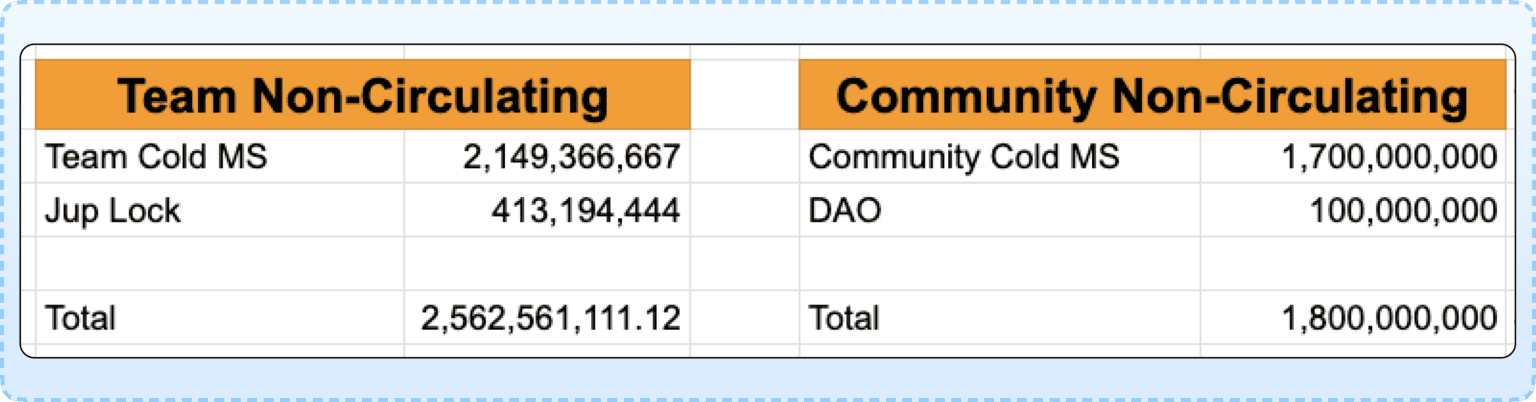

In total, approximately 4.7 billion $JUP tokens remain to be allocated: 1.8 billion to the community and 2.56 billion to the team. Not all of these reserves have been allocated yet, especially to the team; most remain in strategic reserve with no clear plans for vesting. Below are the most significant and current unlocks. The most significant current release is the team’s $466 million JUP allocation through 2025.

OG Team Allocation

$1.4 billion $JUP (20% of the offering). OG Jupiter team members will be rewarded with 20% of supply $JUP, distributed linearly over three years.

- 466M $JUP (~33%) began circulating, but is now blocked until 2027.

- 466m $JUP (~33%) currently in vesting with monthly splits and transitioning to quarterly rights on May 1.

- 466 million $JUP (~33%) vesting starting in February 2026.

Mercurial Stakeholders – $350 million $JUP (5% of the offering)

Mercurial was a former Solana project that the Jupiter team participated in before fully transitioning to Jupiter and Meteora. The amount of supply allocated to Mercurial token holders is a significant monthly allocation: ~$13 million $JUP per month until the end of 2026.

Jupuary – $1.4 billion $JUP (20% of total supply)

Jupuary is the largest source of unlocks. Fortunately, the next Jupuary airdrop will take place in January 2026. ~700 million $JUP tokens will be distributed to protocol users and stackers. Another Jupuary airdrop is planned for 2027, but is not yet confirmed. Jupuary covers almost all of the $JUP allocated to the community.

ASR (Active Staking Rewards) – 200 million $JUP (~2.8% of supply)

Active Staking Rewards are unlocked quarterly; the next date for these rewards to come online is expected to be 2 months from now, sometime in mid-May. After the last ASR unlock, the price went up immediately, as it did after the January unlock. There may be more funds allocated for ASR in the future.

Meow’s allocation is $500 million JUP (7% of the offering)

This allocation is locked for five years and represents Meow’s entire allocation.

New team allocation – $280 million JUP (4% of offering)

The exact timing of the first cliff and vesting of these funds is not yet known. They will be distributed over 3-4 years.

Governance-related unlocks

These unlocks cannot be tracked more than one month in advance, which is the time it takes for the $JUP voters who initiated the unlock process to receive full access to their tokens. These unlocks can be in the tens of millions per month and can be increased after significant DAO votes.

Currently, approximately $54M of $JUPs (0.7% of the supply) are unlocked on the 1st of each month. The selling pressure from these unlocks exceeds the buying pressure from redemptions (~$10M per month), suggesting that most of these tokens are sold immediately.

This is an important point because it makes $JUP vulnerable to a bear market. A bear market causes the price of $JUP to fall, reducing redemption volumes and increasing the likelihood that team members and other recipients of anlocks will sell tokens. However, this is fairly predictable and can be positioned accordingly.

Overall, the continued unlocking of $JUP supply is a strong reason to be selective about the market timing and duration of $JUP trading. With this in mind, the Jupiter team has done much to show solidarity with the community, including Meow blocking his allocation for 5 years and also choosing to burn 3B $JUPs (30% of total supply).

There may be many more times in the future when the team will voluntarily block tokens or give the community more rewards than they have already allocated. It’s important to keep an eye on the news and management votes on unlocking.

Risks and Timing

The $JUP thesis is more suited to a long-term buy-and-hold or swing trading strategy, as opposed to trying to play short-term events or catalysts. This is partly because the team often works in the shadows and we can’t predict when the real surprise will happen, so it pays to have some margin of safety and positioning. Jupiter has made a number of off-the-cuff announcements at conferences, such as the recent acquisition of Moonshot, which came just days after the app played a critical role in the launch of $TRUMP.

Simply put, Jupiter’s status as one of the top protocols generating commissions on any given day can make it much more comfortable to hold that risk; this applies to multiple tokens representing the most profitable protocols, not just $JUP. This can serve as a buffer against precise timing, as it is less likely that $JUP, $HYPE and other tokens with large market caps and token redemption programs will suffer as much as other sector tokens if a trader is on the sidelines when the market moves against them.

Timing is still important, although there is some comfort in the fact that $JUP has decent tokenomics and demand for the token. There is still a good opportunity to position in Solana right now without going too far out on the risk curve. A return to mean for $SOL may be in order, and what level is “mean” for Solana has changed since FTX was unlocked. Anything above the $200 level is definitely closer to $SOL’s fair value, and future upside potential for $SOL and ecosystem tokens is becoming increasingly limited unless new catalysts emerge.

When it comes to risks with $JUP, it’s hard to think of any that haven’t happened in the past. The correlation of $JUP with $SOL and basic execution risk are the most likely reasons for the decline. The team has already seen the FTX crash. It’s hard to imagine a more catastrophic event for the Solana protocol, although obviously Jupiter didn’t have a liquid token at the time.

Events like this provide some confidence in the protocol’s ability to withstand large drawdowns in the $SOL price and properly handle execution during bear markets.

Jupiter has become one of, if not the most important protocol to Solana’s success, although the interdependence is somewhat mutual at this point. A sustained decline in Solana, which would likely coincide with a decline in $SOL, would be the most serious obstacle for $JUP. A trend of this magnitude would likely take months, if not years, to develop.

Right now, Solana is the most active location with the highest trading volume that apps can take advantage of; if something catastrophic happens to the chain, Jupiter is one of the best capitalized and experienced teams capable of moving elsewhere. That said, speculating on such things is mostly foolish. Buyouts are nice, but at this mcap and FDV they don’t move the price, so they’re not worth considering when timing a trade.

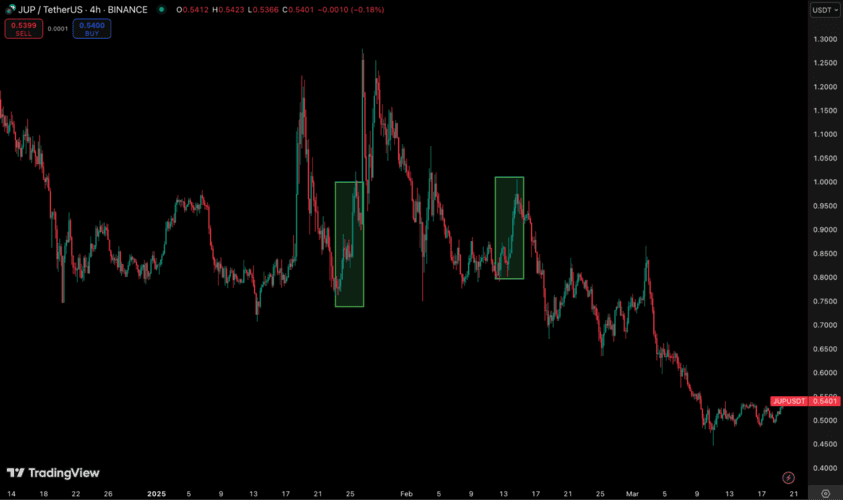

The price of $JUP rebounds after the January airdrop (left) and ASR release (right).

Conclusion

$JUP is a true on-chain conglomerate. In the current market environment, there may be an increased demand for less speculative, established and above all profitable protocols. This is underscored at a time when $SOL appears to have bottomed out, with the FTX release just past and the asset’s inclusion in the U.S. Cryptocurrency Reserve occupying investors’ minds.

The tailwind for Solana will benefit Jupiter immensely, but the thesis behind $JUP is the company’s proven ability to meet its obligations, expand its operations and generate revenue. Solana is a chain with a large number of users and active liquidity, creating the best environment for revenue generation, and $JUP remains one of the best user-centric protocols capable of consistently generating commissions.