Key Takeaways

● In 2024, the crypto industry experienced signicant growth, with market capitalization rising by 96.2% year-on-year (YoY), driven by strong gains in the first and fourth quarters. The launch of spot BTC ETFs in the U.S. in January marked a pivotal moment, boosting market sentiment and attracting new capital. Favorable macro conditions, including the U.S. Federal Reserve’s interest rate cut in September and positive regulatory expectations post-U.S. Presidential election, further propelled the market. Key narratives included the points meta, restaking, memecoins, AI agents, and stablecoins. Looking ahead, we are monitoring global monetary policies, regulatory changes, new ETF approvals, and the emergence of crypto-specic narratives.

● Bitcoin had an eventful 2024, bookmarked by the U.S. spot ETF approvals in January, and the breaking of the long-anticipated US$100K mark in December. The ETFs proved historically successful, attracting around US$35B in net inflows and boasting over US$105B in total assets. Bitcoin dominance exceeded 60%, a level unseen since 2021. Performance versus traditional assets remained extremely impressive, leading almost all traditional investments. On the demand side, the 4th Halving event halved annual Bitcoin issuance, while the Bitcoin ecosystem bloomed, including a 2,000%+ rise in DeFi total value locked. As we look ahead, the growing maturity of the ETFs, the incoming Donald Trump administration (perhaps aided by a Strategic Bitcoin Reserve or further corporate Bitcoin adoption), and a growing Bitcoin ecosystem around Layer 2s (L2s), Decentralized Finance (DeFi), and more, are some factors that excite us.

● In 2024, Ethereum led alt-L1s in metrics like market cap, trading volume, and DeFi TVL, while activity metrics such as daily transactions and active addresses were dominated by Solana, which also offers the lowest average transaction fee. In 2025, the U.S. Ether ETFs, the potential for more dApps in launching their own chain, the Pectra Upgrade, and Ethereum’s prioritization dilemma are key stories to consider. Solana broke fee and DEX volume all-time highs multiple times in 2024 and developer interest grew signicantly, however, stablecoins on the chain remained relatively low. Their new upcoming client, Firedancer, network extensions (i.e., Solana L2s), and SVM stack chains are important stories to follow. BNB chain saw scalability progress with opBNB and data storage development with Greeneld. Sui outgrew Aptos, while Avalanche saw its largest update yet with Avalanche9000. Tron was strong in stablecoin transactions (although saw its position challenged). TON, which slowed in H2 2024, remains important to watch, alongside the launches of Berachain and Monad.

● For L2s, 2024 was earmarked by a plethora of token generation events across both the optimistic and zero knowledge types, with over nine major L2 token launches taking place over the course of the year. It was, however, the Base L2 that stole the limelight in 2024. Despite its lack of a token, Base grew to capture 39% and 67% of the market in terms of total value locked (TVL) and daily active users respectively, Full-Year 2024 & Themes for 2025 4 making it the top L2 in both metrics. With many of the airdrop rewards now behind us, 2025 will tell which L2s can sustain user activity and capital without relying heavily on token incentives.

● 2024 has marked a robust recovery for DeFi, driven by a substantial inux of capital that propelled total value locked up by 119.7% year-to-date (YTD) to US$119.3B. This resurgence has sparked a renaissance across DeFi sub-sectors, with core areas like Money Markets and Decentralized Exchanges (DEXes) reaching new milestones. The year has been dened by the emergence of previously inaccessible on-chain nancial primitives, the narrowing gap between DeFi and Centralized Exchange (CEX)-like experiences, increased adoption by both consumers and institutions, and heightened protocol competition. Together, these developments are paving the way for DeFi to nd product-market and deliver tangible impact in the real-world.

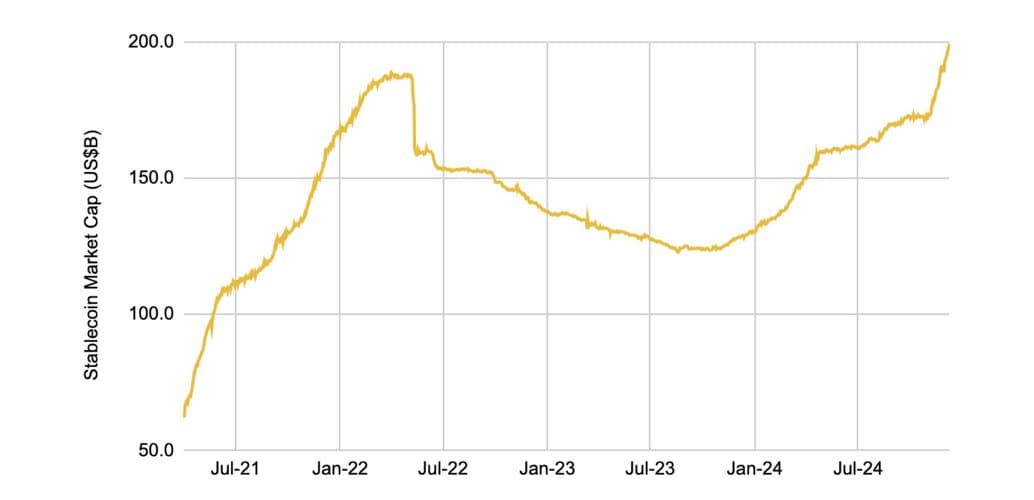

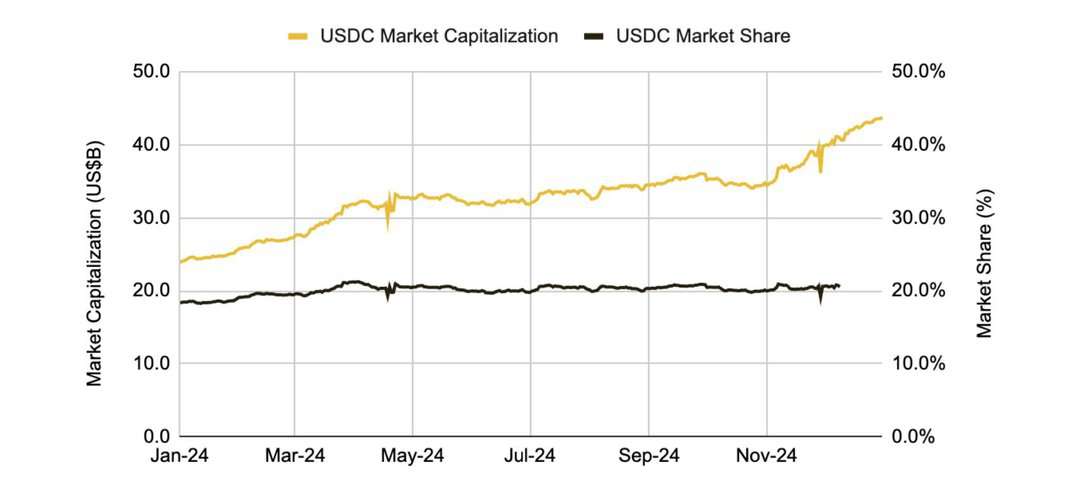

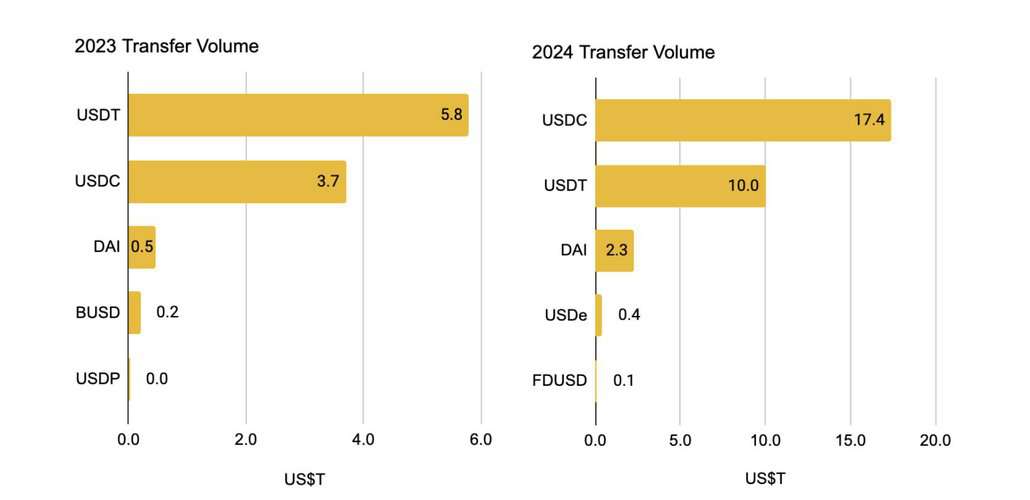

● The stablecoins market experienced remarkable growth in 2024, reaching an all-time high market cap of US$205B and ended the year just slightly lower at US$204B, representing a 56.8% YoY increase. USDT, the leading stablecoin, saw a 50.2% increase in market cap but lost some market share to USDC, which grew by 82.4% and experienced a 3% absolute increase in market share. Ethena’s USDe, launched in December 2023, quickly became the third-largest stablecoin with a market cap of approximately US$5.9B.

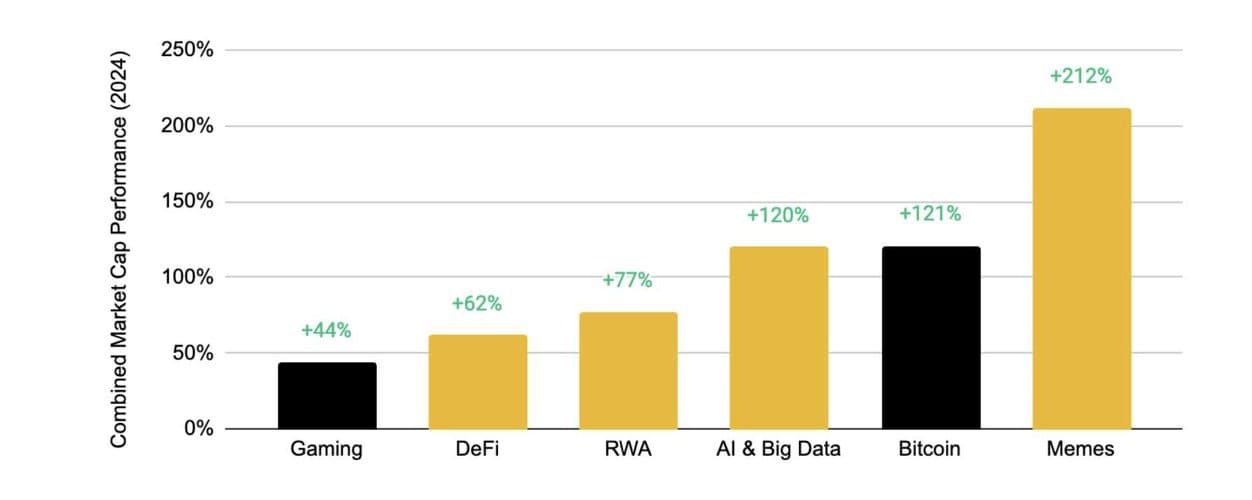

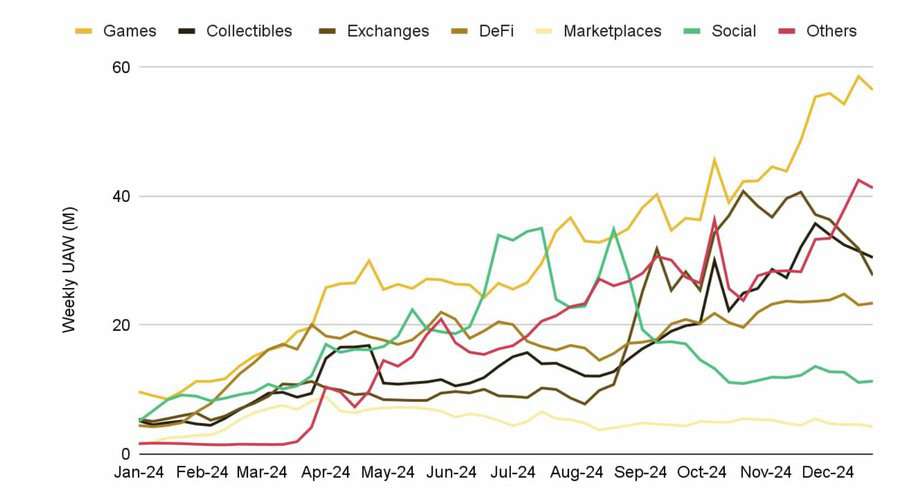

● In 2024, the gaming sector experienced modest growth, with the total gaming token market cap increasing by 44%, underperforming the overall crypto market which grew by 96.2% YoY. Despite the relatively slower pace of growth, the Web3 gaming industry saw notable developments. The number of unique active wallets (UAWs) interacting with games increased by 580% throughout the year, reaching over 50 million by year-end. Additionally, hundreds of new titles were announced across major gaming ecosystems and platforms, with standout titles like “Off the Grid” bringing Web3 gaming into mainstream appeal for the rst time.

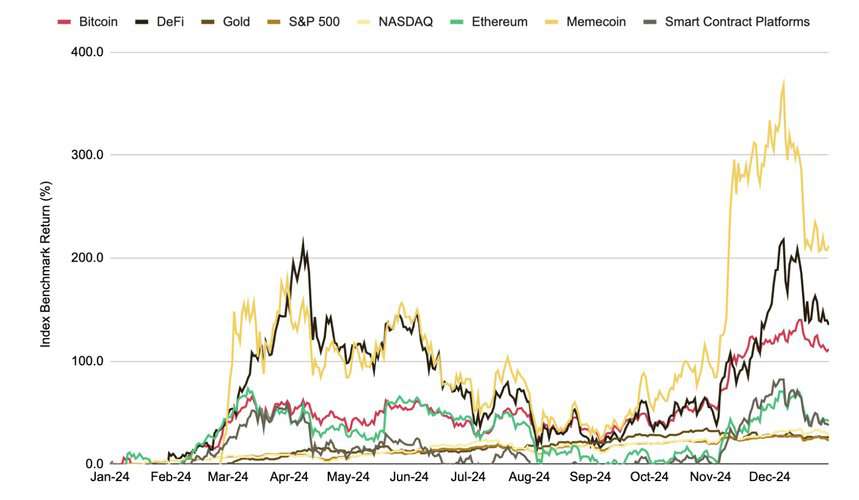

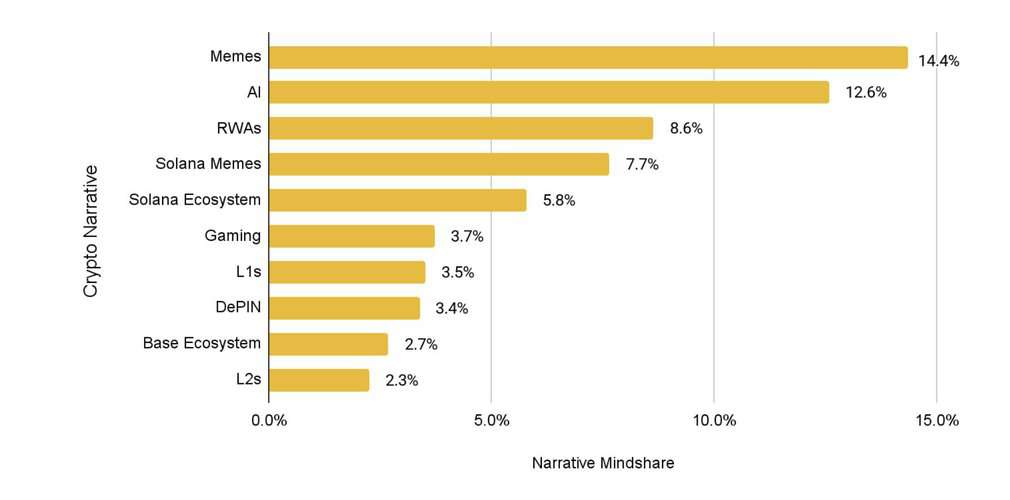

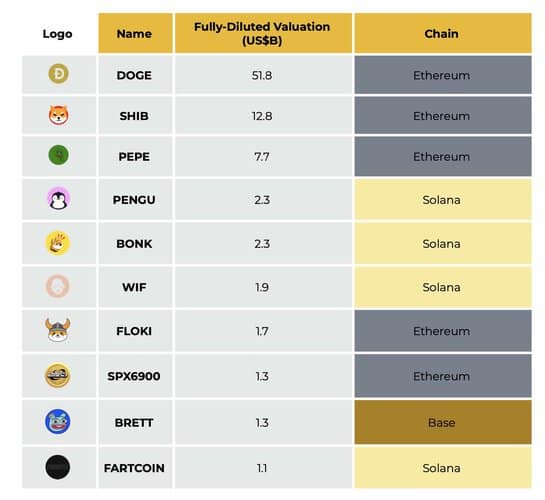

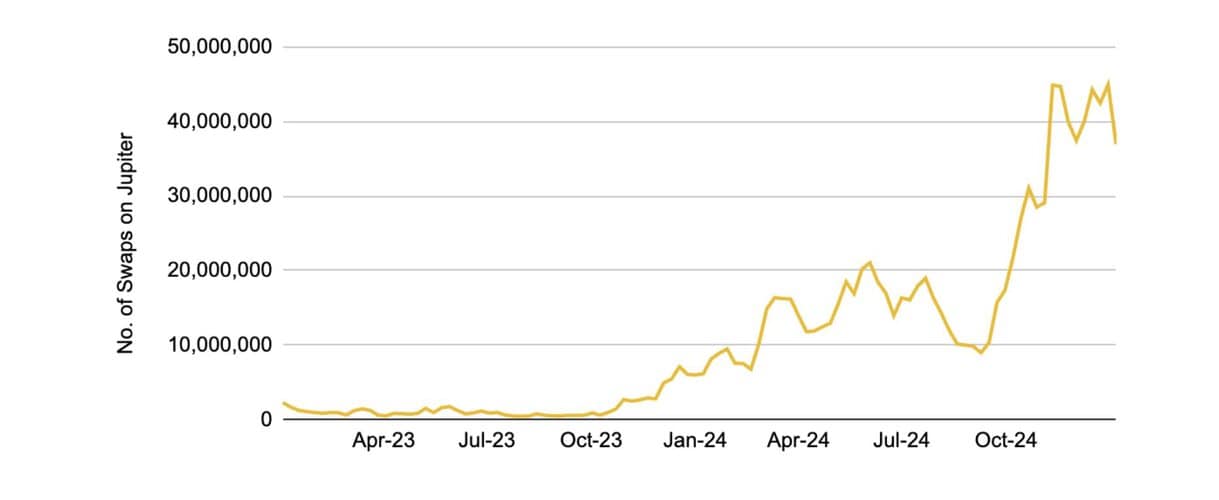

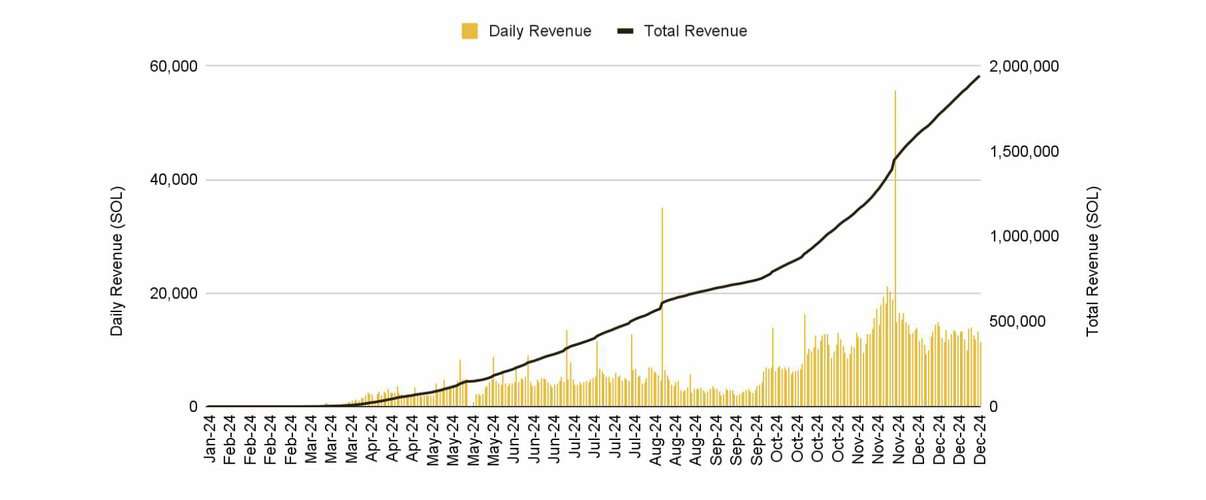

● Memecoins were the top performing crypto sub-sector in 2024 (+212%) and dominated mindshare. The top memecoins are split between Solana and Ethereum, although Ethereum still hosts the top three, including Dogecoin, which is in its fourth cycle. Solana has become the default memecoin trading chain, driven by a cohesive and unfragmented product suite and consistently cheap fees. The incredible growth of Pump.fun has also been key to the success, with the memecoin launchpad having seen 5.7M+ memecoins and over US$400M in revenue in 2024.

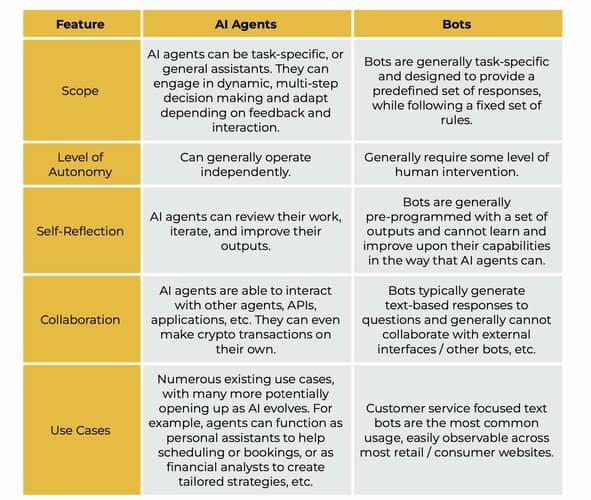

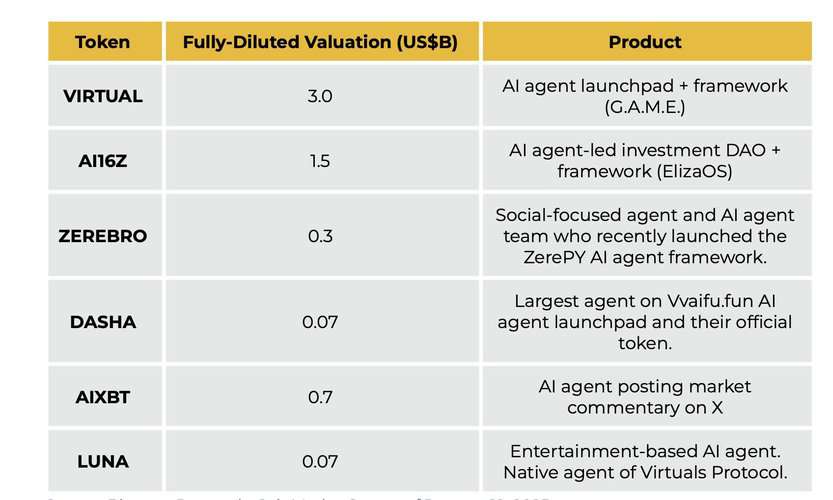

● AI agents, initially sparked by Truth Terminal and $GOAT, have captured the market since October and become a dominant narrative. Infrastructure providers like Virtuals Protocol (G.A.M.E. framework) and ai16z (ElizaOS framework) have been key players. The rst agents have largely focused around market commentary (aixbt) or entertainment (Luna, Eliza), with lots more in development. Swarms (groups of agents), the entry of web2 into AI agents, and the rapid development and anticipated trajectory of AI x crypto, are key areas to watch.

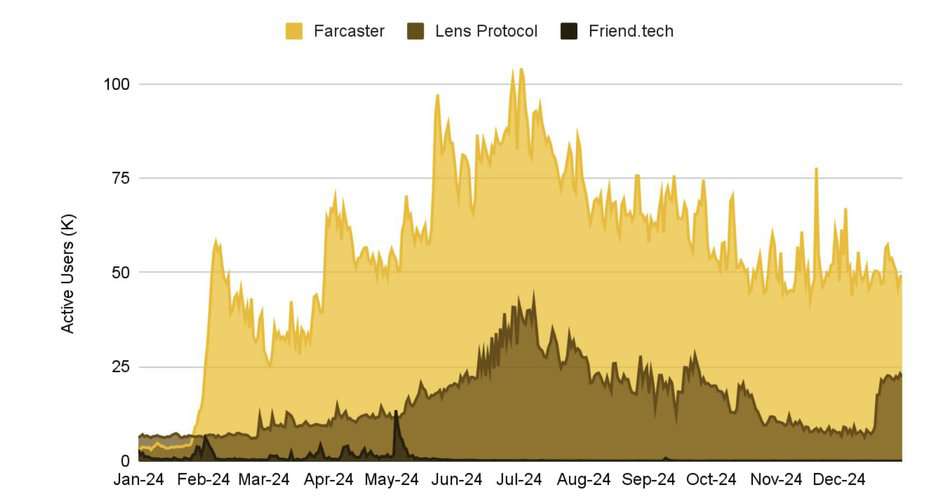

● While speculation-driven SocialFi platforms initially spurred user growth, 2024 became a year of consolidation for Decentralized Social (DeSoc). Daily UAWs fell from Full-Year 2024 & Themes for 2025 5 a peak of 35.0M in July to 11.3M by year-end, underscoring the persistent challenges of user retention for DeSoc products. However, dApps on social networks like Farcaster showed steadier growth, emerging as bright spots in the sector. These platforms shifted toward developer-centric value propositions — focused on front-end composability, distribution, and integration into existing UX through products like Frames and Blinks — which could play a key role in driving adoption in 2025.

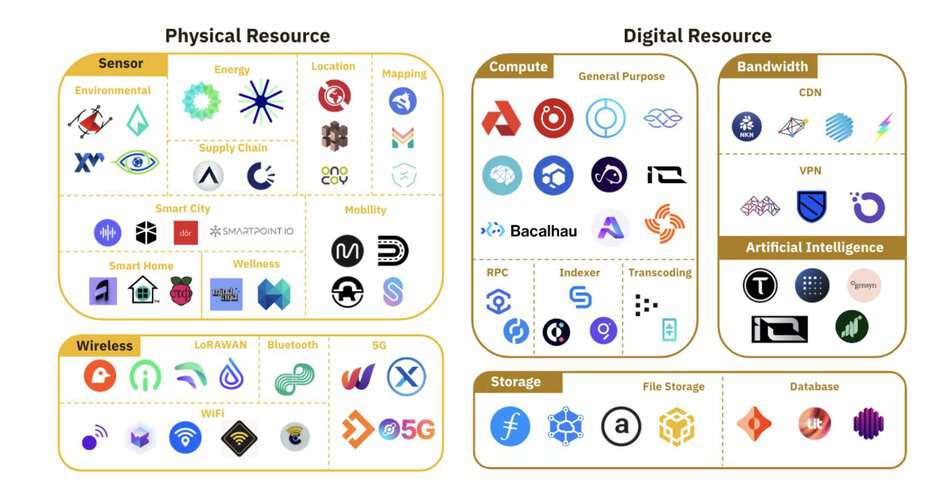

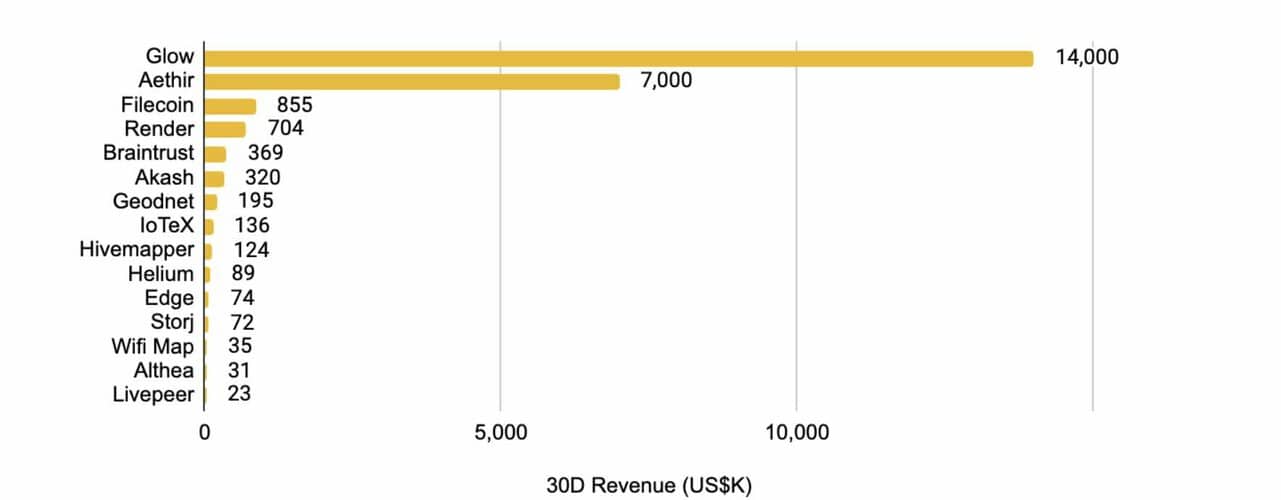

● DePIN has demonstrated real-world applications in areas such as compute, telecommunication, and energy, attracting notable interest and investment. Despite a diverse landscape with 249 projects, some DePIN initiatives face challenges in generating meaningful revenue, indicating varying levels of demand.

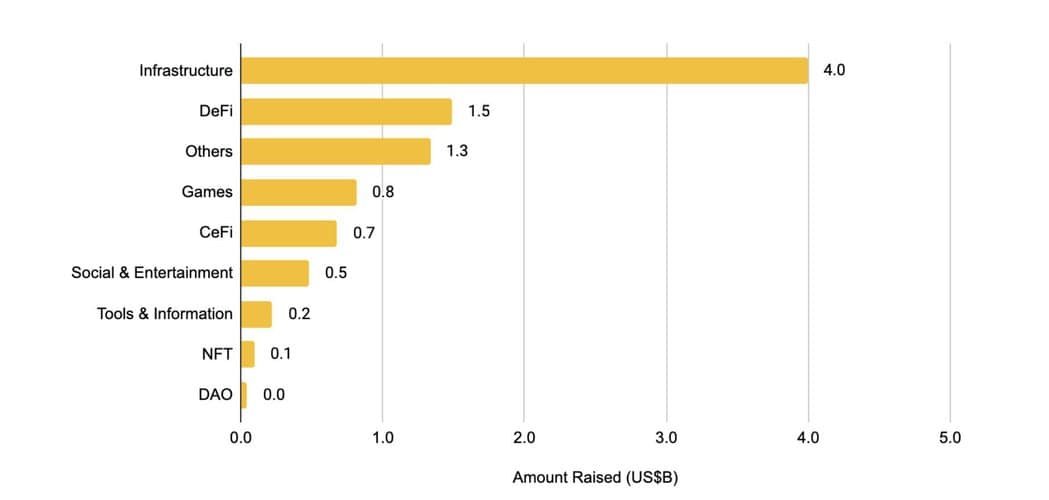

● Web3 projects attracted a total of 1,432 investments, amassing a collective capital of US$9.2B in 2024. Of this, nearly US$4B was invested in infrastructure projects, accounting for around 44% of total funds raised in 2024. This was followed by DeFi with US$1.5B (16% of funds raised) and Games with US$0.8B (9% of funds raised).

● In 2025, eight key themes are particularly exciting to us, and we anticipate signicant progress in these areas throughout the year. These themes span various narratives and sectors, such as those related to the macro environment, Bitcoin ecosystem, articial intelligence (AI), yield-bearing stablecoins, and more.

Overview

2024 marked the second consecutive year of strength for the crypto industry, with total crypto market capitalization rising by 96.2% year-on-year, following a 108.6% rise in 2023. Notably, the crypto market surpassed its all-time high, reaching a peak of US$3.9T, before closing off the year at US$3.4T. The growth was driven by advances recorded in the rst and fourth quarters of the year, which posted gains of 59.5% and 40.7% respectively.

Figure 1: Total crypto market capitalization rose by 96.2% in 2024

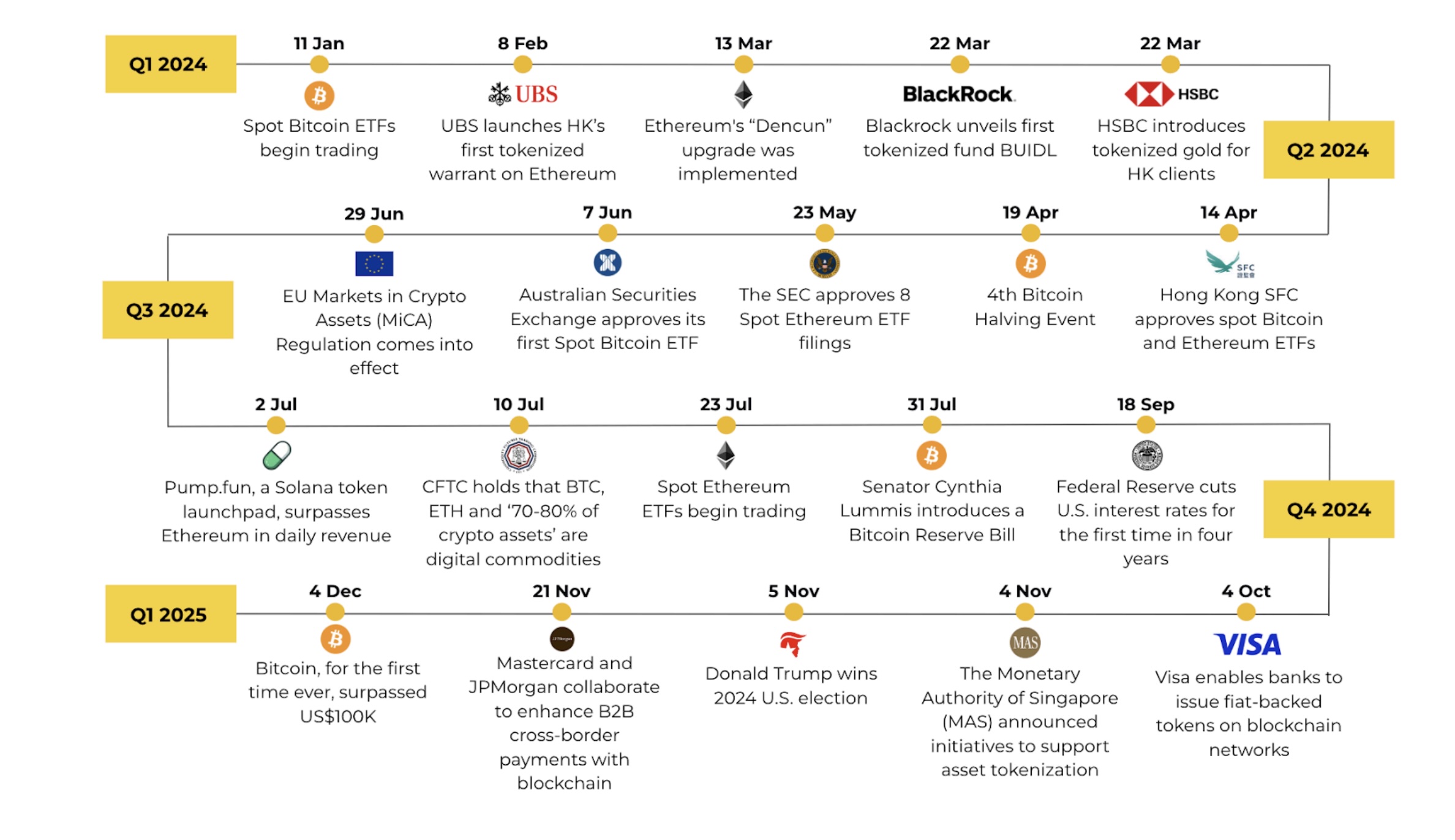

The successful launch of spot BTC exchange-traded funds (ETFs) in the U.S. in January marked a pivotal moment for the industry and ushered in a period of bullish sentiment and positive ows. While the initial price reaction was muted, the following months saw strong gains as the market digested the impact of the ETFs on attracting new capital, increasing accessibility to a greater pool of investors, and reinforcing the growing acceptance of crypto as a mainstream investment.

Favourable macro conditions, spurred by the U.S. Federal Reserve’s rst interest rate cut since 2020 in September reignited investor sentiment in the latter part of 2024, driving risk assets such as equities and crypto to new highs. Sentiment was further lifted in November following the U.S. Presidential election with investors anticipating favorable regulatory shifts for digital assets, propelling total crypto market capitalization past US$3T for the rst time since 2021.

In the rst half of the year, various narratives gained momentum, including the points meta, restaking hype, memecoin frenzy, and airdrops. However, the second half was Full-Year 2024 & Themes for 2025 predominantly characterized by increased activity and attention around memecoins, AI developments, and stablecoins. These narratives are explored in greater detail in the subsequent sections of this report.

Figure 2: Timeline of notable events in 2024

Looking ahead, we are keeping a close eye on global monetary policies, post-election regulatory changes in the U.S., institutional involvement in crypto, the growing intersection of crypto and AI, and the emergence or resurgence of crypto-specic narratives. We are cognizant of the structural overhang of a large amount of upcoming unlocks in the foreseeable future, and we urge investors to do their own research. On the bright side, it is clear that market participants are increasingly aware of this trend and project teams have also experimented with novel ways to raise funds in a more equitable manner.

Layer 1s

Bitcoin

Figure 3: Bitcoin metric performance year-on-year

Bitcoin Dominance and Sentiment

The general sentiment around Bitcoin has continued to improve across the year, with the approval of the U.S. spot ETFs in January spreading this feeling to a wider institutional audience. This positive sentiment has been reflected in Bitcoin’s steadily increasing market dominance, which reached nearly 60% this year, a level unseen since early 2021.

As a reminder, Bitcoin dominance measures the relative market share of Bitcoin compared to the rest of the market. This is calculated using Bitcoin’s total market capitalization (market cap) over the total market cap of all cryptocurrencies combined.

Figure 4: Bitcoin market dominance reached ~60% this year, a level unseen since March 2021

Performance Versus Traditional Assets

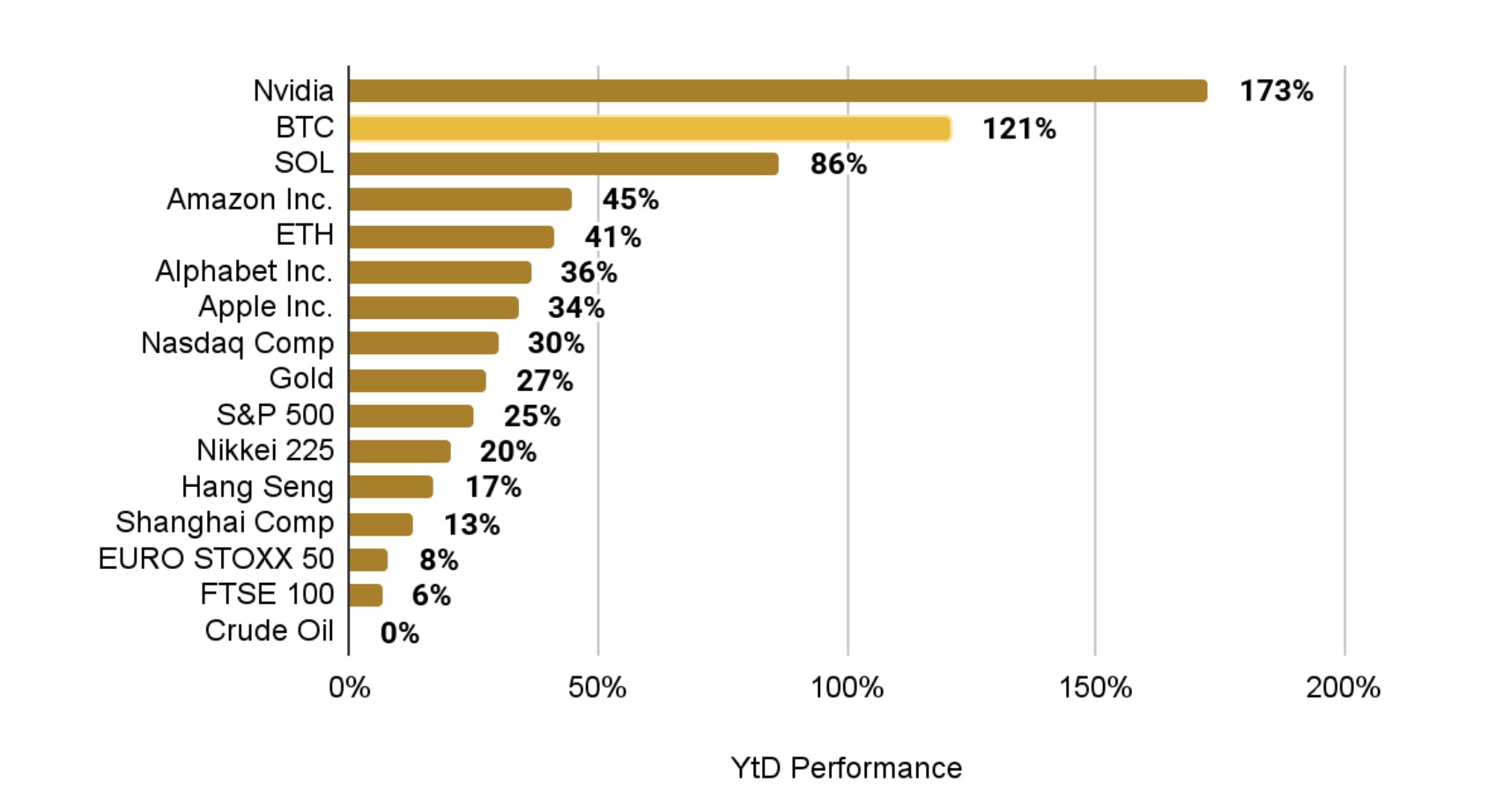

Comparing Bitcoin’s performance to other major investments, Bitcoin (+121% ) ranks second only to Nvidia (+173%) in 2024 returns. Solana is close behind at 86%, while Ethereum ranks among the top five at 41%. Amazon, Alphabet, and Amazon’s equities were the only other investments in our comparison group that were up over 30% in 2024.

The major stock market indexes were further behind, with some displaying single-digit returns. Gold, the commonly touted Bitcoin alternative, rose only 27% , while crude oil had a flat year. This chart highlights how incorporating Bitcoin into a portfolio can enhance diversification and improve overall performance when compared to a solely traditional asset mix.

Figure 5: Bitcoin and Nvidia led 2024 returns among a basket of major assets

Spot ETF

One of the defining narratives of 2024 was the approval of spot BTC ETFs in the U.S. in January. These helped to add a new source of institutional demand to the Bitcoin market, a factor that has enhanced the diversity and depth of investment interest compared to previous cycles. U.S.-based institutional investors, from hedge funds to pension funds, now have a simpler, more direct, and straightforward way to access crypto markets. Since the ETF structure is familiar and comfortable for institutional investors, it is thus an ideal way to introduce conservative investors to crypto markets.

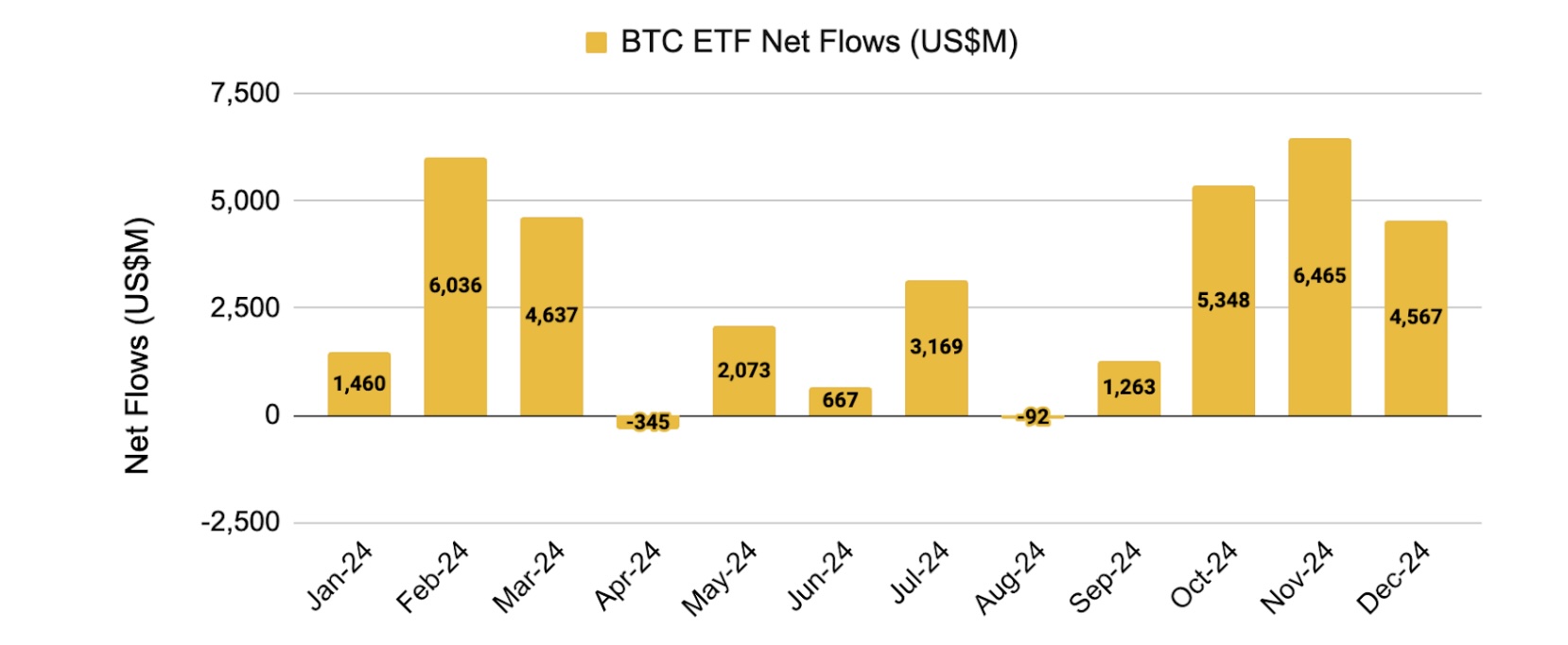

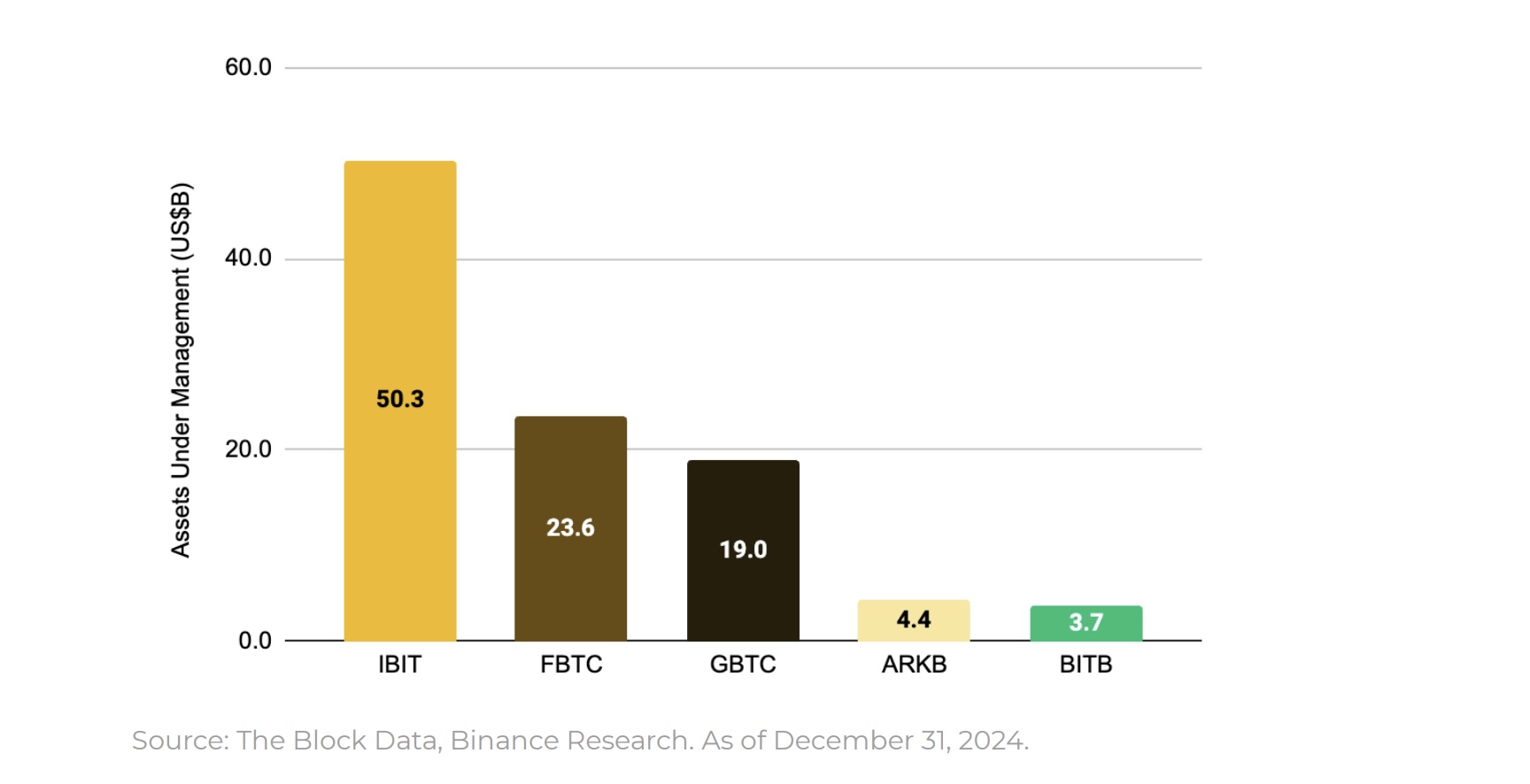

Overall, the Bitcoin ETFs have recorded US$35B+ of net inflows since the January 2024 launch, with volumes having surpassed US$650B, while total assets under management is over US$105B. November was a particularly strong month, seeing approximately US$6.5B of net inflows, including a record-breaking week from November 18–22, which brought in US$3.3B.

Figure 6: The spot Bitcoin ETFs ended the year on a high, seeing over US$11B of net inflows in November and December

This surge in adoption is led by BlackRock’s iShares Bitcoin Trust (IBIT), which boasts over US$37B in cumulative inflows and ~US$50B in assets, commanding nearly 50% of the market. Fidelity’s offering follows as the second largest, managing US$24B in assets from US$12B in net inflows. Together, these two giants dominate the Bitcoin ETF space, reflecting growing institutional confidence and interest in crypto investment products

Figure 7: BlackRock, Fidelity, and Grayscale command the majority of the U.S. spot BTC ETF market by AUM

Interest has also spread internationally. Hong Kong approved spot Bitcoin and Ether ETFs in April 2024, marking progress despite relatively limited volumes compared to the U.S.. Meanwhile, European crypto ETPs — roughly equivalent to U.S. spot ETFs and available since 2015 — are experiencing significant growth, with total AUM rising ~97% from ~US$9B in 2023 to over US$17B in 2024.

Two key factors could drive bullish momentum for Bitcoin ETFs in 2025. First, the one-year anniversary of U.S. spot ETFs marks a potential turning point. While traditional investors were initially cautious when onboarding crypto, the performance in 2024 has likely built confidence. This could prompt more investors to diversify into Bitcoin ETFs in the coming months.

In addition, the recent presidential victory of pro-crypto Donald Trump has heightened bullishness across the U.S. (especially with regards to Bitcoin). Following this sentiment, Bitcoin broke the US$100K mark, with ETF flows reaching yearly highs after the election victory. We may see more of this sentiment come through in the coming months which may result in further traditional investor involvement. With a relatively low barrier to entry, Bitcoin ETFs offer traditional investors a simple way to dip their toes into crypto. As a result, we expect ETF flows to continue growing .

The Halving

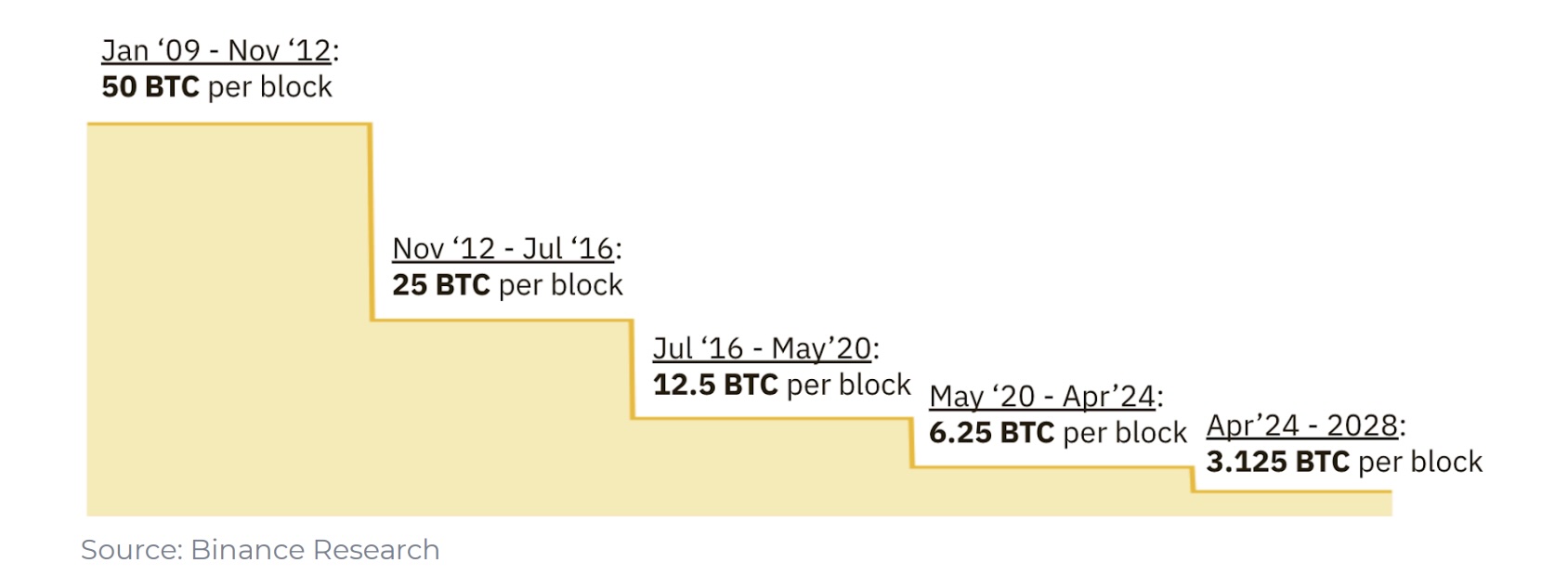

Bitcoin operates on a fixed issuance schedule, a key feature of its appeal. A set amount of Bitcoin is rewarded to miners for validating each block, known as the block reward. Every 210,000 blocks — approximately every four years — this reward is halved, reducing the rate of new Bitcoin issuance by 50%.

This event, called the “Bitcoin Halving,” is a pivotal moment in the crypto world. As Bitcoin has a capped supply of 21 million, the halving plays a critical role in its monetary policy, with significant implications for miners, investors, and the broader market. For a deeper dive, check out The Future of Bitcoin #1: The Halving & What’s Next .

Figure 8: Bitcoin’s block reward has decreased from 50 BTC per block to 3.125 BTC per block across its first four Halving events

Given that Bitcoin miners derive the majority of their income from the block reward, the Halving represents a direct ~50% reduction in their income. This has major revenue implications for miners and has historically led to some level of revenue diversification and industry consolidation. Since the April 2024 Halving, we have observed an increasing trend of miners diversifying into providing AI and high performance computing (HPC) infrastructure, as well as, larger miners attempting to acquire or merge with smaller competitors. We will likely see a continuation of this in 2025, especially with regards to providing AI-related computational power and services.

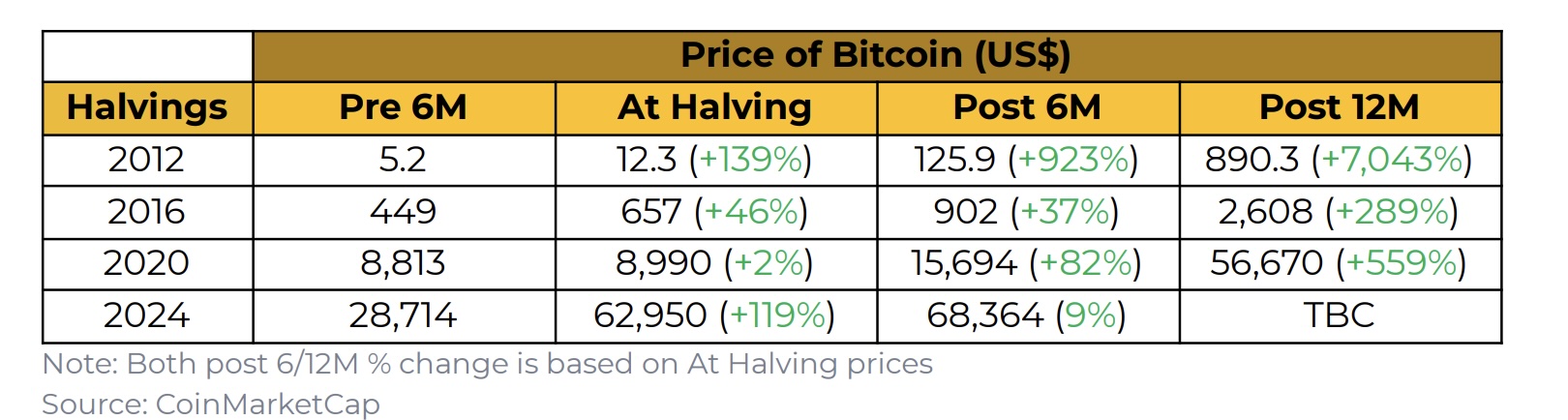

The Halving likely doubles as a global campaign emphasizing Bitcoin’s inflation-resistant, self-enforced monetary policy. It highlights Bitcoin’s fixed supply and growing demand, drawing attention to its scarcity. At a time when Bitcoin is more accessible to investors than ever, the Halving reinforces its unique value proposition.

Figure 9: Each Halving event has been followed by strong BTC performance in the 6-12 months following the event

Bitcoin Ecosystem

While Bitcoin’s traditional utility has largely revolved around it functioning as a form of digital gold due to its immutable monetary policy and fixed supply in a world of ever-inflating fiat currencies, things are changing. Developers have long aimed to expand Bitcoin’s utility, with significant progress seen in 2023 and 2024.

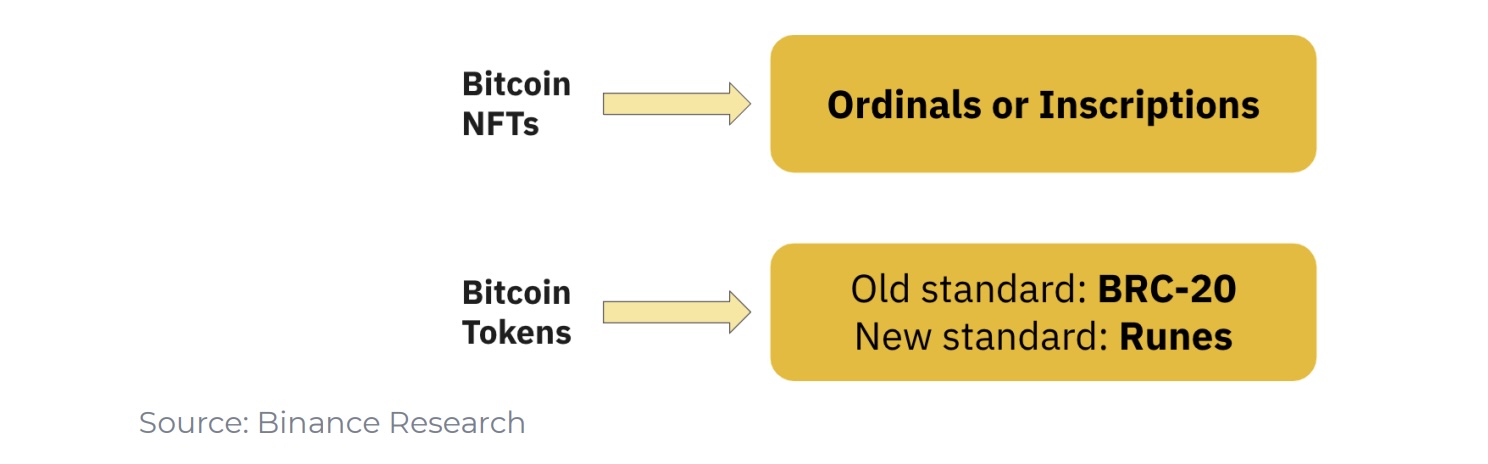

Ordinals & Runes: Casey Rodarmor’s “Ordinal Theory” enabled the tracking of individual Satoshis (the smallest unit of Bitcoin), and ascribed a unique identifier to every single one. These individual Satoshis were then able to be “inscribed” with arbitrary content such as text, images, and videos. This created an “Inscription” or what soon became known as a Bitcoin NFT. Initially launched in late 2022, these saw significant attention across 2023.

In late 2023, the BRC-20 standard was introduced, enabling the deployment, minting, transfer of Ordinal-linked fungible tokens on Bitcoin. Building on this development, the Runes Protocol launched in April 2024, coinciding with the Bitcoin Halving. Created by Casey Rodarmor, Runes offer another approach to creating fungible tokens on the Bitcoin network.

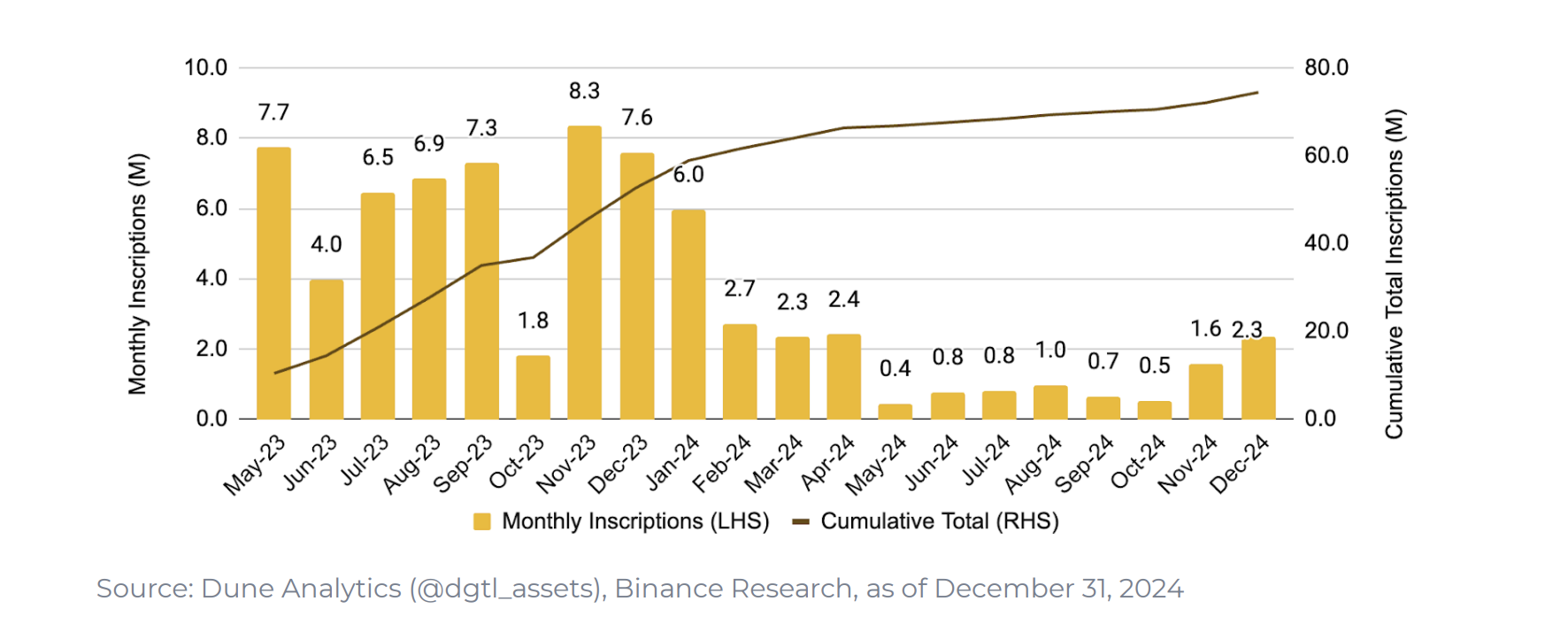

Since the initial launch in December 2022, over 75M Inscriptions have been minted on the Bitcoin blockchain, generating over 6,970 Bitcoin (~US$692M) in fees.

Figure 11: Monthly Bitcoin Inscriptions have declined significantly since the highs of 2023

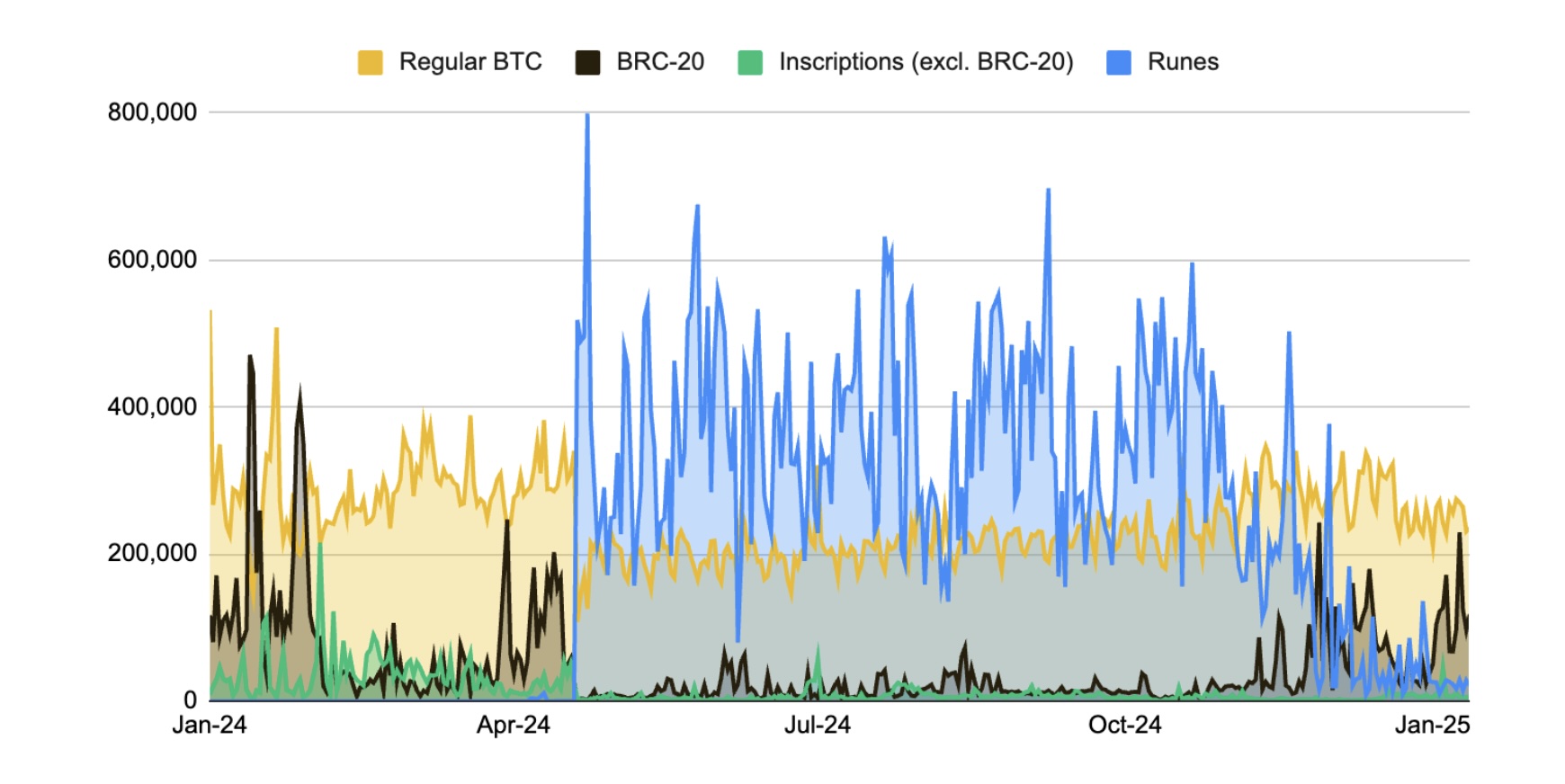

Since their launch, Runes and BRC-20 transactions have accounted for over 49% of Bitcoin’s transaction activity on average. While standard Bitcoin transactions still dominate, new Bitcoin markets have contributed to increased activity and fee revenue.

Figure 12: Runes have represented 49% of all Bitcoin transactions, on average, since their launch in April

While not a game changer, the additional hundreds in millions in fees that Inscriptions, BRC-20s, and Runes have generated are surely welcome. This is especially important in light of the recent Bitcoin halving. As a reminder, Bitcoin miners are compensated in two different ways: block rewards and transaction fees, with the block rewards halving every four years. The April 2024 halving reduced this from 6.25 BTC to 3.125 BTC. Thus, an increase in transaction fees is required in order to sustain the miners, given the block reward will eventually reduce to zero.

Layer 2s (L2s): One of the indirect effects of Ordinals, BRC-20s, and Runes has been the ushering in of a new renaissance for Bitcoin expressivity. However, an issue arises due to the inherent technical limitations of Bitcoin, which does not support smart contracts in the same way as alt-L1s like Ethereum, Solana, and BNB Chain does. What this means is that a lot of work is being done on creating alternative layers for Bitcoin expressivity, i.e., Bitcoin L2s.

Various teams are working on solutions, including long-standing teams such as Lightning Network, Stacks, and RGB. Newer teams are also emerging with innovative solutions, including Citrea and Merlin’s Bitcoin zk-rollups.

While some teams have launched testnets, many are still in the development phase. We expect to see further launches and traction in 2025.

Also worth mentioning is the introduction of BitVM and BitVM 2. BitVM’s goal is to scale the Bitcoin network through introducing smart contract capabilities, without requiring significant changes to Bitcoin’s existing infrastructure. BitVM operates somewhat similarly to how we understand optimistic rollups on other L1 chains. Development around this protocol may help expand Bitcoin’s capabilities far ahead of where they are now, and also help create a more secure way to bridge BTC to secondary layers. Although it is relatively early in BitVM’s history to see where it will go, this is an important area to keep up with through 2025.

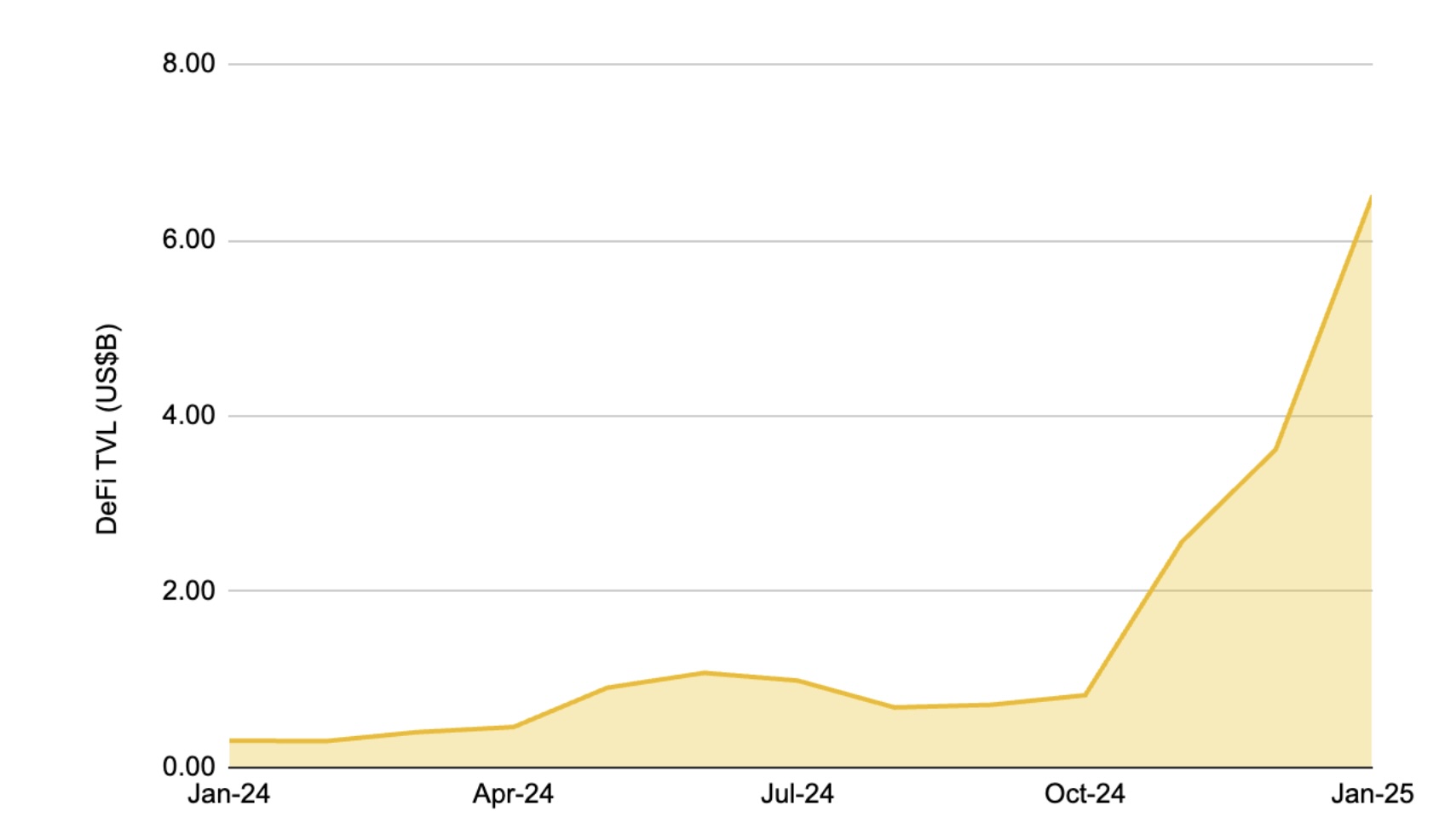

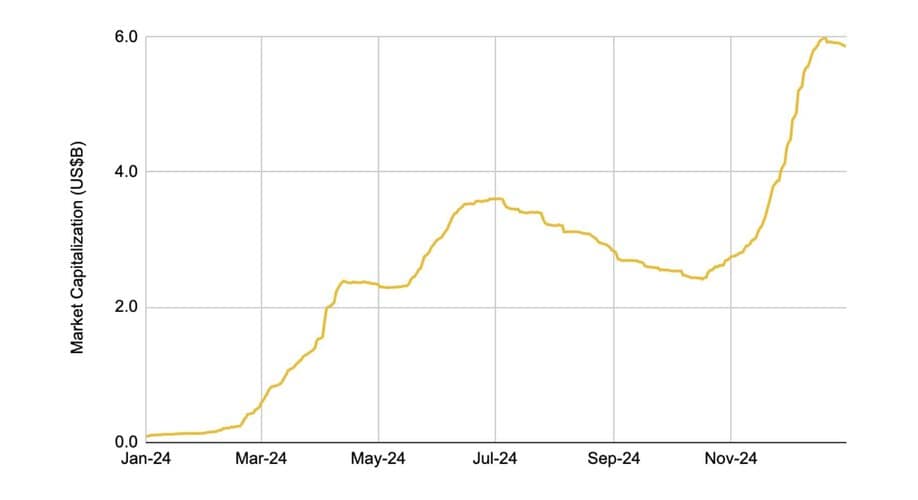

DeFi: The Bitcoin DeFi or BTCFi space is another to keep a close eye on. 2024 was a breakout year for the sector, with TVL growing by over 2,000% from US$0.3B to over US$6.5B, cementing Bitcoin’s place among the top five DeFi chains.

Figure 13: Bitcoin DeFi total value locked (TVL) grew by over 2,000% in 2024

Numerous new BTCFi projects have either launched in the last year, or are currently being funded and developed. A significant amount of TVL is associated with the Bitcoin restaking platform, Babylon, which commands ~82% of the BTCFi market. Babylon utilizes a timestamping protocol in order to leverage the immense crypto-economic security of Bitcoin to secure other proof-of-stake (PoS) chains.

Various other projects, from Bitcoin money markets, to Bitcoin DEXes & AMMs are also in different stages of development. We are likely to see this activity continue to bump up across 2025, with many more product launches expected.

What may 2025 bring?

There are a number of catalysts for Bitcoin (and the broader crypto ecosystem) as we head into 2025. A key driver here is the U.S. and what is expected from the incoming Donald Trump government.

Given Donald Trump has multiple NFT collections and a DeFi project, and a record number of pro-crypto have been elected officials across the House of Representatives and Senate, U.S. crypto regulation developments are expected in 2025. Enacting clear regulation of digital assets is expected to bring more clarity to TradFi institutions and benefit existing crypto ETFs and potentially allow for more to be created.

Taking into account the U.S.’ major position across global financial markets and improved sentiment towards crypto, similar developments in many other countries across the world are expected to follow. Focusing specifically on Bitcoin:

Strategic Bitcoin Reserve: This was a product of Senator Cynthia Lummis’ bill to create such a reserve in the U.S. and has been mentioned numerous times by Donald Trump during his Presidential campaign trail.

Interestingly, a number of different U.S. states are working on their own legislation to create Bitcoin reserves on a state-level. This includes Pennsylvania, Florida, Ohio, and Texas.

Perhaps even more importantly, the issue is being discussed in various nations globally. There has been discussion and bills proposed in Brazil, the Czech Republic, Poland, Russia, with speculation in other countries including China.

There has been a rise in corporate Bitcoin adoption, with many firms joining MicroStrategy in adding Bitcoin to their treasuries. This includes the likes of Semler Scientific, Metaplanet, Genius Group, etc. Many Bitcoin miners, including Riot and Marathon, have also been purchasing more Bitcoin for their treasuries, while others like streaming company Rumble are also considering implementing the strategy.

More Ecosystem Development: As we mentioned previously, there is significant traction across Bitcoin L2s, Bitcoin DeFi, and other parts of the ecosystem. With increasing global attention on the largest cryptocurrency, as well as increasing flows from traditional investors (owing to the ETFs), we expect to see further development across the broader Bitcoin ecosystem in 2025.

Bitcoin Improvement Proposals (BIPs): BIPs are formal proposals sent to the Bitcoin community describing potential new features that could be added to Bitcoin. For example, Bitcoin’s last two major upgrades, SegWit (2017) and Taproot (2021) implemented a number of BIPs into Bitcoin. These upgrades were essential to the creation of Ordinals, BRC-20s, and Runes.

An important BIP to track is BIP-347, which seeks to implement OP_CAT to Bitcoin. To put it very simply, OP_CAT can allow Bitcoin to combine two pieces of data during a transaction, potentially unlocking smart contract capabilities across the network. OP_CAT is one of many “covenant” proposals, which create additional conditions and rules around how Bitcoin can be spent, thereby creating the possibilities for more advanced logic within the network.

Although Bitcoin traditionally moves very slowly and carefully, covenants have been discussed for over ten years and have received renewed attention over the last couple of years following the Ordinals-led boom. It will be interesting to watch if one or more new BIPs can be introduced or at least gain further traction across 2025

The Other L1s

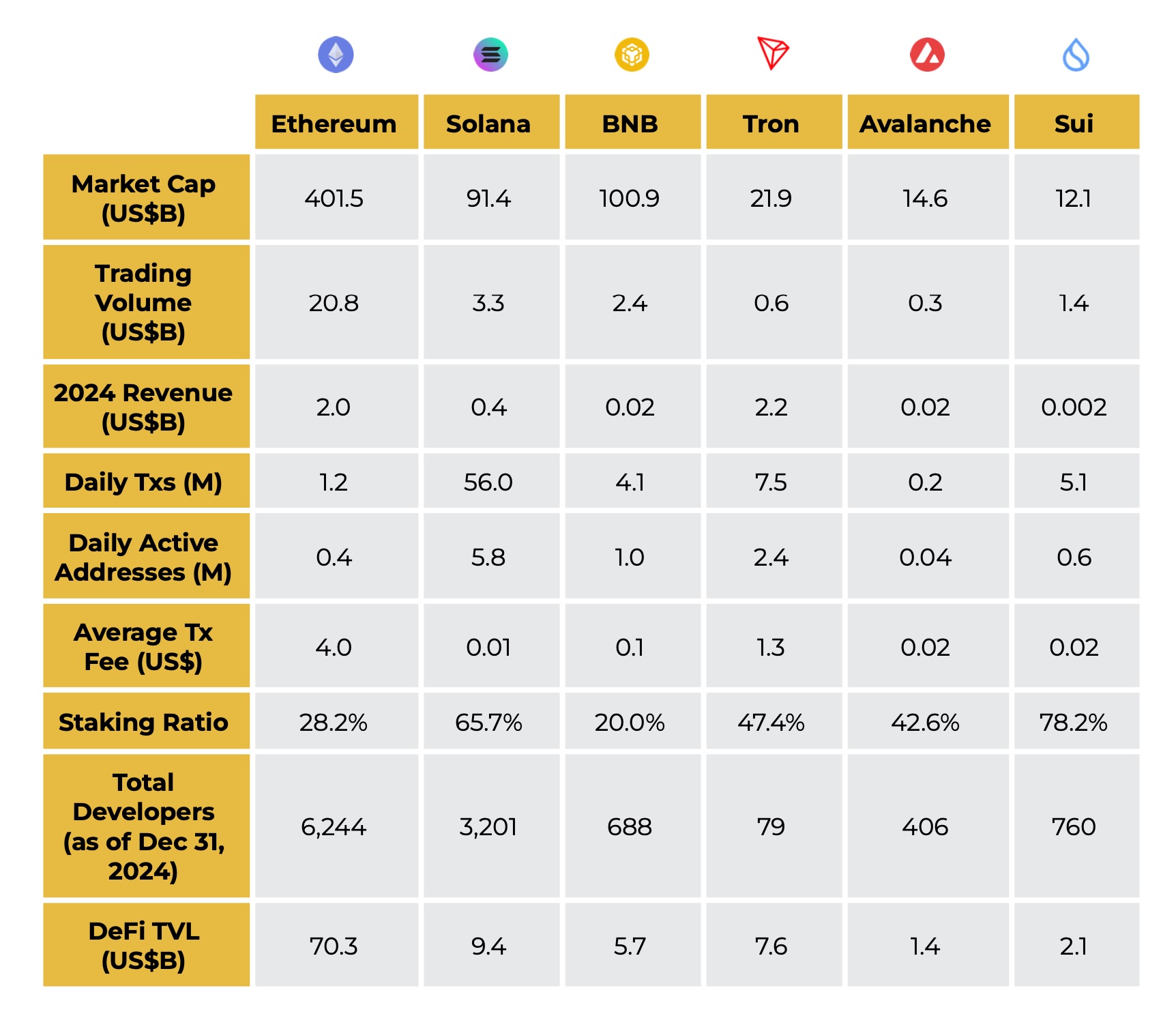

Figure 14: A summary of where things stand for the major L1s at the end of 2024

When looking at the high-level metrics, it is clear that Ethereum remains in a position of strength and leads on numerous fronts including market cap, trading volume, DeFi TVL, and total developers. On the other hand, activity metrics such as daily transactions and active addresses are dominated by Solana, which also offers the lowest average transaction fee. Developer numbers are interesting to note, with Ethereum leading by a large margin, followed by Solana with roughly half of Ethereum. BNB Chain, Sui, and Avalanche show comparable numbers, while Tron’s developer community remains smaller. Tron led on 2024 revenue, no doubt helped along by its dominance in stablecoin transactions.

Ethereum

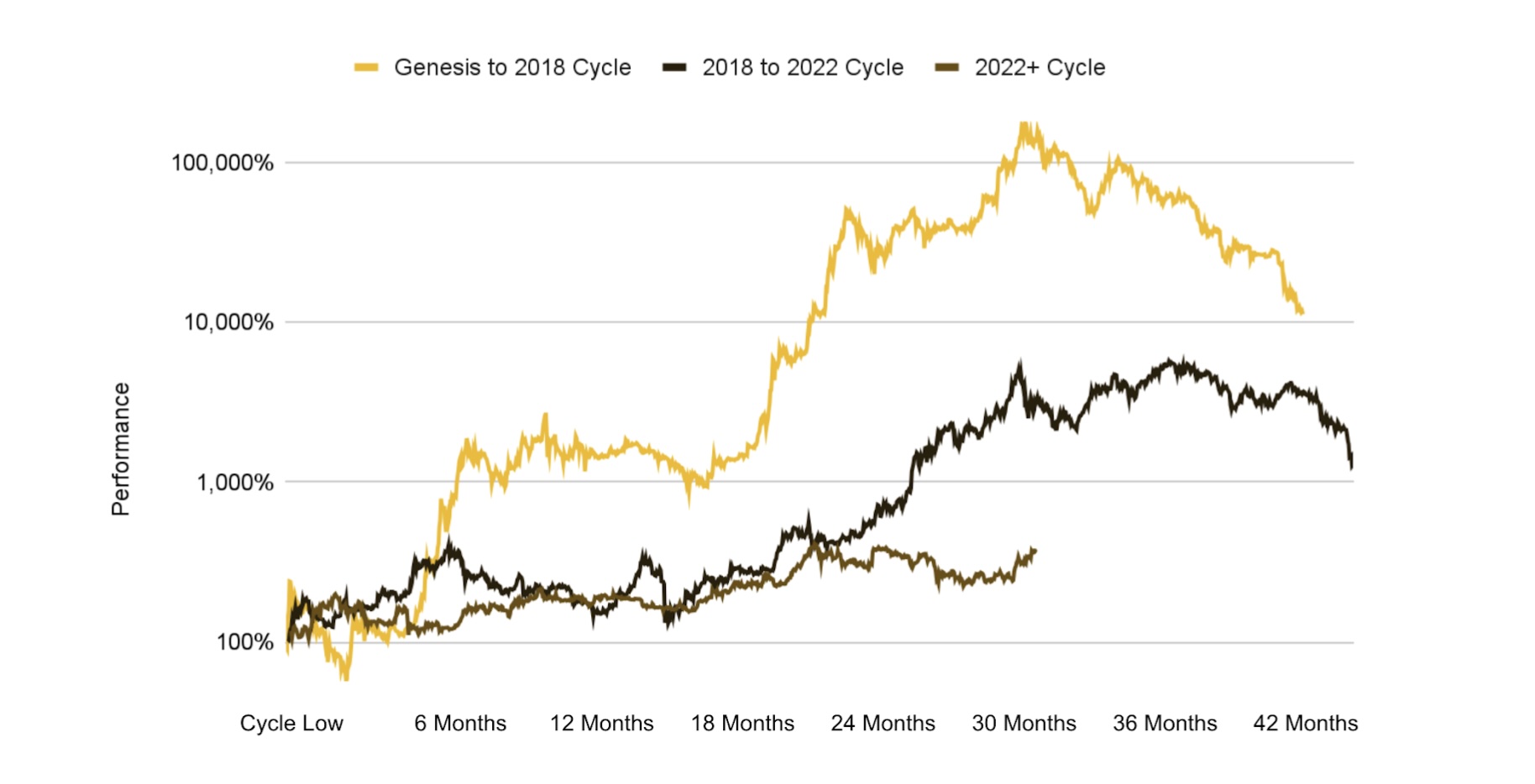

Ethereum had an interesting 2024. There were some interesting developments with regards to restaking, its growing rollup universe, and the U.S. spot Ether ETFs. At the same time, Ether as an asset significantly underperformed against other major bluechips like Bitcoin and Solana, and the majority of the top 30 tokens by market cap.

Figure 15: Current ETH Performance Lags Behind Previous Market Cycles

The Impact of Dencun

Ethereum’s Dencun hard fork went live in March 2024, introducing various changes to the network. The most anticipated was EIP-4844 (a.k.a. proto-danksharding), allowing users to benefit from lower gas fees on L2 transactions. This was a major milestone for Ethereum’s road to scalability and lays the groundwork for full danksharding in the future.

Specifically, EIP-4844 introduced “blobs,” which provide L2s with a more gas-efficient way to post transaction data. Blobs drastically reduced fees for posting data to Ethereum’s L1, enabling L2s to support higher transactions per second (TPS) and attract increased user activity. Blobs achieve this by storing the bulk of data off-chain and employing a pricing mechanism called “blob gas” that operates independently from Ethereum’s gas market. Additionally, data is stored temporarily for around two weeks rather than permanently.

Figure 16: L2s are capturing a growing share of transaction activity

While the growing adoption of L2s demonstrates the success of Ethereum’s rollup-centric roadmap, it also had a reverse effect. Critics argue that as L2s capture a larger share of transaction and user activity, economic value is being redistributed, shifting away from Ethereum’s L1.

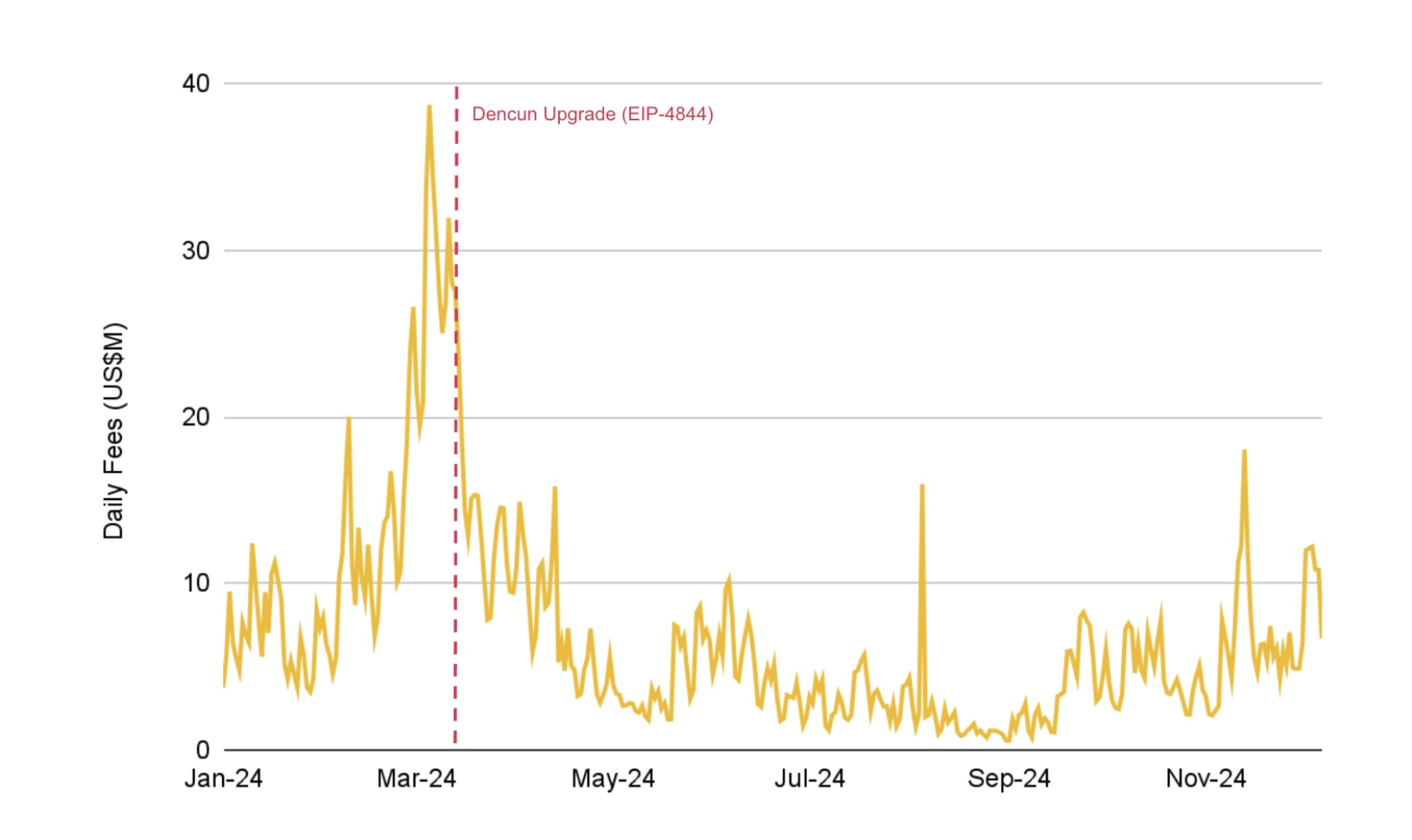

The evidence for this criticism is clear when we consider Ethereum’s transaction fee revenue, which has taken a notable hit. In fact, Ethereum’s fee collections have reached their lowest levels in years, despite the ongoing bull market and increased activity.

Figure 17: Following Dencun, Ethereum network fees have trended generally downward

There is also the matter of increasingly fragmented liquidity driven by the plethora of Ethereum L2s. Due to general interoperability challenges across crypto, this has contributed to somewhat complex user experiences. For example, how does one explain the difference between Arbitrum USDT, Base USDT, zkSync USDT, and the fact that these are all a form of Ethereum USDT to crypto newbies?

Other than newbies, some seasoned crypto users even expressed fatigue with the sprawling Ethereum L2 ecosystem. In contrast, monolithic and fully integrated alt-L1s, where dApps operate in shared environments and offer Web2-like experiences, have gained traction i.e., Solana. It remains to be seen whether L2s will continue their momentum in 2025 or if attention will shift back to Ethereum L1.

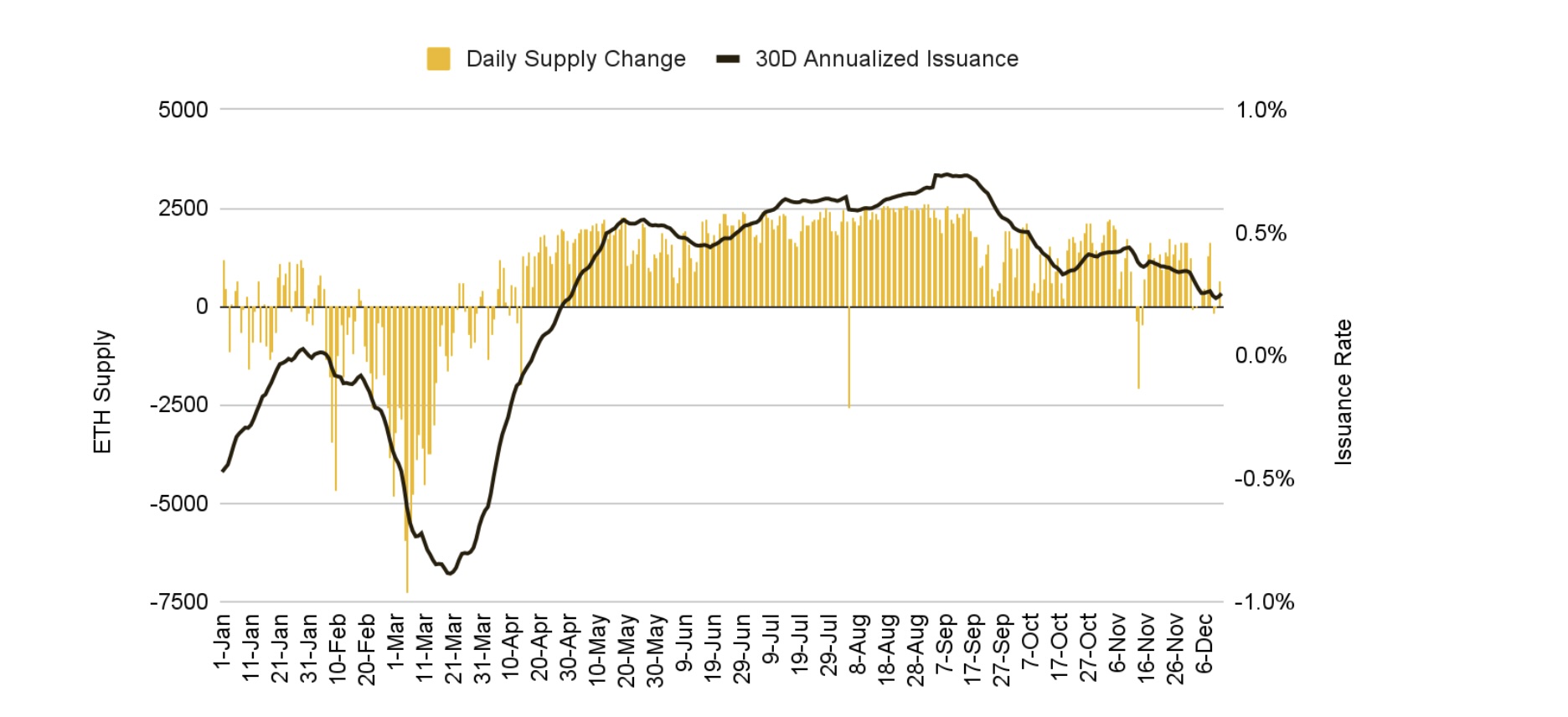

The End of Ultrasound Money?

Lower transaction fees have also impacted ETH’s inflation dynamics. Ethereum’s supply is governed by issuance, staking rewards, and the fee burn mechanism (EIP-1559). “Ultrasound Money” has been a long-standing narrative of many in the Ethereum and EVM communities, whereby the burn effect of EIP-1559 will outweigh the issuance of ETH, making it a deflationary asset. The “ultrasound” is a play on what is often referred to as

Bitcoin’s “sound” monetary policy, which ensures consistent supply. The idea is that Ethereum will be ultrasound as it will be deflationary.

This was initially observed through many parts of 2023, following The Merge in 2022, when Ethereum transitioned to proof-of-stake. However, with reduced fees following the Dencun Upgrade, the ETH burn rate has declined, reversing many of the deflationary trends observed 2023. In fact, ETH issuance reached ~0.74% annually in September, a high not seen in two years, dampening the ultrasound money narrative that many in the Ethereum community pushed in 2022 and 2023.

Figure 18: After Dencun, daily issuance consistently outpaced burns, causing ETH’s 30-day annualized inflation to turn positive

Nonetheless, while recent changes have impacted ETH inflation, such trends should be expected during scaling transitions that increase blockspace supply faster than demand. Ethereum’s issuance rate remains below 1%, far lower than most alt-L1s. Furthermore, cyclical market activity should naturally restore the burn mechanism as demand picks up – something we have started to see in recent weeks. The key risk, however, lies in Ethereum’s ability to maintain consistent blockspace demand across cycles, particularly amid rising competition from alt-L1s and the increasing reliance on L2 activity.

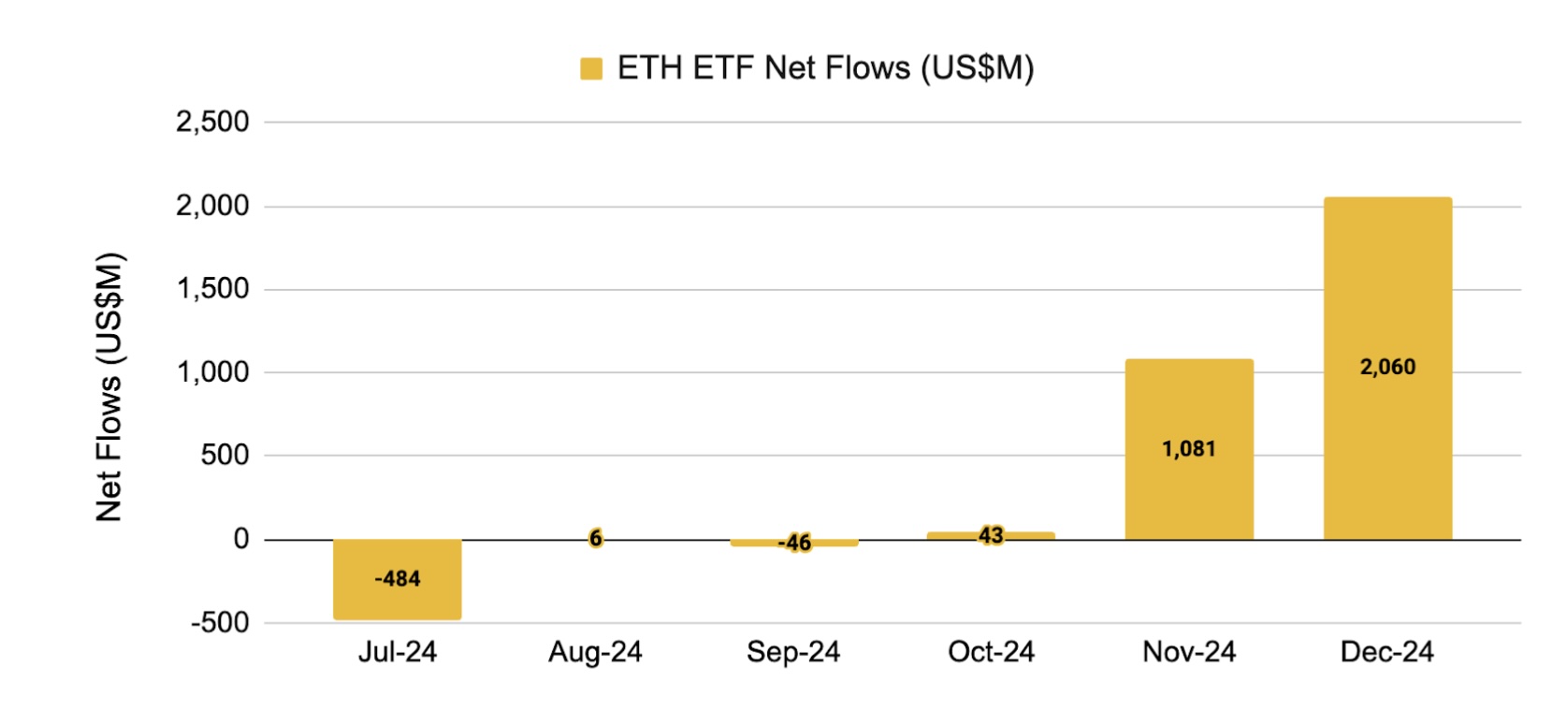

ETF Discussion

The approval of the U.S. spot BTC ETFs in January 2024 was followed by the approval of the ETH ETFs in July. Much of the analysis we conducted for the BTC ETFs is also applicable here. Specifically, creating a new source of institutional demand for ETH.

However, it is important to note that ETH ETF flows remained relatively subdued for much of 2024, recording net outflows until November, after which post-election optimism improved sentiment.

Figure 19: Ether ETFs picked up in November and December, after a slow start

Overall, US spot ETH ETFs received a cumulative US$2.7B in net inflows since their July 2024 launch, an overall success among the broad ETF universe. Total volumes surpassed US$43B, with total AUM upwards of US$11B. November and December were particularly strong months, bringing in over US$1.1B and US$2.1B in net inflows, respectively. While numbers improved significantly by the end of the year, we should note that spot BTC ETFs attracted ~13-14x higher net inflows than the ETH ETFs.

Similar to the BTC ETFs, ETH ETFs stand to benefit from growing institutional interest as traditional finance becomes more comfortable with onboarding new asset classes, bolstered by the recent pro-crypto sentiment due to Trump’s recent victory.

Additionally, there is also an additional catalyst in the form of staking. A key difference between Bitcoin and Ethereum is their respective consensus mechanisms, i.e., Bitcoin uses proof-of-work (PoW), whereas Ethereum uses proof-of-stake (PoS). This means that ETH holders who choose to stake their ETH are able to benefit from a native staking yield (something not available to BTC holders). However, as things stand, those who hold ETH ETFs in the U.S. are unable to stake and earn yield on their holdings. But, given that many in the market expect a more constructive and accommodative crypto environment in the U.S. with the new government, taking yield on ETFs is something that many are expecting to be approved in the coming year. If this occurs, the ETH ETFs will have a unique feature in comparison to their BTC counterparts, and we might expect to see an increase in inflows towards them.

What’s Next?

Pectra Upgrade: Scheduled for early 2025, Pectra consolidates two previously planned upgrades: Prague (focused on the execution layer) and Electra (focused on the consensus layer). Together, Pectra introduces a set of updates designed to achieve three key objectives:

Address critical shortcomings in Ethereum’s PoS protocol. Enhance user experiences for interacting with smart contract dApps. Further advance L2 scalability by increasing Ethereum’s data availability capacity.

While the first two objectives aim to improve Ethereum’s overall functionality, the third reinforces its commitment to the rollup-centric roadmap. Two notable proposals included in Pectra specifically target scaling resources for L2s:

EIP-7742: This proposal allows the Beacon Chain to dynamically adjust the network’s target and maximum blob gas limit without requiring major hard forks.

EIP-7691: This increases the maximum blob count (currently capped at 6 blobs per block with a target of 3), further scaling Ethereum’s DA layer. With a higher blob count, the base blob fee would increase in a more controlled manner during periods of peak demand, enabling smoother price adjustments.

While Pectra’s scope is streamlined (inc. continuation of prior blobspace upgrades), it is not expected to have an outsized impact on ETH value in the short-term. However, beyond Pectra, several forthcoming initiatives may have more direct implications. These include efforts to reduce issuance through stake ratio targeting, improve censorship resistance, and advancing scaling capabilities via Peer Data Availability Sampling (PeerDAS).

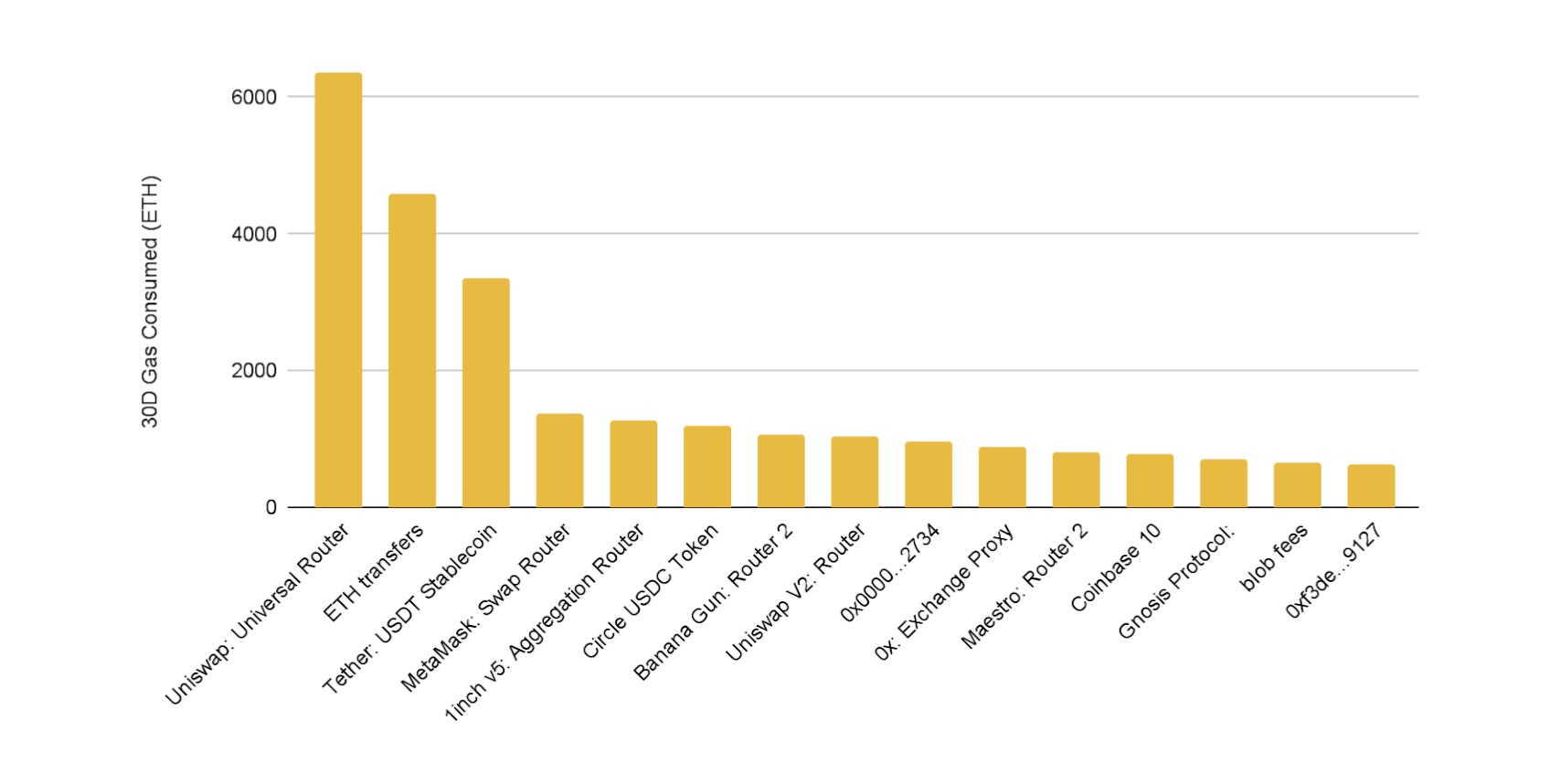

More app-chains? Some dApps have turned to application-specific chains (app-chains) to meet higher performance requirements or vertically integrate their ecosystems, allowing them to capture a larger share of user and order flow. By leaving — or not opting for — Ethereum’s L1, these dApps forgo fee value accrual to the Ethereum ecosystem.

Notable examples include dYdX and Hyperliquid, but the most significant upcoming move is Uniswap’s shift to Unichain. As one of Ethereum’s largest gas consumers, Uniswap has historically made a substantial contribution to its fee pool. To put it in perspective, across November / December, Uniswap consumed approximately nine times more gas than blob transactions.

Figure 20: Uniswap consumed approximately nine times more gas than blob transactions over a 30-day period in November / December

A fair question to ask is whether more leading applications will choose to leave the Ethereum L1, or perhaps forgo it altogether, in order to capture more value via their own app-chain. Something to keep an eye on.

The Prioritization Dilemma: Ethereum’s broad ambitions pose another challenge, as it simultaneously pursues multiple market spaces. This challenge arises from the prioritization dilemma: should Ethereum focus on L2s to enhance blobspace and compete with alt-DA layers, or prioritize L1 improvements to strengthen the execution layer and contend with alt-L1s? This strategic ambiguity has a direct bearing on ETH’s value accrual.

This divergence of focus between multiple key areas introduces uncertainty, which can weigh on market confidence. While pursuing many areas concurrently is theoretically possible, following multiple paths risks diluting focus and slowing progress, particularly when competing protocols excel in specialized niches.

Without clear directional alignment, there are risks of overextending efforts and spreading value too thin, reducing the likelihood of achieving any single vision effectively.

Figure 21: Does Ethereum have a single, unified vision?

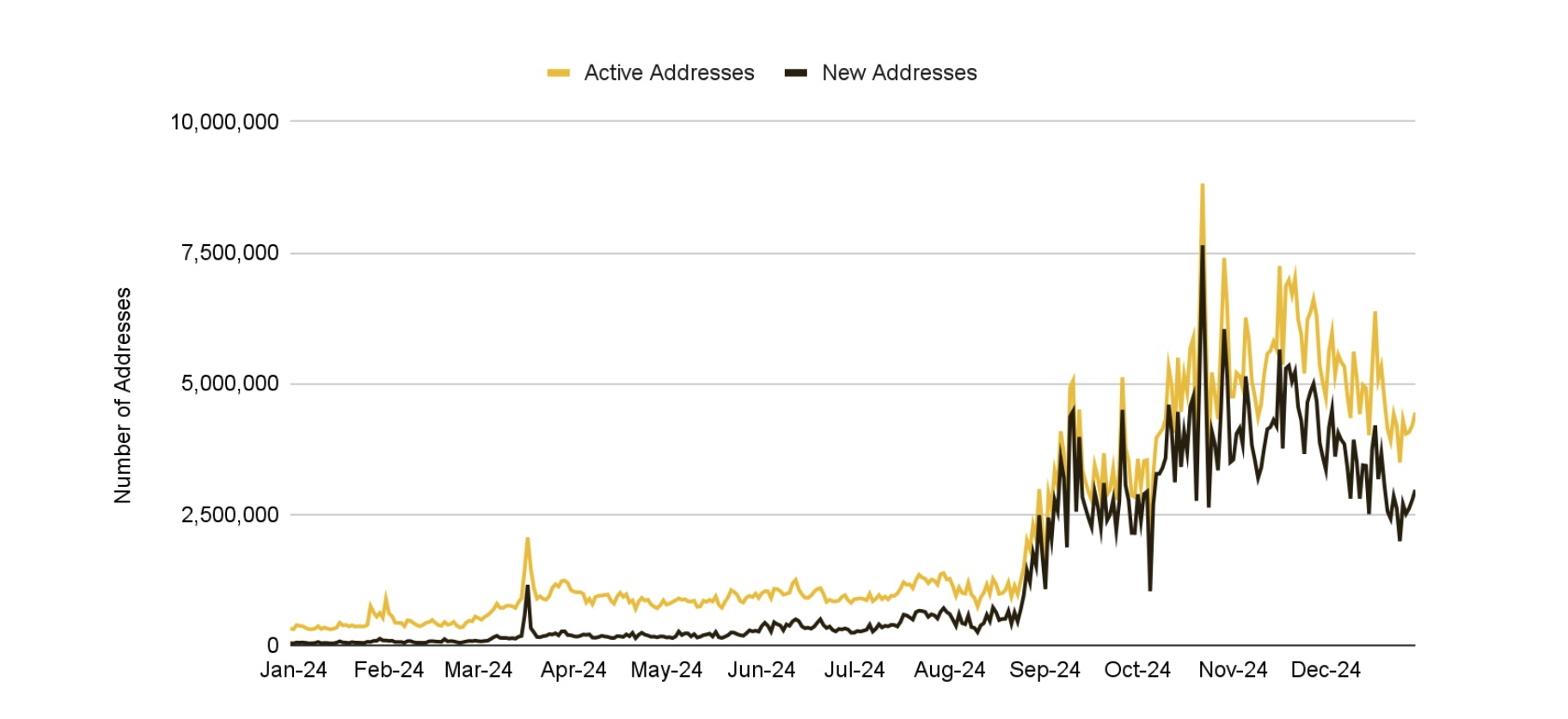

Solana

Solana had a very strong year, performing extremely well from both a fundamental and narrative point-of-view. On the fundamental side, network growth reached new all-time highs and surpassed Ethereum in many key categories, from DEX volumes to fees. From a narrative perspective, Solana remained at the forefront of some of the largest drivers of 2024, the most notable of which was memecoins.

Figure 22: Solana’s new and active addresses demonstrated significant growth in 2024

DEX Volumes and Revenues

Driven by memecoins, and a growing DeFi ecosystem, among other factors, Solana has performed with strength in terms of volume and fees.

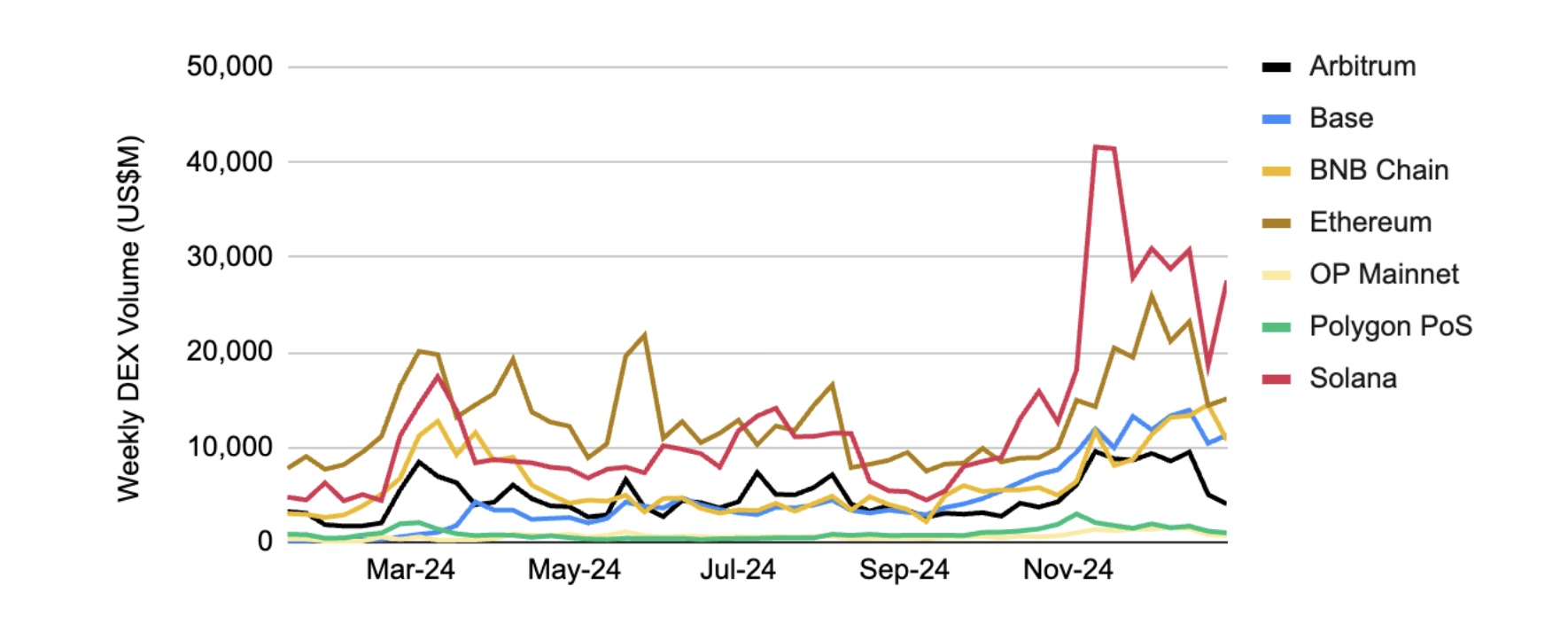

DEX Volume: Solana’s DEX volumes broke their all-time high levels multiple times in 2024 and are now higher than those of Ethereum. In fact, Solana’s November 2024 DEX volumes were comparable to those of Ethereum and all L2s combined.

Figure 23: Solana’s DEX volumes have surpassed Ethereum and are significantly ahead of other major chains

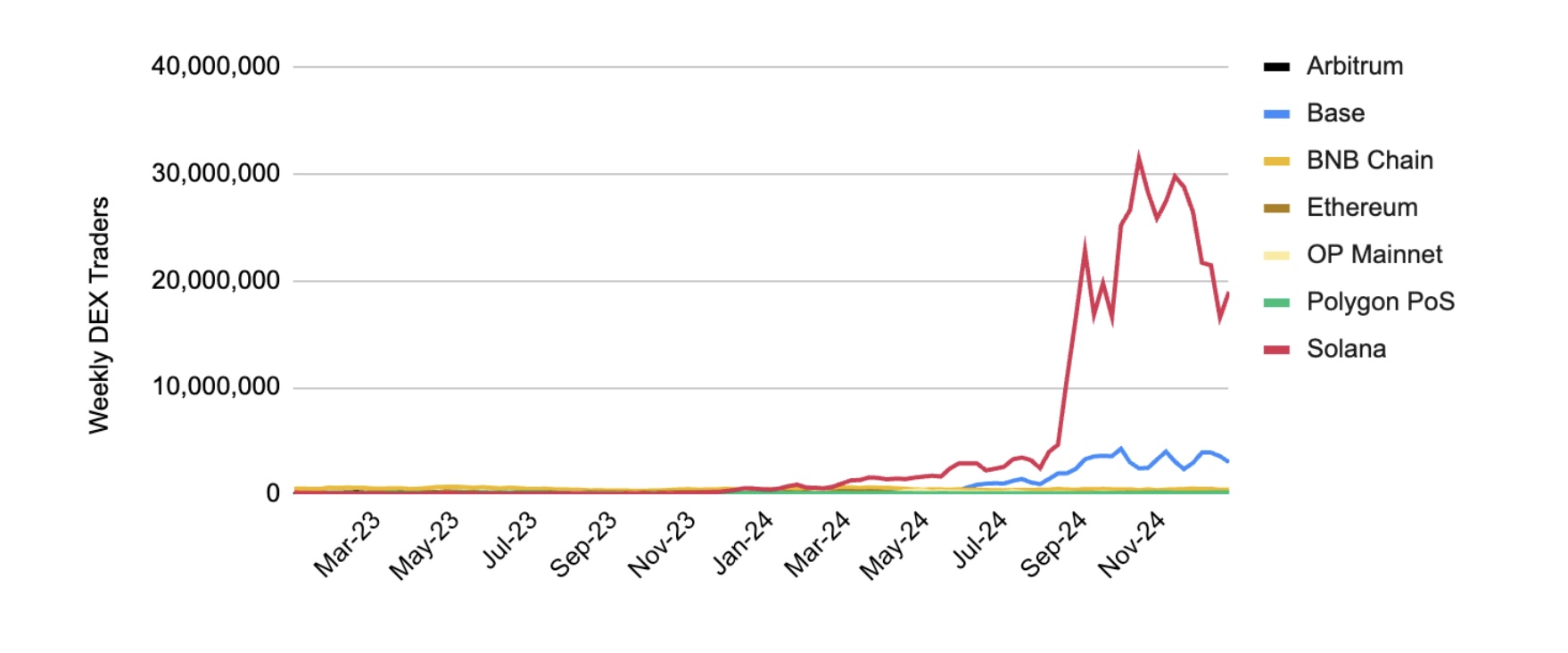

As we can see in Figure 24, the weekly DEX traders figures for Solana have seen significant growth relative to the rest of the market. While not completely attributable to memecoin trading, this has undoubtedly been a key growth driver.

Figure 24: Weekly DEX traders have surged for Solana

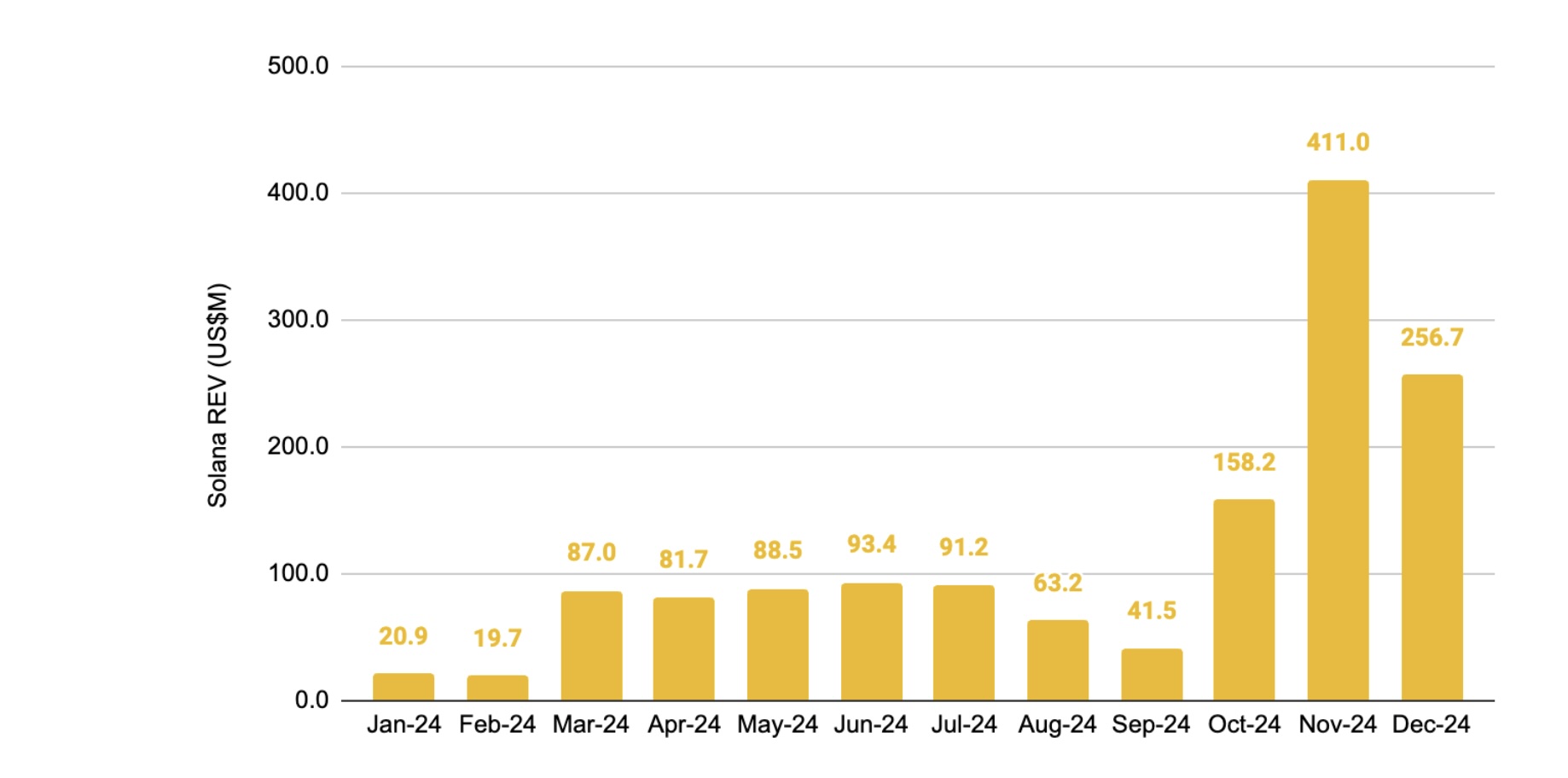

Profitability: Solana’s real economic value (REV), which represents the network’s total income from its various fee sources, consistently saw new highs through 2024. November was a particularly large month, seeing over US$410M in REV to set Solana’s new all-time high.

Figure 25: Solana’s monthly real economic value (transaction fees + MEV tips) grew significantly 2024

Memecoins

Memecoins have been one of the leading narratives of this cycle and saw an explosion across 2024. As we will see later in this report, memecoins were the top performing sub-sector in 2024, with a year-to-date return of over 200%.

Solana has been central to the growth of the memecoin markets, with many traders choosing it as their blockchain of choice when trading memes. There are multiple factors at play here, with the relatively cheap transaction fees and the cohesive and unfragmented product suite, being key highlights. Solana’s leading non-custodial wallet, Phantom, has also been important, with its simple user experience being a key factor. Having expanded from Solana to also supporting Ethereum, Polygon, Base, and Bitcoin, Phantom has further announced upcoming support for Sui and Monad this year.

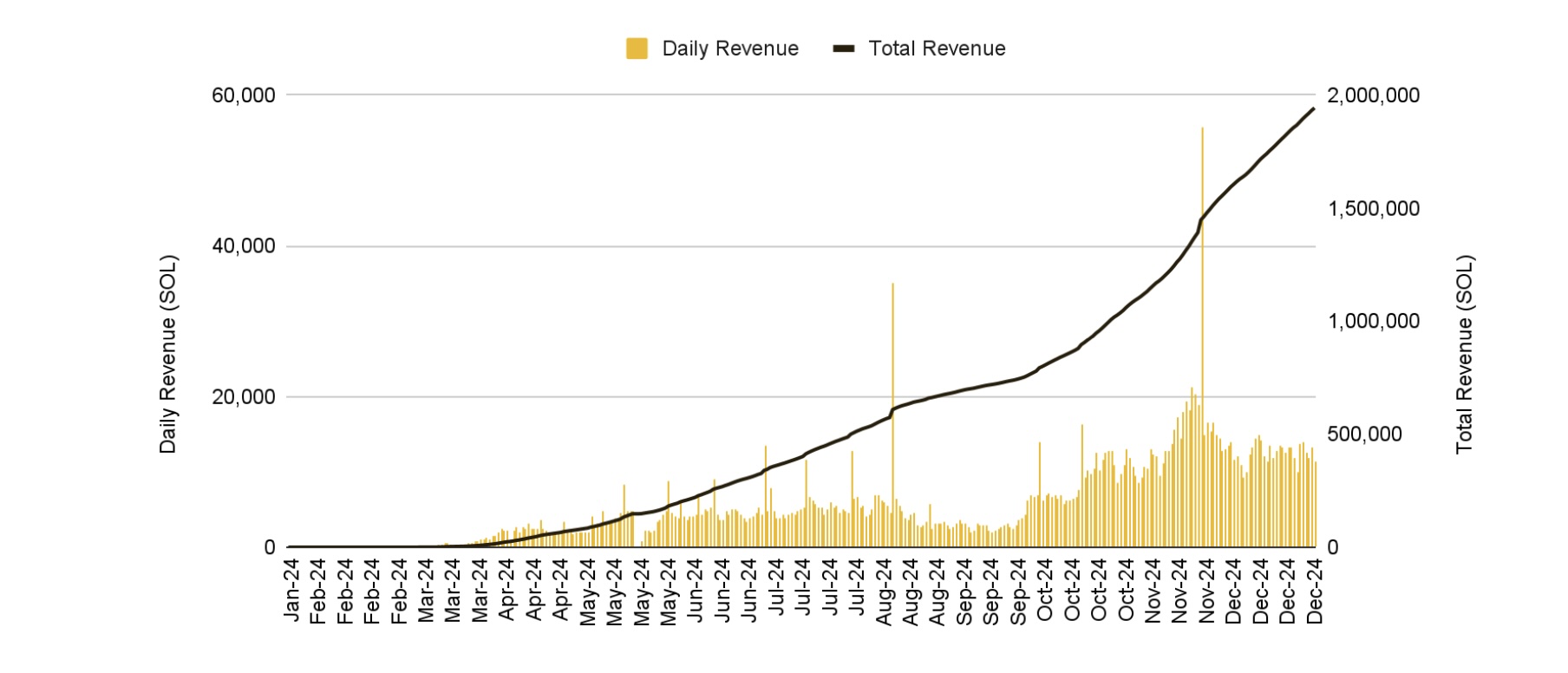

Pump.fun: Solana’s native memecoin launchpad, Pump.fun, has been integral to the story, providing users a cheap and near-instant way to launch memecoins. Traders also benef it from each token being a fair launch without any pre-sale nor team allocation. Pump.fun’s success has meant that Solana has emerged as the leading chain for new token launches. In fact, over 5.7M new memecoins have been deployed via pump.fun, while the platform has generated over 2M SOL in revenue (~US$410M). This has made pump.fun among the most profitable apps across the entire crypto market.

Figure 26: Pump.fun has generated over US$410M in revenue since their launch

Meme sustainability?: Critics argue that Solana’s performance is not necessarily sustainable due to the prevalence of memecoin trading and the uncertainty around whether memes can last.

However, this might not be all too relevant. Ultimately, as we saw above in the DEX metrics, Solana has shown that it is a premier avenue for trading and users have chosen it as such. While it may be dominated by memecoins as things stand, other assets can take their place as the narrative evolves.

Memecoins, while currently prominent, represent just one category of tradable assets. Solana’s infrastructure and scalability suggest it is well-positioned to excel with other asset classes as market dynamics shift. In fact, the frenzy around memes has further meant that their trading has served as somewhat of a stress test for the network. Commendably, Solana has maintained near 100% uptime for nearly two years, with only one incident in 2024. This is very different to 2022, when such incidents were significantly more common.

Areas of Interest

DePIN: Decentralized Physical Infrastructure Networks (DePIN) remains one of the most interesting innovations in the crypto world and something to keep a close eye on. DePIN projects are typically infrastructure projects that use blockchain technology and crypto-economics to incentivize individuals to allocate capital or rent out their resources to create a transparent, decentralized, and verifiable infrastructure network .

Solana hosts various DePIN projects, including Hivemapper, a community-powered decentralized mapping service, and Helium, a crypto-powered 5G cellular network. Pipe, Dawn, and Teleport are others to keep an eye on.

Solana is also leading the AI agent narrative, as well as, hosting AI infrastructure projects such as Grass. Progress on this particular sub-sector will be important to track this year.

Network Extensions: Solana’s take on L2s are called “network extensions” i.e., networks that extend Solana’s capabilities for a focused set of operations.

While it may sound quite similar to traditional L2s, they are different insofar as app-specific networks, rather than general extensions of blockspace. This means that they do not necessarily contribute to liquidity fragmentation, which Ethereum L2s have been criticized for. Additionally, their existence is not due to Solana’s scaling limitations (like it is for Ethereum), but rather to add custom functionality that differs from the L1.

An early example is the perps DEX, Zeta Markets, which is building the Bullet rollup to better support low-latency trading. This is expected to have a mainnet launch in Q1. Solana also has Magicblock, which allows developers to create Solana Virtual Machine (SVM) ephemeral rollups with a focus on use cases like gaming.

SVM Stack: Solana Virtual Machine (SVM), a competitor to the widely used Ethereum Virtual Machine (EVM) is also growing in relevance and popularity. There are a number of chains building on the SVM, which might potentially increase the SVM’s network effects. This is important as one of the key drivers of Ethereum’s growth and relevance has been the widespread popularity of the EVM.

Examples include Eclipse , which recently launched its mainnet offering. Eclipse uses a combination of the SVM, Ethereum, and Celestia.

Others like Soon, Atlas and Sonic are also building on the SVM stack and are expected to see progress this year.

What’s Coming Up?

Firedancer: Solana’s hotly anticipated, new, independent validator client is set to be released this year. Solana currently has two clients, both of which are forks of the original Solana Labs client. Agave, maintained by the Anza team, and another by Jito Labs. However, as both are forked from the original Solana Labs client, if a bug takes down one of these clients, it is likely that it is present in both. Firedancer, on the other hand, is completely independent, and even written in a different language (C++ vs Rust for the original client).

The key benefit of Firedancer is increased network reliability and resiliency, i.e. if a bug takes down the other clients, the network can remain running on Firedancer. Additionally, Firedancer aims to significantly bolster Solana’s scalability, with Firedancer having processed 1M+ TPS in tests — significantly higher than Solana’s current average of ~3-5K. Firedancer will also help reduce latency times, which should help give Solana dApps a performance boost.

At Solana’s Breakpoint conference in September 2024, an interim non-voting version of the full Firedancer client called Frankendancer went live on mainnet, while the Firedancer client went live on testnet. The full version is expected sometime later this year.

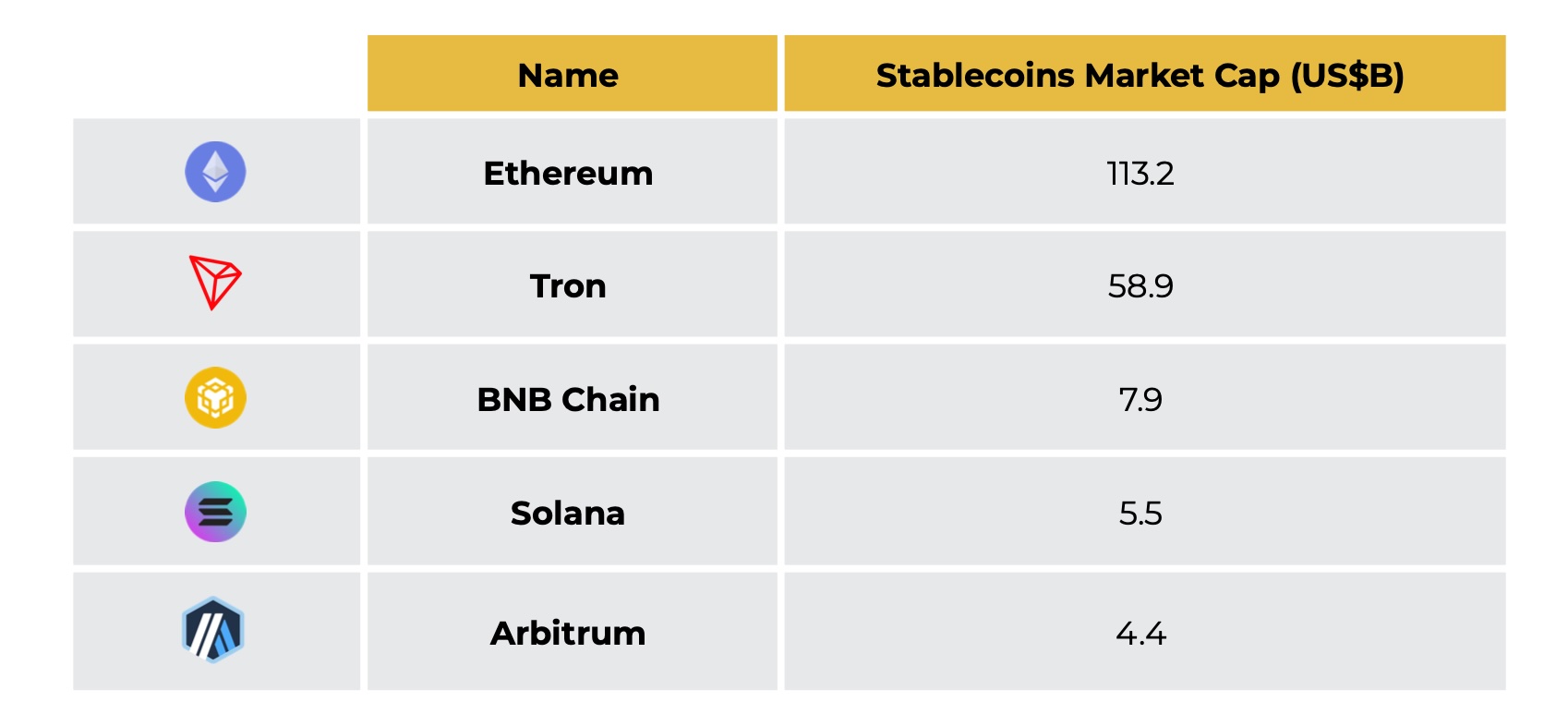

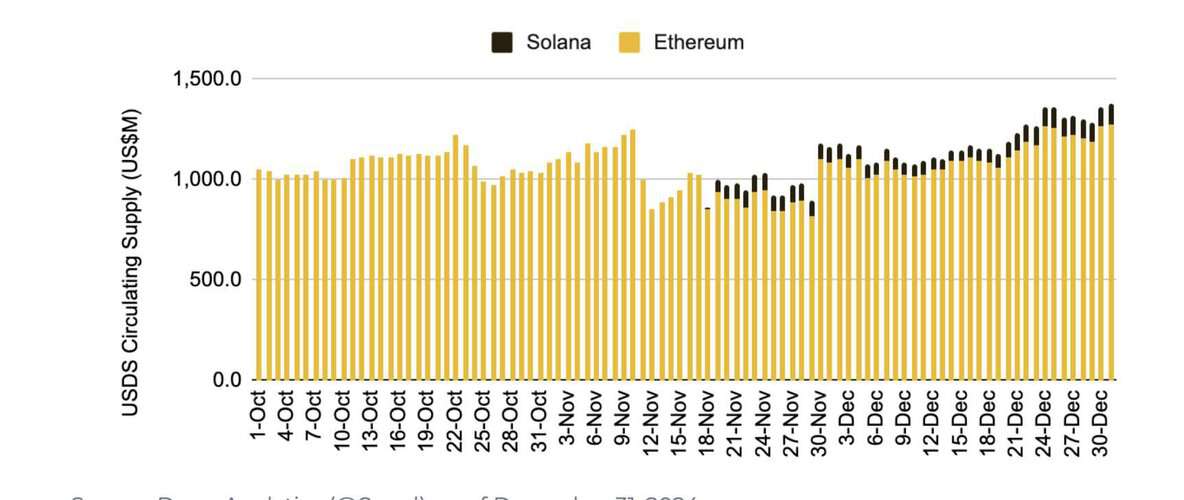

Limited stablecoins?: Although stablecoin volume and availability on Solana has been growing, it still lacks the likes of Ethereum and is an area that should be paid attention to. Stablecoins are the lifeblood of L1s, especially DeFi, and it is easy to argue that the significant stablecoin concentration on Ethereum is at least a partial contributor to its continued dominance in DeFi.

Figure 27: Solana stablecoin market cap is significantly lower than that of Ethereum

2024 saw the launch of Paypal’s PYUSD on Solana, which initially saw strong growth, driven by incentives and partnership. However, after peaking at over US$1B circulating, supply (i.e., market cap, as supply = market cap for stablecoins if they maintain their US$1 peg) has slowly dwindled down towards US$500M. It remains to be seen if PYUSD will regain growth in the coming year.

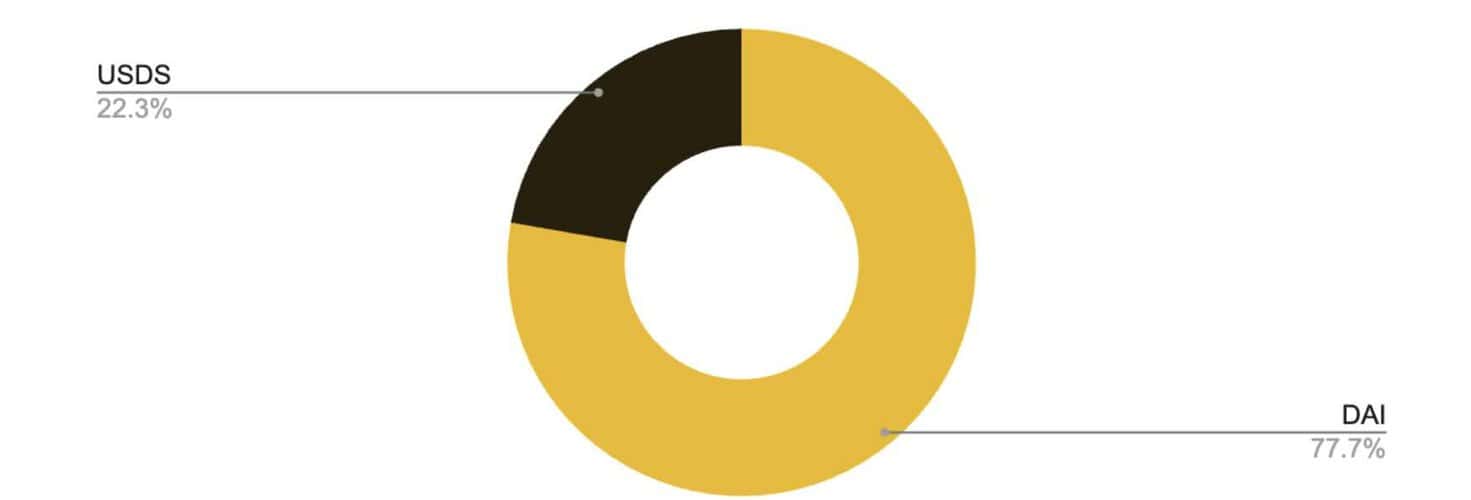

More recently, we also saw the launch of USDS (Sky Dollar, the new stablecoin from the MakerDAO team) on Solana. Although supply is still limited at around US$110M, it is a step in the right direction.

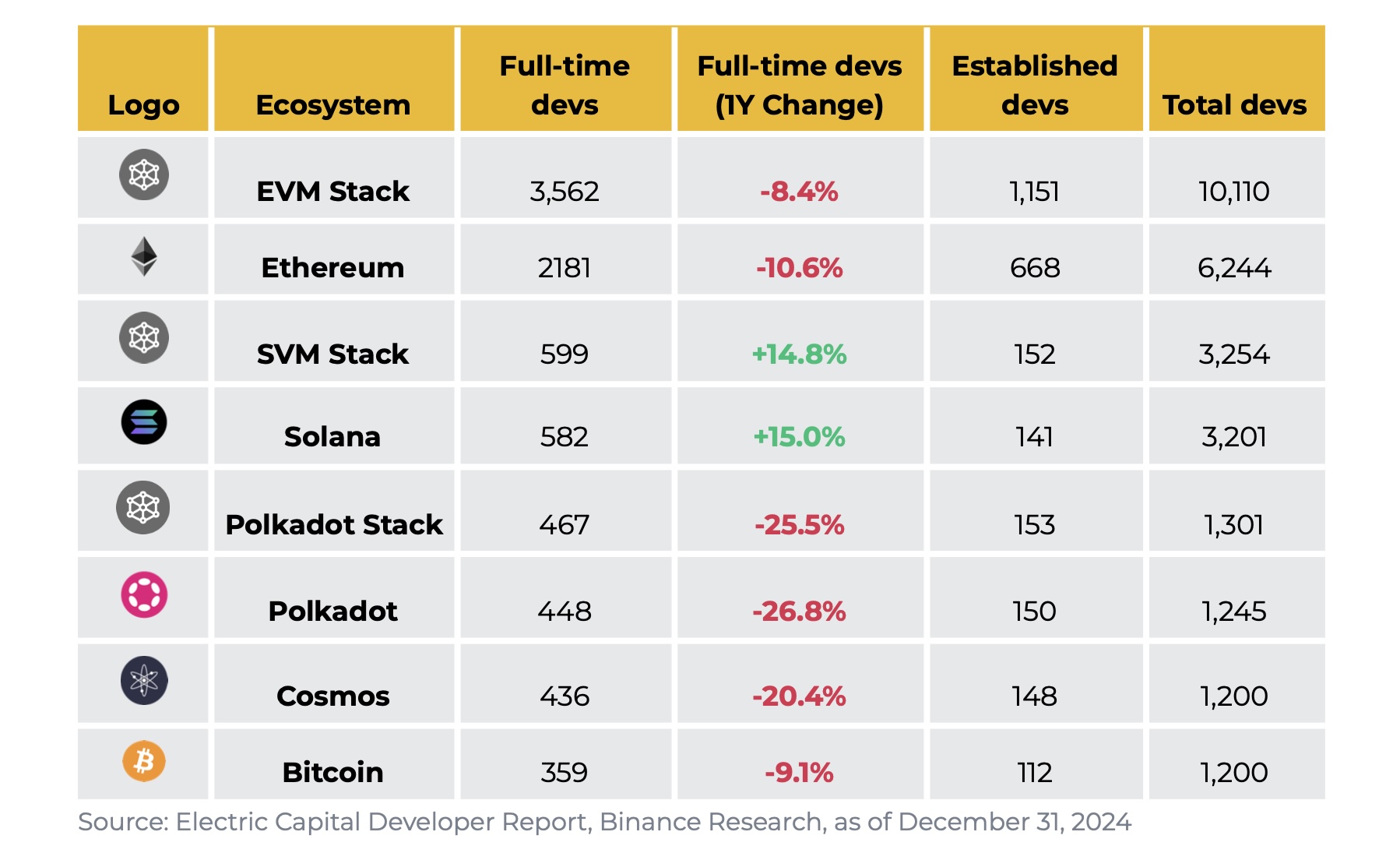

Growing Developer Interest: A critical factor to note in the growth trajectory of any crypto project is the level of developer interest it gets. In this metric, Solana excels.

Solana’s full-time developers rank second only to Ethereum. While Ethereum saw a drop off in developer interest in 2024, Solana saw a double-digit increase.

An important fact to note is that Ethereum has a ~6 year headstart on Solana given that it launched in 2014, versus 2020 for Solana. As we have seen above, Solana’s volumes are already exceeding those of Ethereum, while other metrics like fees are also starting to compete. Given developer interest is typically a leading metric for growth, as things stand, the future for Solana looks bright.

Figure 28: Solana saw a largest jump in developer interest in 2024 among the major chains and ranks second only to Ethereum

BNB Chain

BNB Chain ended 2024 in a position of strength as a leading L1 progressing in a number of different directions. Notable achievements include the network consolidation under the ‘One BNB’ multichain strategy, scalability progress led by opBNB and data storage growth under BNB Greenfield. BNB Chain was also positioned as an AI-first chain with the implementation of noteworthy initiatives like the Gas-Free Carnival and stablecoin incentives.

Ecosystem Growth

BNB Chain saw a significant 58.2% increase in total value locked, from US$3.5B in January to US$5.5B by the end of 2024. Also, it saw a 17.7% rise in unique addresses, growing to over 486M.

The average transaction fee on BNB Chain during 2024 remained at US$0.03 per transaction. BSC’s fees continued to be competitive compared to blockchains like Ethereum, Arbitrum, and Avalanche. Transaction activity was also robust, with an average of ~4M daily transactions during 2024, highlighting capacity for high throughput.

2024 also saw BNB Chain embark on a number of initiatives to drive both developer and user growth. Specifically:

To promote affordable stablecoin transfers, BNB Chain launched the Gas-Free Carnival in September 2024. This initiative eliminated gas fees for transferring or withdrawing stablecoins like USDT, FDUSD, and USDC on BNB Chain and opBNB. BNB Chain also launched the TVL Incentive Program to encourage DeFi projects to grow their TVL, accelerating stablecoin adoption.

BNB Chain also committed US$1M through the Meme Innovation Battle to accelerate memecoin innovation within the ecosystem.

BNB Chain also held numerous hackathons, distributing over US$2 million in prizes to over 20 projects.

BNB Chain also executed Seasons 7 and 8 of its Most Valuable Builder (MVB) Program, and launched the BNB Chain Incubation Alliance (BIA) to improve Web3 project development. The MVB program saw 48 projects selected out of over 1,200 applicants, while 12 winners were awarded across five BIA events. Winners received direct admission to the MVB Program and extended support, including access to BNB Chain’s launch-as-a-service (LaaS) and the Kickstart programs.

opBNB

opBNB is a BNB Chain optimistic rollup L2 solution based on the OP Stack. opBNB is EVM-compatible, capable of up to 4.6K transactions per second (TPS), and has an average gas fee (37) of ~0.001 gwei (which is

In 2024, opBNB achieved an average DAU of 4.7M, with an average of 7.1M transactions being processed per day. Leading dApps include derivatives platform, KiloEx as well as DeFi platforms, PancakeSwap and Goose Finance.

As we look ahead, opBNB is targeting 10,000 TPS and a 10x cost reduction, with notable updates such as support for new wallets, a customized gas token, and bug fixes in the Optimism SDK.

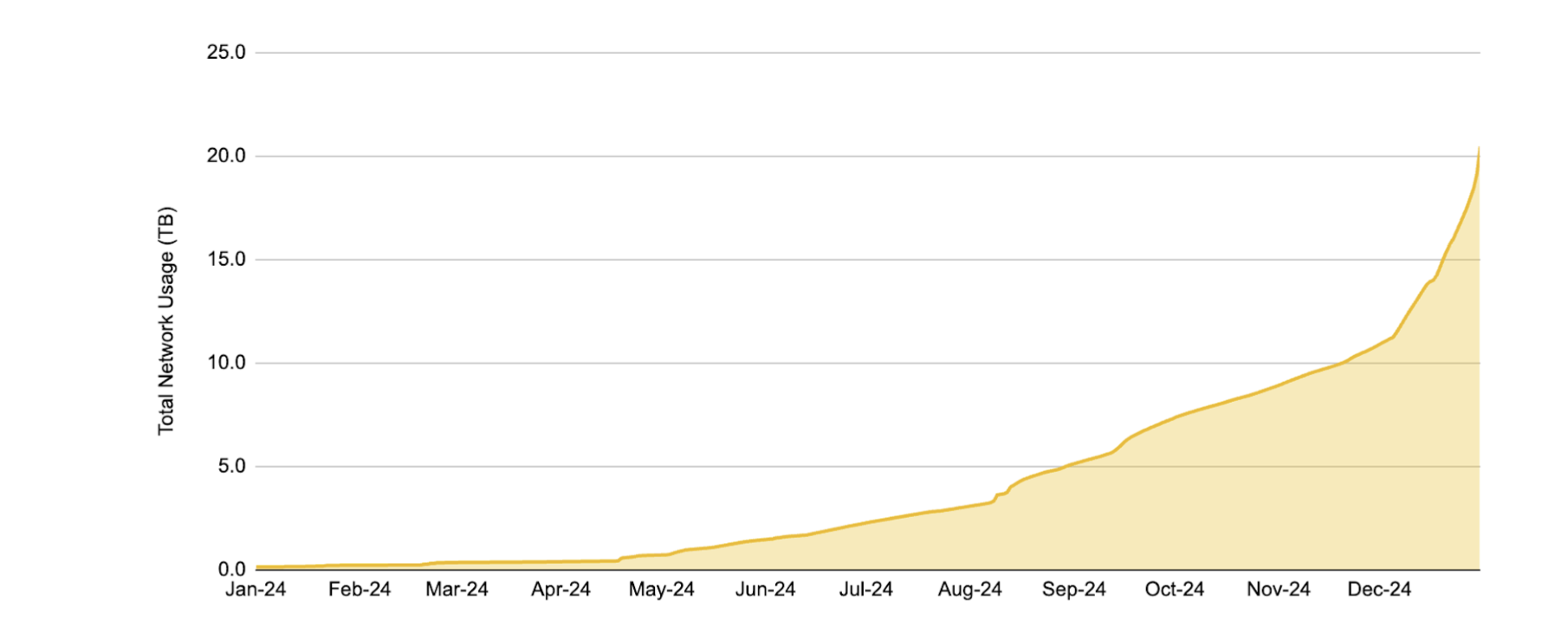

BNB Greenfield

BNB Greenfield provides decentralized data storage infrastructure within the broader BNB Chain ecosystem. It is a storage-oriented blockchain where users can create, store, and exchange data that they fully own. With the use of a native cross-chain bridge, all of the data stored in BNB Greenfield can easily be transferred to BNB Smart Chain, where it can be used by BNB Chain dApps and any new BNB Greenfield dApps. Use cases include website hosting, cloud storage, blockchain data storage, publishing, personal data markets, etc. More details can be found on the official website here .

Since launching their mainnet in Q4 2023, BNB Greenfield has seen ~18.6 TB of storage, 17.6M transactions across ~106K total addresses. Notable players include AI studio, Limewire, infrastructure players CodexField, Aggregata, and Rido, alongside Binance Web3 Wallet.

Figure 30: BNB Greenfield’s network usage has been rising

2024 was the completion of three forks in order to enhance functionality and user experience. The alpha version of Greendrive was also launched, supporting over 30 public datasets and featuring an updated user interface. Greendrive offers a secure, permission-based environment for storing and sharing AI data and models. The BNB Archive Layer was also introduced, built on BNB Greenfield, to provide permanent storage for historical block and blob data, ensuring long-term availability and decentralization.

For further detail on BNB Chain’s progress in 2024, please check out their 2024 Annual Report. As we look ahead, BNB Chain will focus on its positioning as an AI-first chain, driven by its high throughput and low transaction costs, opBNB’s rapid processing for real-time responsiveness, and BNB Greenfield’s secure, decentralized data storage. BNB Chain will also continue to empower startups via its various flagships programs.

Others

Avalanche

Avalanche remains among the few alt-L1s that has managed to maintain a degree of relevance in a market largely dominated by the big players. Their flagship L1, the C-Chain, sits in the top 10 DeFi and stablecoins chains, with a DeFi TVL of ~US$1.3B, and over US$2.2B in stablecoins.

They recently rebranded “Subnets” as “Avalanche Layer-1s”, of which there are 34 live on mainnet. The most notable among these are DeFi Kingdoms (Gaming) and Dexalot (DEX). In March, Avalanche released Teleporter, which is a communication protocol designed to improve interconnectivity between the Avalanche L1s. Teleporter facilitates tokens, NFT, and message transfers across subnets, and continues to see daily activity.

Most recently, Avalanche saw its largest ever update with Avalanche9000. The update reduced the minimum gas fee on the C-chain by up to 96%, lowered the cost of deploying Avalanche L1s by ~99%, and improved L1 interchain messaging. This was accompanied by a US$250M locked-token sale. It will be interesting to see if this leads to more L1s being deployed and greater growth on the C-chain.

Move-based Chains: Aptos, Sui

Born from the ashes of Meta’s Libra project and launched in late 2022, Aptos and Sui have been steadily growing over the last couple of years. Both utilize the Move programming language and class themselves as high-throughput L1s. Aptos has focused on bringing institutional interest to crypto and RWAs, with recent partnerships including Franklin Templeton, and Microsoft. On the other hand, Sui has been more involved in the gaming and consumer space, recently announcing their own handheld gaming device, the SuiPlay0X1.

While still relatively early in their lifecycles as L1s, it appears that the market has been more responsive towards Sui, which has a fully-diluted value (FDV) ~4x higher than that of Aptos. It will be interesting to see how things evolve in the coming year.

TON

TON saw a surge in popularity and narrative mindshare in 2024, particularly around the middle of the year. Key to this growth has been their close links to the Telegram messaging app, which has over 950M monthly active users which is a key part of crypto circles. TON’s viral tap-to-earn minigames, including Notcoin and Hamster Kombat commanded significant mindshare in the summer of 2024 and gained millions of users and token holders (following highly publicised airdrops). While there have been some criticisms of the simplicity of the games, the mass appeal and virality has been undeniable. As we look ahead to 2025, it will be important to see if TON can leverage the vast reach of Telegram in order to onboard new users and build larger crypto communities across its various different markets. How apps evolve from tap-to-earn to more sustainable plays will also be interesting to monitor.

Tron

Tron remains a leading stablecoin settlement chain and host to nearly ~US$60B (41%) of USDT. However, for the first time since June 2022, Ethereum has overtaken Tron as the leading network for USDT, with ~US$67B (46%) of USDT supply. It will be important to monitor how and if Tron responds to this change.

In terms of DeFi TVL, Tron sits as the third-largest chain. However, this is only composed of ~34 protocols, compared to over 1.2K for Ethereum and over 180 for Solana. JustLend is responsible for ~US$6B out of US$7.3B of total Tron DeFi TVL.

Upcoming

Monad

One of the more widely anticipated upcoming chains, Monad is building a “high-performance Ethereum-compatible L1” that can offer up to 10,000 transactions per second (tps) with 1 second block times and 1 second block finality. As a reference, Ethereum block times average around 12 seconds, while finality is typically achieved in 12-18 minutes.

Monad implements four key aspects to achieve this performance:

MonadBFT: A high-performance consensus mechanism derived from the widely used HotStuff.

Deferred Execution: One of Monad’s novel features is that execution is decoupled from consensus. To recap, consensus is the process where nodes agree upon the official ordering of transactions, while execution is when transactions are actually processed and the state of the blockchain is updated.

Deferred execution is a key driver of high levels of transaction throughput for Monad.

Parallel Execution: Transactions are executed in parallel on Monad, rather than sequentially, again contributing to higher throughput.

MonadDb: This is Monad’s custom database for storing the state of the chain. This is purpose-built to support Monad’s parallel execution and is a key feature of the chain.

Monad has conducted “Monad Madness” hackathons in order to help ecosystem growth and now has teams building (46) in various different sectors.

Monad has raised ~US$263M across four funding rounds and recently announced the Monad Foundation . Monad launched their devnet in March, their testnet in November, and is expected to launch mainnet in 2025 .

Berachain

Another very-well funded EVM L1 expected to launch over the next few months, Berachain uses a novel proof-of-liquidity consensus mechanism that focuses on building systemic liquidity within the Berachain ecosystem of dApps and aligning all stakeholders via a three-token model. The idea is that native applications can create reward vaults and encourage validators to direct emissions into them. Users can stake their assets into the reward vaults to receive these emissions, while validators benefit from the staked assets. This is meant to create a flywheel of liquidity and rewards and allow for close partnerships between all parties within the Berachain ecosystem.

Berachain has gone through various stages of testnets across 2024, and is expected to launch mainnet in 2025. This comes after raising ~US$142M in funding.

Layer 2s

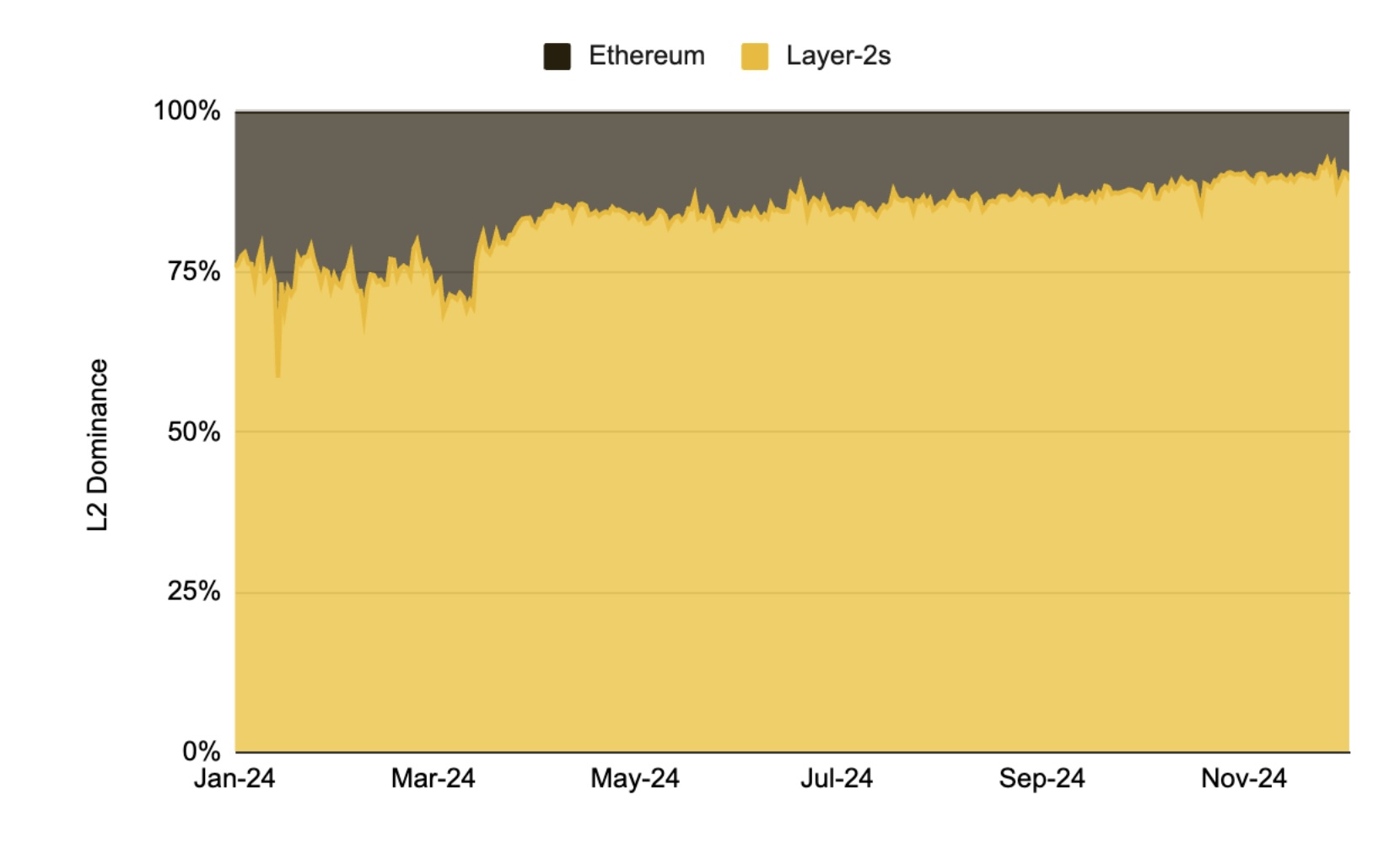

Ethereum Layer 2 (L2) solutions have played a crucial role in retaining users and activity within the Ethereum ecosystem, even as cheaper and faster Layer 1 (L1) blockchains have successfully established their own user bases and market share.

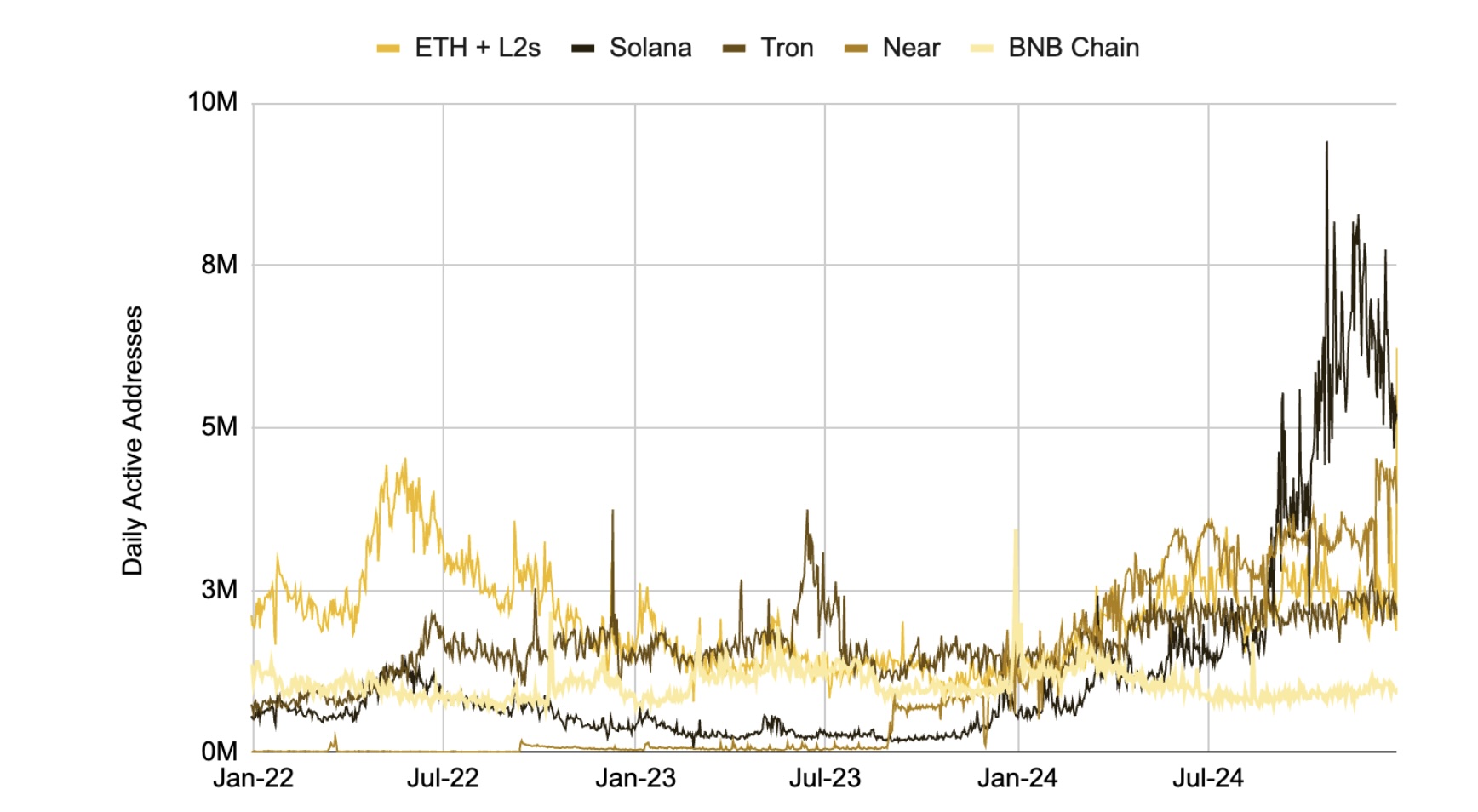

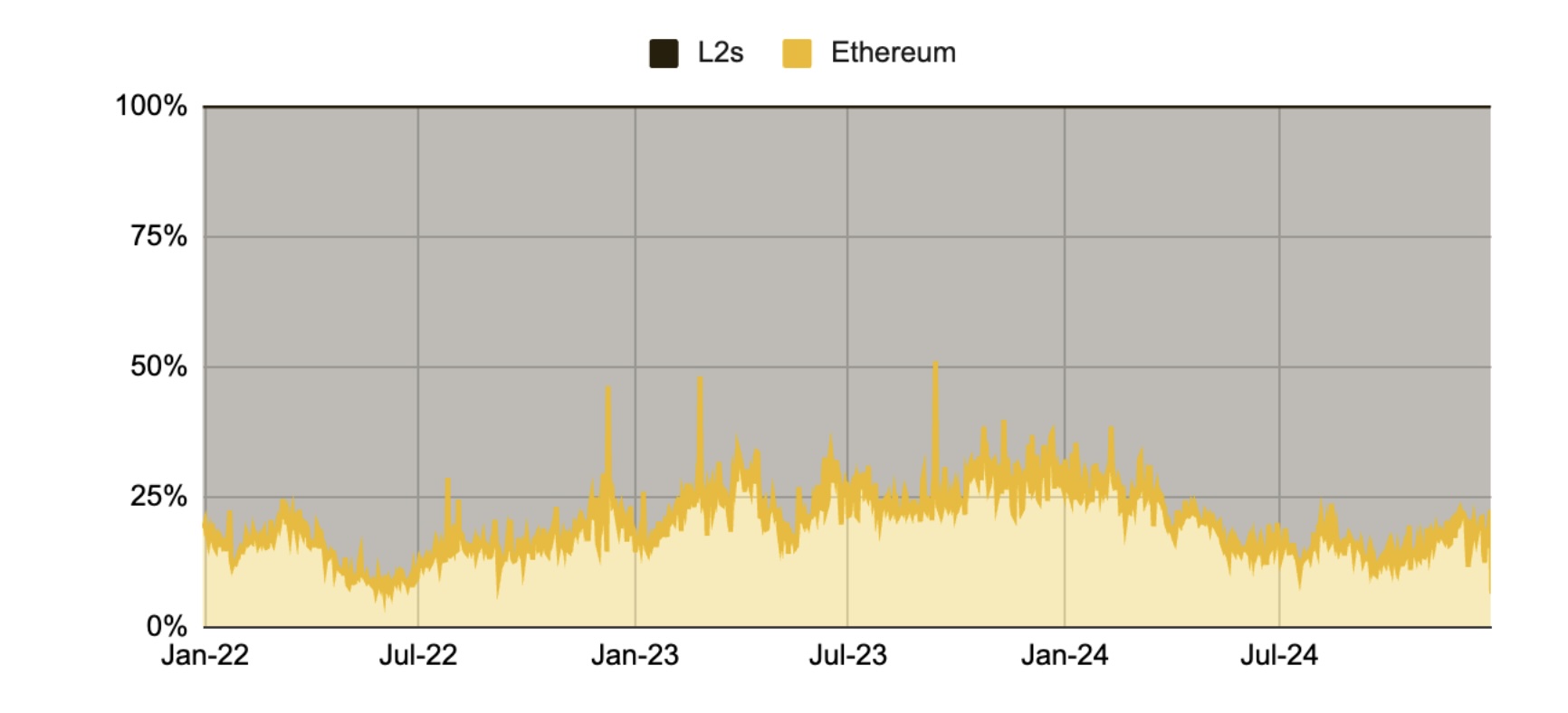

Figure 32: In terms of daily active addresses, L2s have allowed the Ethereum ecosystem (currently at 18% market share) to keep pace with other widely used L1 ecosystems

Much of the Ethereum ecosystem’s continued competitiveness with the new chains in terms of user count can be attributed to the L2s, which have played a pivotal role in attracting and retaining users within the Ethereum ecosystem. Of the total daily active addresses within the Ethereum ecosystem, the vast majority of them were found on the L2s throughout 2024.

Figure 33: L2s have been responsible for the majority of daily active addresses, averaging 80% across the year

Source: Artemis, Binance Research as of December 31, 2024

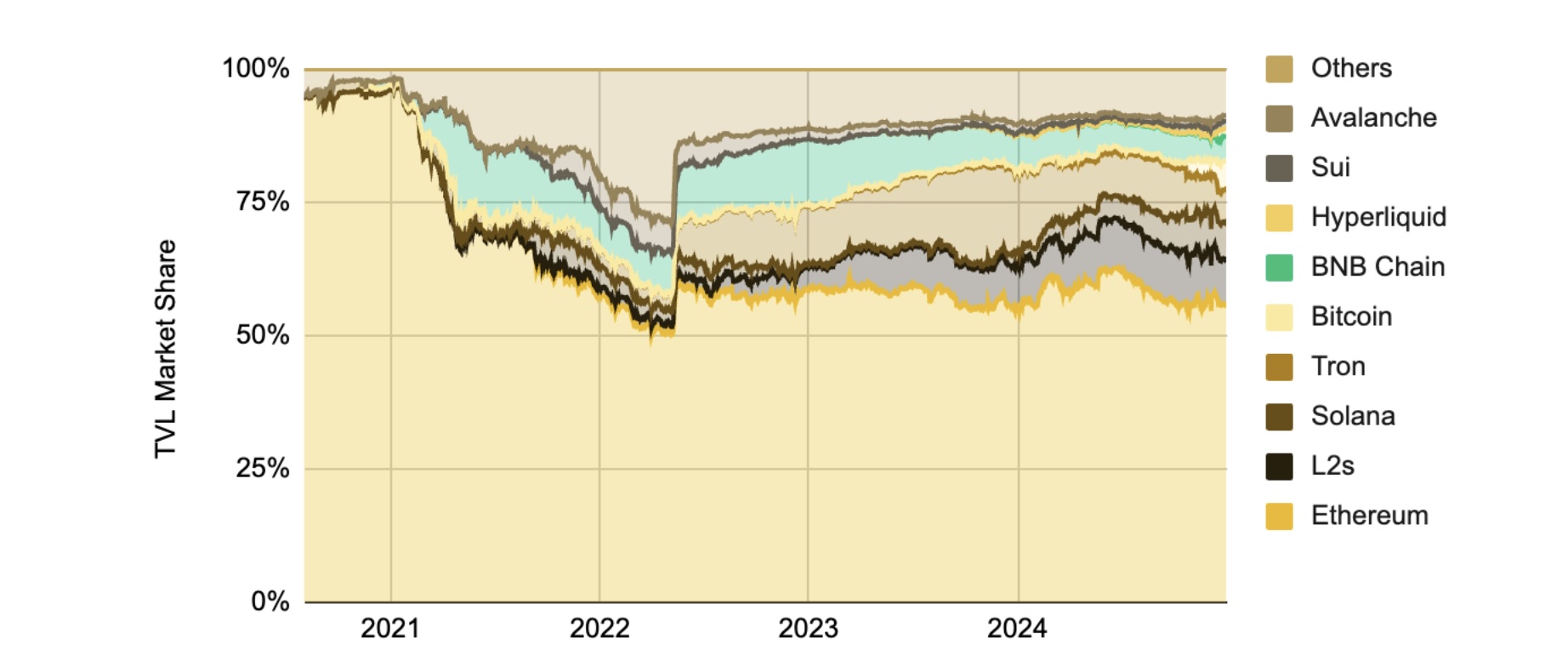

While other L1 ecosystems have reduced Ethereum’s dominance in terms of active users, the Ethereum ecosystem continues to lead significantly in terms of Total Value Locked (TVL), capturing approximately 64% of the total market share across both the Ethereum mainnet and its L2 solutions combined. This substantial dominance in TVL may be a soft indication of the market’s current perception of Ethereum as a more decentralized and secure ecosystem for long term capital storage.

Figure 34: Ethereum and its L2s collectively represent ~64% of the total TVL across all chains, with Ethereum accounting for ~US$66B and L2s contributing ~US$10B

The Year of Airdrops

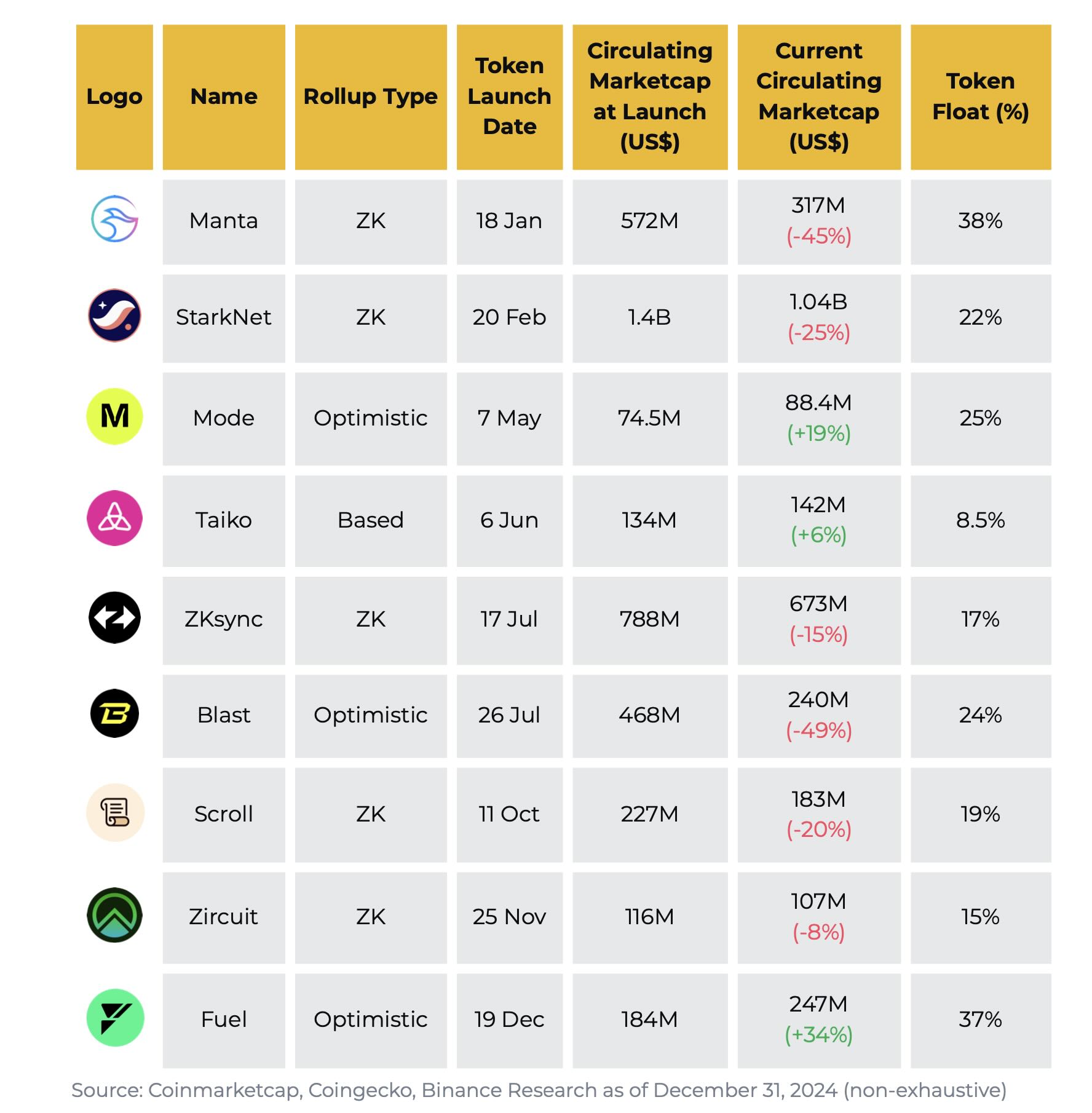

The L2 ecosystem is experiencing rapid expansion, with increasing competition among projects. According to L2beat, there are 50 rollups and 70 validiums and optimiums (49) currently in various stages of development as of December 2024. In addition to many new L2s, 2024 saw many existing L2 projects launch their tokens.

Figure 35: Many of the major L2 tokens airdropped in 2024 are sporting lower circulating market caps than at launch, with an average token float of ~23%

The market capitalizations of many L2 tokens launched this year have declined since their respective launch. This trend may be partly attributed to negative market sentiment regarding the relatively low token floats of many of these tokens.

An Optimistic Outlook

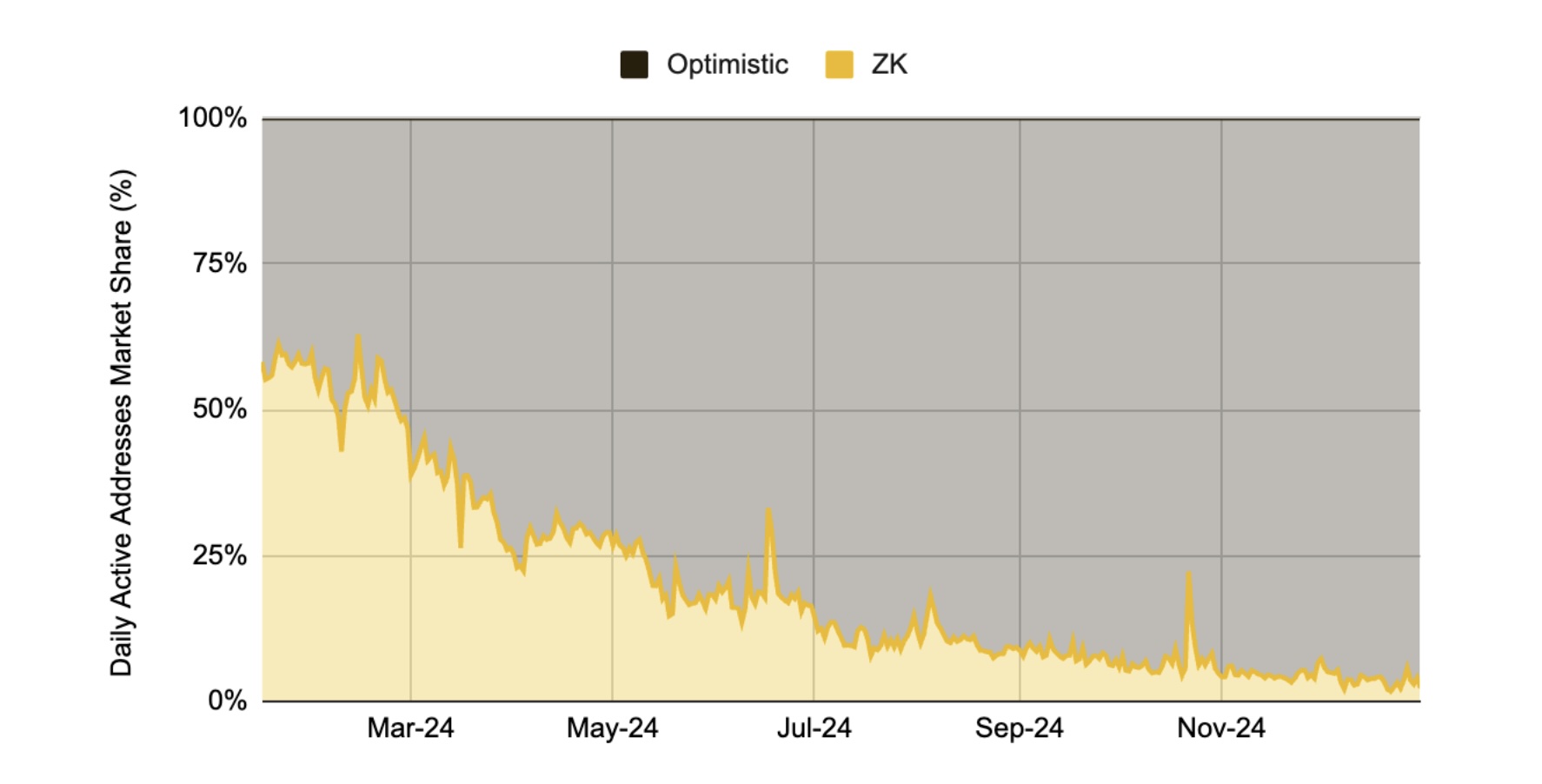

By and large, optimistic rollups continue to be the most widely utilized rollup type. ZK rollups started the year relatively strong in terms of daily active addresses, driven largely by the zkSync Era and Linea airdrop campaigns, which took place earlier in the year. As hype around the ZK L2 airdrop campaigns cooled, so did user activity on those chains, relative to their optimistic counterparts. We saw the optimistic market share in terms of daily active addresses gradually rise to over 96% where it sits today, driven in large part by the rapid growth of the Base L2.

Figure 36: Optimistic rollups have captured over 98% of the daily active address market share across the major rollups in 2024

While ZK rollups have yet to meaningfully supplant retail users from their optimistic competitors, the December announcement from Deutsche Bank revealing its decision to build a L2 using the ZKsync technology stack has the potential to set a trend for other institutional players looking to adopt zk rollups.

As the L2 space continues to heat up, adoption from established companies from both the crypto and TradFi sectors decide to build on Ethereum L2s will be essential to assessing the future health and competitiveness of the Ethereum ecosystem, as well as provide further clarity on the issues surrounding the ongoing ETH Value Debate .

The Optimistic Rollups

Base

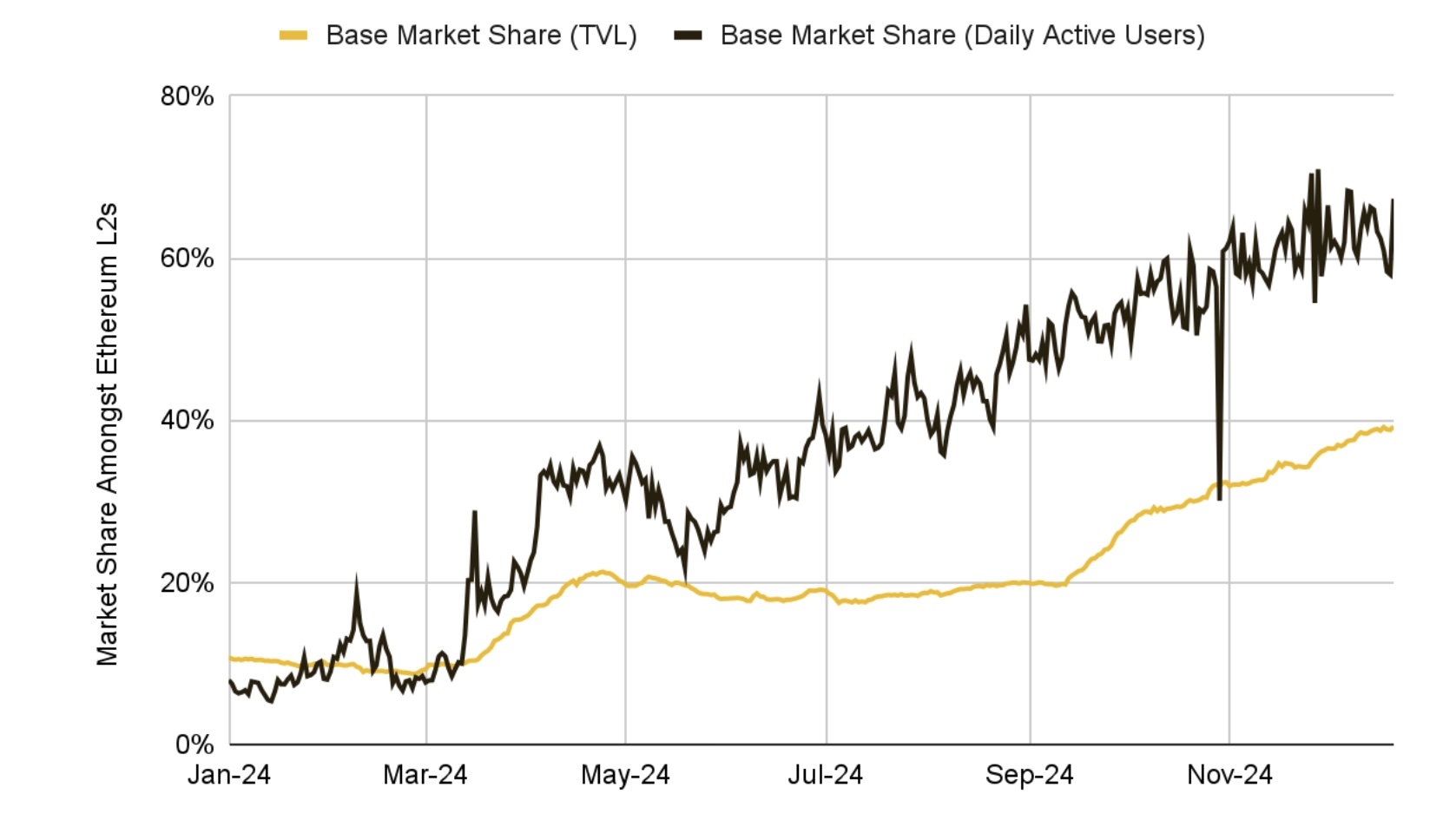

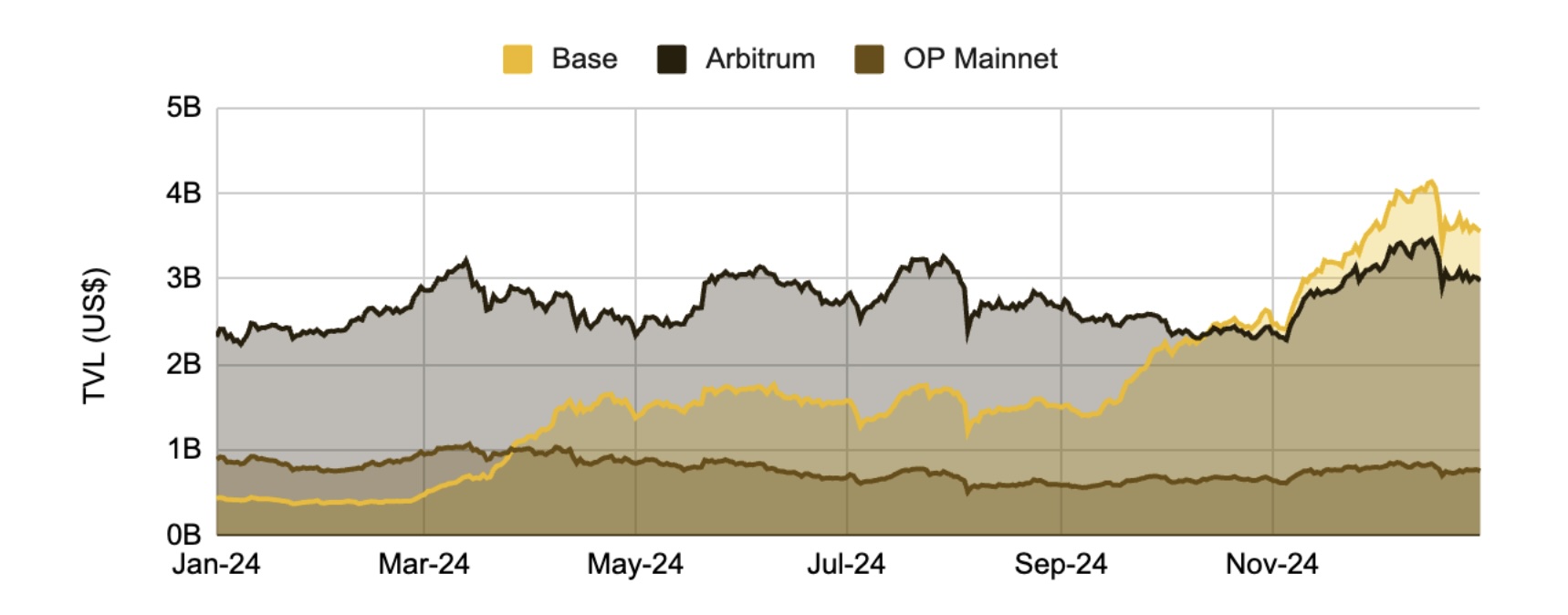

Over the course of 2024, Coinbase’s Base L2 has steadily risen to become the largest L2 on most metrics. It overtook Arbitrum, the previous largest L2, in terms of daily active addresses in July, and in terms of TVL in October 2024.

Figure 37: Base has steadily risen to capture 39% and 67% of the market in terms of TVL and daily active users respectively, making it the top L2 in both metrics

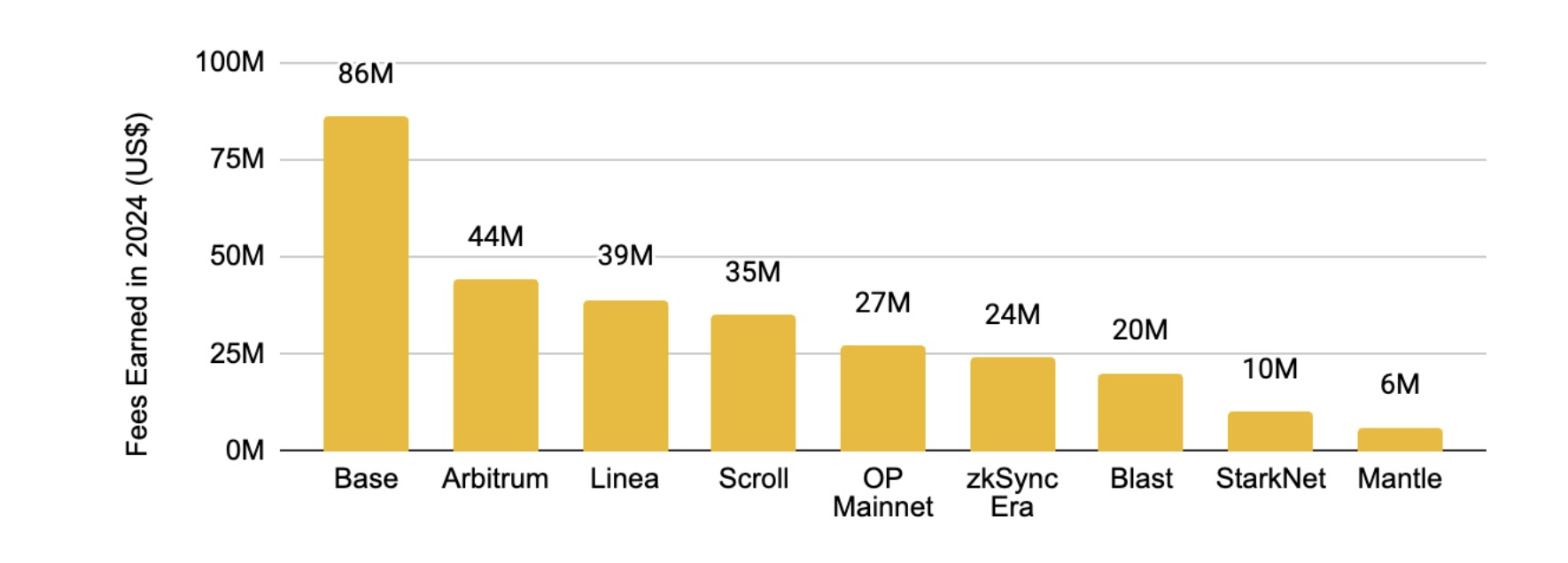

The success and rapid adoption of the Base L2 endeavour has proven to be highly profitable for Coinbase. Year to date (YTD), Base L2 has generated US$86M in fees for the company, putting it at almost double the amount earned by Arbitrum, which comes in second place.

Figure 38: In 2024 Base generated the most fees out of all L2s, at almost twice the amount earned by Arbitrum YTD

The profitability and success of the Base L2 is likely one of the driving factors behind the announcements and launches of the numerous new L2s in 2024 from well-established companies like Kraken, Uniswap and recently even Deutsche Bank.

Arbitrum

For most of its existence, Arbitrum has experienced limited competition for its spot as the number one L2. This year however, we’ve seen a significant shift in market dynamics, as new L2 players have risen up to challenge Arbitrum’s previously unfettered dominance. In 2024, Base supplanted Arbitrum as the L2 with the highest TVL and daily active addresses.

Figure 39: Arbitrum falls to second place amongst the L2s in terms of TVL for the first time since 2022

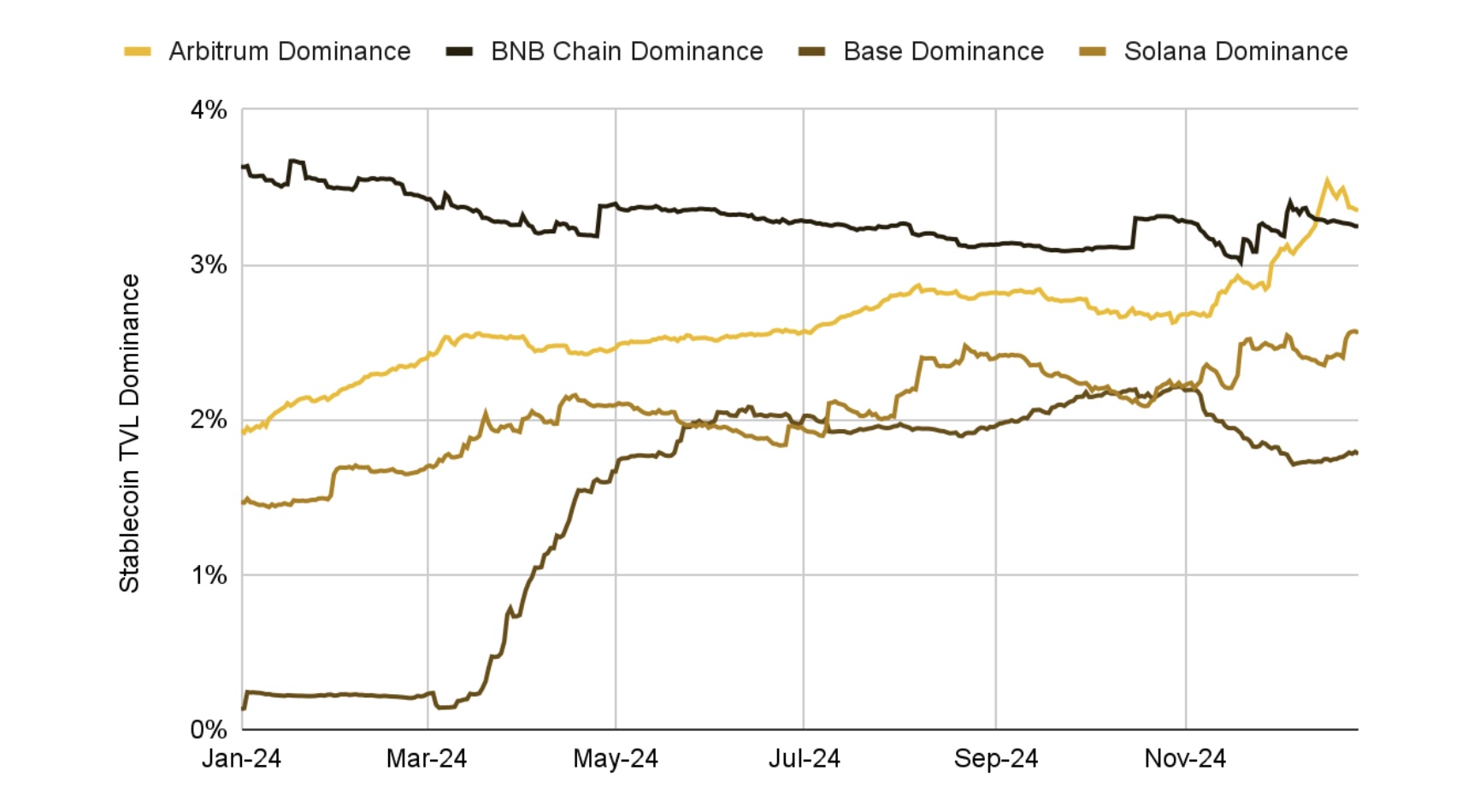

Although Arbitrum has been losing ground to newer L2s in terms of TVL, it has significantly outpaced even some of the largest L1 chains in terms of growth of stablecoins. Over the past 3 years, growth of stablecoin supply on Arbitrum has grown steadily, surpassing Solana’s in March 2023 and remaining higher for much of 2024. Starting in October 2024, the stablecoin supply on Arbitrum saw a large uptick, pushing it ahead of BNB Chain for the first time and surging from US$4.3B to US$6.7B over the past 3 months.

Figure 40: Arbitrum became the chain with the 3rd largest stablecoin supply, behind only Ethereum and Tron, with a market share of 3.4% (~US$2B worth of USDC is locked in the Hyperliquid Bridge)

The surge that began in October was likely largely driven by the launch of various RWA tokenization projects on the chain, such as Franklin Templeton’s and Blackrock’s tokenized money market funds. Another key driver to stablecoin growth on Arbitrum was Hyperliquid, which currently accounted for ~US$2B worth of USDC locked in their bridge.

In addition to stablecoins and RWAs, the Arbitrum Orbit ecosystem has also seen major growth in 2024 for the gaming and consumer use cases, with the launch of chains like XAI, Proof of Play, and Apechain which utilize the Orbit technology stack.

Building on the momentum of 2024, there are a number of interesting L2s and Layer 3s (L3) coming to the Arbitrum Orbit ecosystem in 2025, which continue to expand the range of purpose-built chains built using Arbitrum Orbit.

Corn – a BTCfi chain built using the Arbitrum Nitro stack, that will use BTCN, a 1:1-backed, bridged version of Bitcoin, as its gas token. On August 22, 2024, Corn launched an airdrop campaign allowing users to earn points (Kernels).

Rivalz – a decentralized peer-to-peer network for modular AI applications, it offers a secure source of verifiable personal, credential, and behavioral data, with built-in privacy and intellectual property rights. It is the first Player-to-AI network built on Dymension and powered by Celestia Labs.

Animechain – from the team behind the Azuki NFT project, Animechain aims to enhance creators’ creativity with AI-based production tools. Using AI Rights Assets (AIRA) and a unique token system, it supports the sustainable growth of the anime and content industry. They released a litepaper in May 2024.

Plume – with its mainnet launch slated for early 2025, Plume aims to simplify the process of bringing off-chain assets, such as real estate, art, and financial instruments, onto blockchains by handling paperwork, custodial requirements, and more.

OP Mainnet

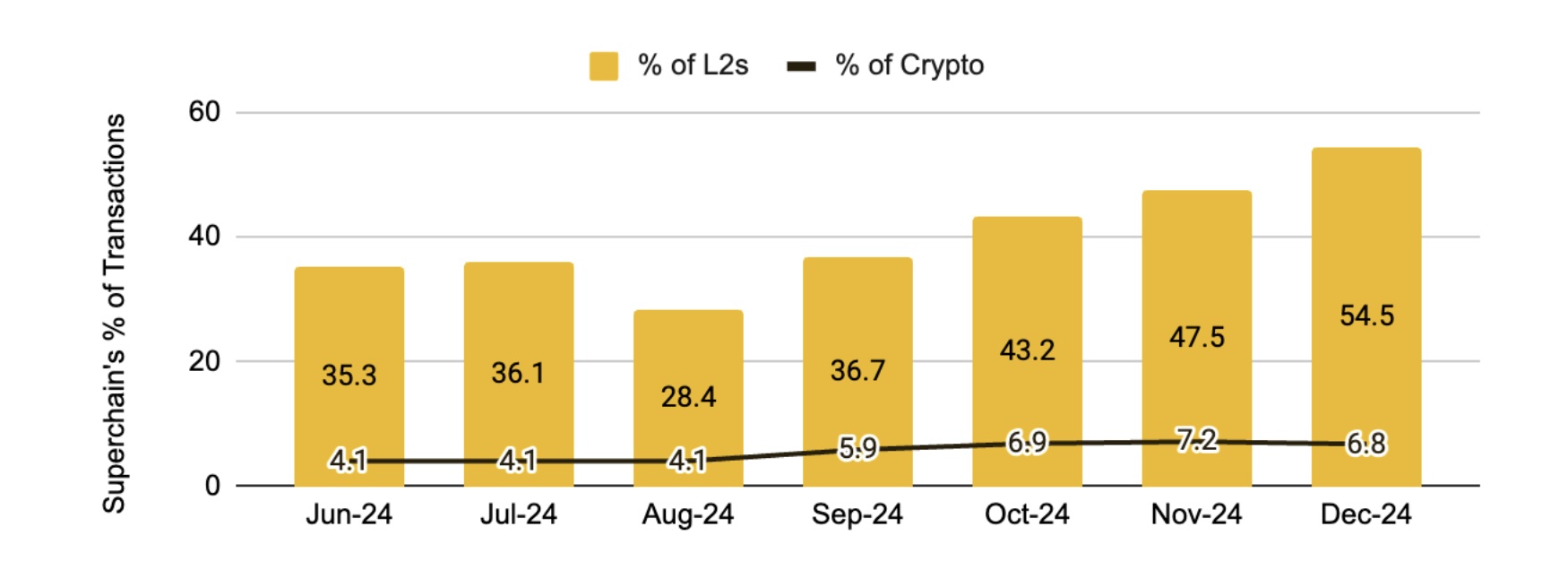

The Optimism Superchain has been gaining significant traction in terms of attracting new users and retail activity. Across the second half of 2024, it has been the source of a large proportion of the total crypto transactions, accounting for ~54% of the total L2 transactions, and ~6.8% of the total crypto transactions in December 2024.

Figure 42: The Optimism Superchain was responsible for 54.5% of total L2 transactions and 6.8% of total crypto transactions in December 2024

Overall, the OP Superchain has experienced tremendous growth in terms of usage in 2024, driven in large part by the success of the Base L2. On top of the increased activity on existing OP Stack chains, it was also a huge year in terms of the number of new L2s added to the Superchain.

The OP tech stack continues to be adopted by companies, both crypto-native and otherwise, looking to launch their own L2s. Two major Superchain L2s to look out for are:

Unichain – developed by the team behind Uniswap, Unichain is a DeFi-native Ethereum L2, optimized to be the home for liquidity across chains. The team has announced plans to launch mainnet in early 2025.

Soneium – on August 28, Sony Block Solutions Labs (Sony BSL) launched the Soneium Minato public testnet and the Soneium Spark incubator. The L2 Soneium

The Zero-Knowledge Rollups

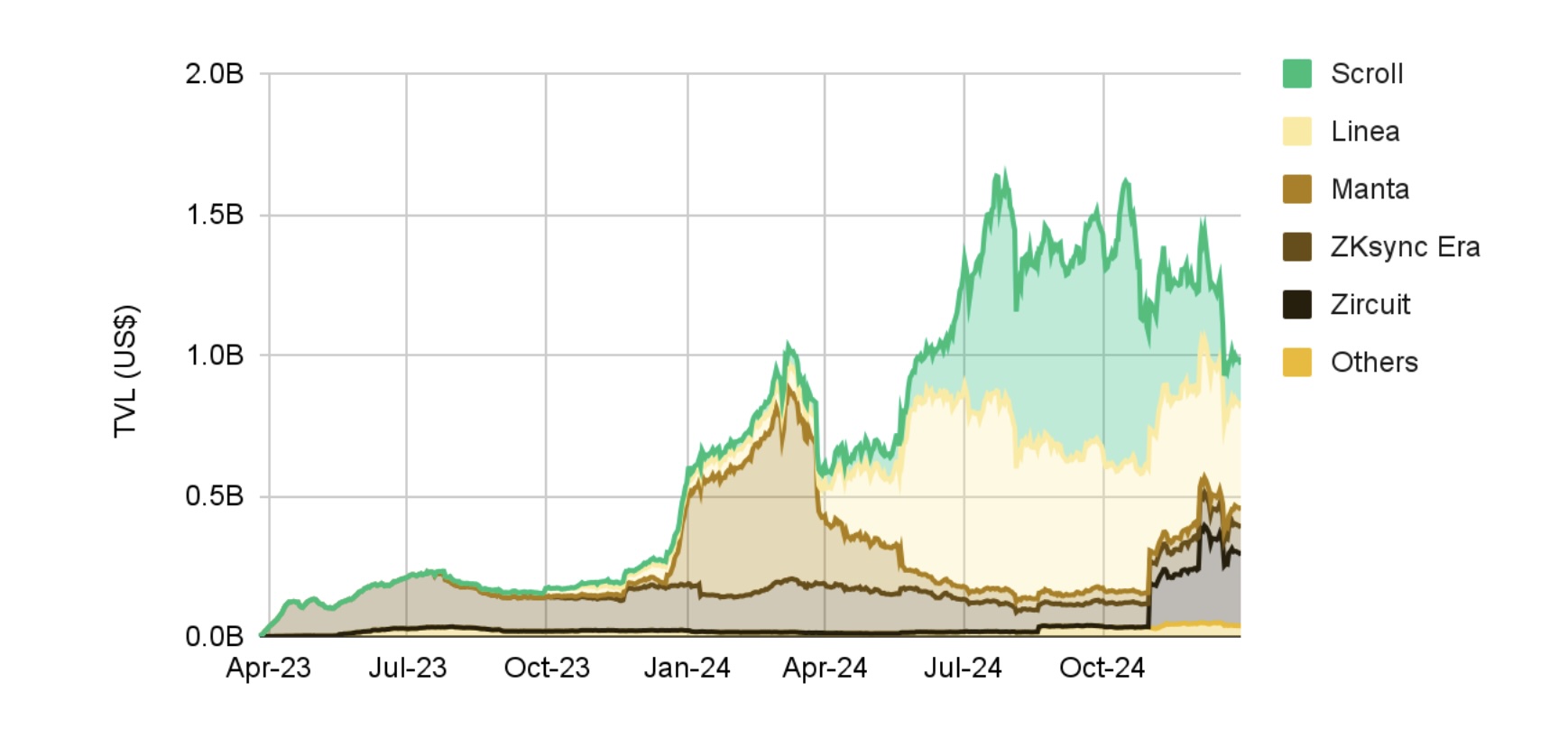

In Q2 and Q3 of 2024, ZK rollups saw a significant uptick in TVL, driven largely by the slew of airdrop campaigns. As the airdrop farming fervor cooled however, we saw capital flow out from the ZK rollups, bringing their total TVL down over 50% from its peak of US$2.1B to US$1.1B.

Figure 44: TVL across ZK rollups peaked at ~US$1.6B in July, before retracing to ~US$1B as of December 2024

zkSync Era

Matter Labs, the developer of the ZKsync layer-2 network, introduced the ‘Elastic Chain’ in July as part of its ZKsync 3.0 roadmap. Similar to Polygon’s AggLayer, which was announced in January 2024, the Elastic Chain aims to unify custom blockchains created with the ZK Stack toolkit , providing a seamless user experience akin to a single chain.

Having debuted June 2024, the Elastic Chain is seemingly off to a good start. We saw a number of notable projects choose to make use of the ZK tech stack to launch their own L2s over the course of the year.

Deutsche Bank (Project Dama) – In December, the Germany-based global MNC Deutsche Bank announced its intention to develop a public and permissioned Ethereum L2, leveraging the ZKsync technology stack. This move is part of Deutsche Bank’s effort to enhance efficiency and cost savings in regulated financial services while tackling privacy and transaction challenges.

Abstract chain – Scheduled to launch its mainnet in Jan 2025, Abstract chain is coming hot on the heels of the hype around the Pudgy Penguins ecosystem, which just launched its $PENGU token airdrop on December 17. Abstract is co-built by Igloo Inc., the parent company of the Pudgy Penguins NFT project. Abstract chain intends to be a consumer crypto chain, featuring native account abstraction, aimed to provide a seamless end user experience.

Treasure L2 Chain – TreasureDAO, previously an Arbitrum-based gaming platform, launched its Treasure L2 mainnet using the ZKsync tech stack in December 2024.

Cronos zkEVM – First chain (after ZKsync Era) to go live as part of the ZKsync Elastic Chain, launched mainnet in August.

Lens – Slated to launch in early 2025, the team behind social network protocol Lens is partnering with the team behind Aave, Avara, to design the new ZK L2 to cater to SocialFi applications, incorporating customisable features like accounts, usernames, graphs, feeds, and groups.

Polygon Agglayer

In January 2024, the Polygon team introduced AggLayer. AggLayer integrates fragmented blockchains into a cohesive network of ZK-secured L1 and L2 chains, functioning as a single chain. It aggregates ZK proofs from all connected chains, unifies liquidity and assets across multiple chains in a seamless manner, and ensures secure, near-instant cross-chain transactions.

In a December blogpost, Agglayer announced its intentions to focus on four specific verticals:

DeFi – AggLayer aggregates liquidity across blockchains, eliminating the need for developers to deploy on multiple chains, split liquidity, create new liquidity for each wrapped token, and use bridges. This introduces expanded design spaces for developers to build unified DeFi solutions.

Gaming – Agglayer will allow gamers to avoid being locked into a single chain. Connections will include Ronin, Immutable, Moonveil, Wilder World, and others. The launch of the Immutable zkEVM gaming-purpose chain was a notable development on this front in 2024.

RWA – AggLayer simplifies integration between disparate RWA systems, creating a unified environment and enabling a true market for RWAs.

AI + DePIN – Easier integrations and improved cross-chain data sharing enable seamless AI system collaboration across platforms. Built-in security mechanisms ensure trust, while enhanced interoperability accelerates innovation.

On December 20, 2024, AggLayer launched its testnet v0.2 to stress-test pessimistic proofs. With the mainnet launch anticipated in early 2025, competition within the ZK rollup ecosystem could begin to intensify . This could potentially lead to a duopoly between AggLayer and ZKsync Era, reminiscent of the competitive dynamic between Arbitrum and OP Stack in the optimistic rollup space.

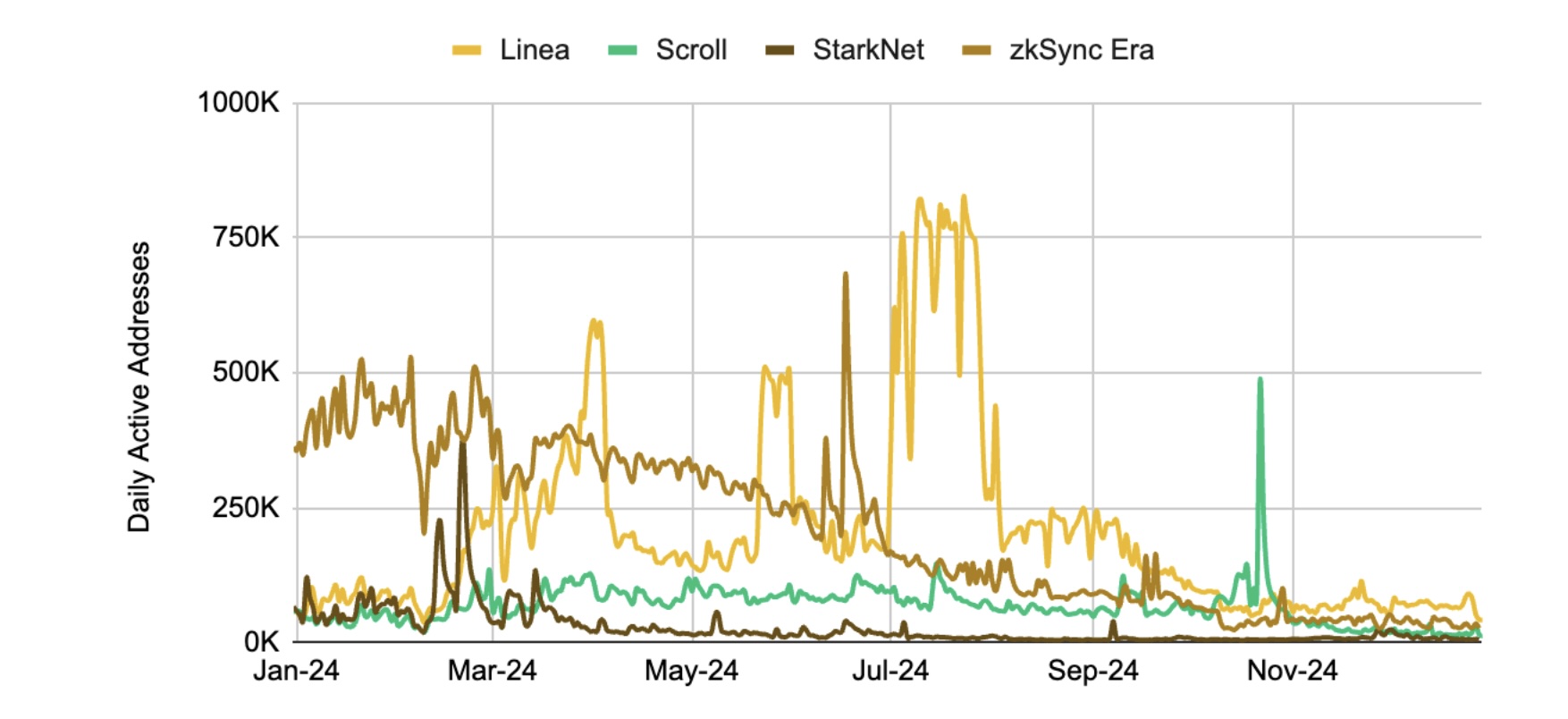

Linea

In November, the Consensys-backed L2 announced plans to launch its LINEA token in Q1 2025. This would make it the final major ZK rollup to launch a token in the foreseeable future, following the likes of competitors like Manta, ZKsync Era, StarkNet, and Scroll, which all launched their tokens in 2024.

Against the backdrop of the Linea token airdrop purportedly coming in early 2025, the chain currently holds the number one spot in terms of DeFi TVL among ZK rollups at over US$360M. Although its daily active address count has declined significantly from its peak in July of 796K, Linea retains the highest daily active addresses amongst the ZK rollups at just over 41K.

Figure 45: Linea retains the highest daily active addresses amongst ZK competitors, at just over 41K as of December 2024

In October 2024, the Linea team reaffirmed its commitment to decentralizing the protocol with a proposal titled “Towards Linea’s Decentralization.” This proposal outlines a plan to transition the zkEVM to a permissionless system and establish decentralized governance by changing the current block validation, block proposal, and finalization processes.

Monitoring the adoption rate of the Linea L2 in 2025, along with its competition with other L2 solutions, could offer early insights into how the market evaluates different decentralization strategies. The decentralization of the L2 sequencer, in particular, has been a prominent topic of discussion within the Ethereum community in 2024.

Decentralized Finance

The Big Picture

The past year marked a renaissance for Decentralized Finance (DeFi), proving largely positive compared to previous years. While some sub-sectors stagnated and certain metrics lagged, others broke records, showcasing DeFi’s importance as a core growth driver for the industry. The biggest gain came from a broadening market base, fueled by new on-chain products, nascent narratives, diversity across chains, and the prospect of a more favorable regulatory environment post-U.S. election — leaving plenty to anticipate in the new year.

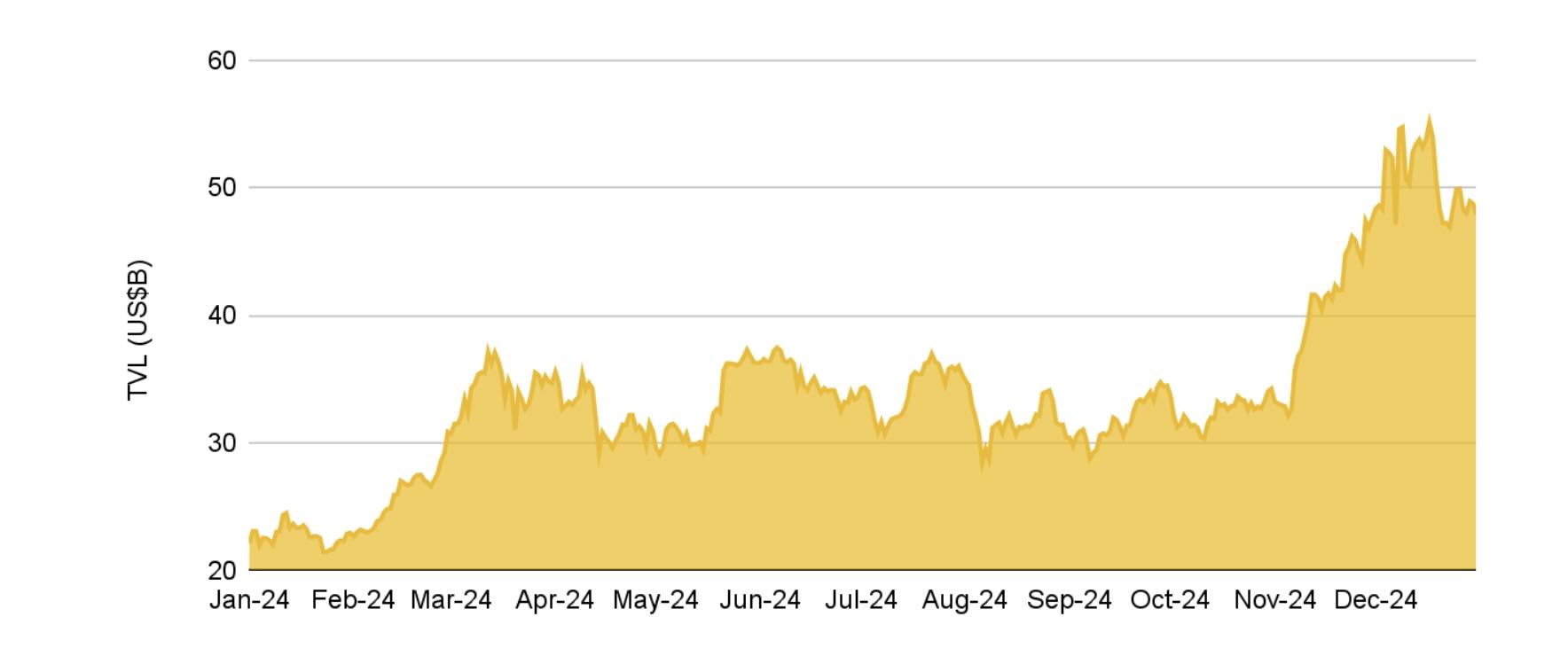

Accompanying these trends was a notable influx of capital into DeFi. With 2024 ushering in bullish market conditions, increased user activity, and stronger investor appetite, total value locked (TVL) surged to US$119.3B from US$54.3B, representing a strong 119.7% year-to-date (YTD) gain.

Figure 46: DeFi TVL surged 119.7% in 2024, reaching US$119.3B

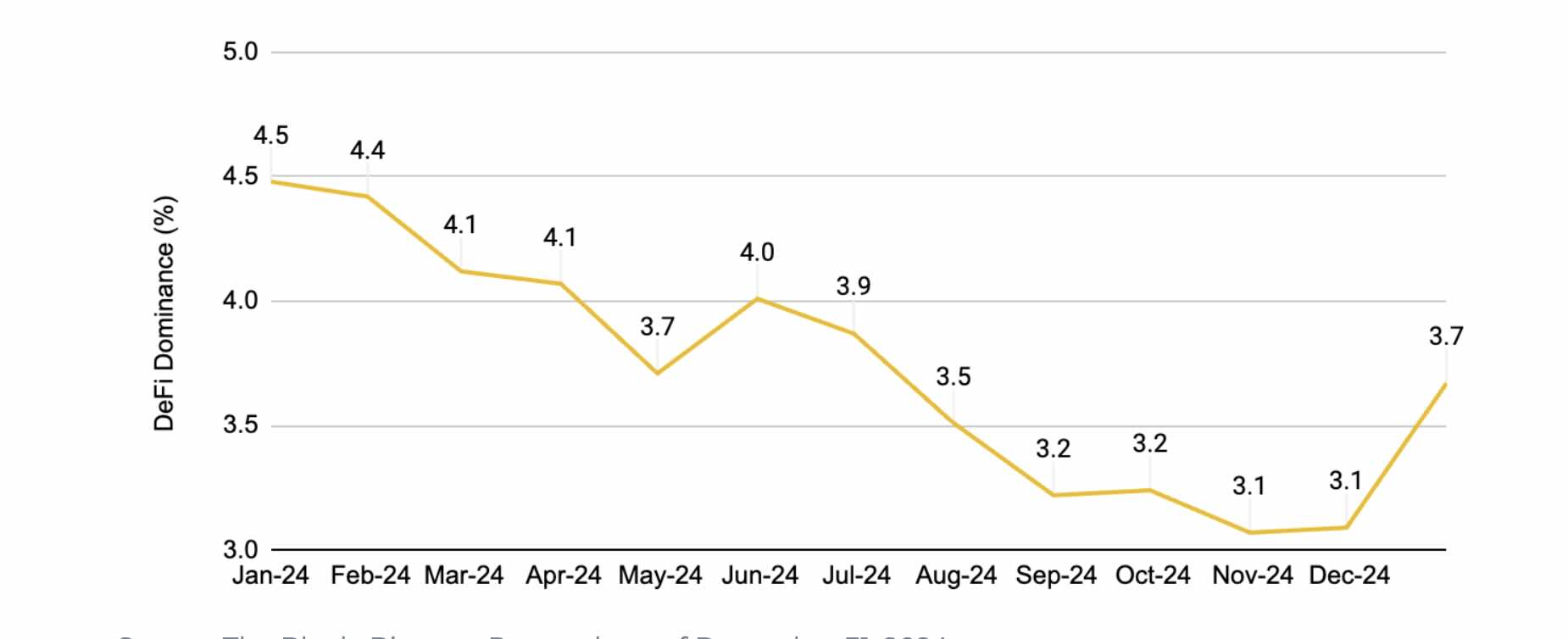

However, DeFi Dominance — which measures DeFi’s share of the global crypto market cap — presents a different picture, slipping from 4.5% to 3.7% despite a brief reversal following the U.S. election in November 2024. Over the course of the year, it declined by 0.8% in absolute terms. While the sector has attracted substantial capital inflows, DeFi’s public market valuations still trail the broader crypto market, indicating room for further growth. This also suggests that investors may be focusing on select DeFi niches or directing their capital to other areas of the crypto ecosystem.

Figure 47: Despite a reversal in November, DeFi dominance posted a 0.8% decline in absolute terms for 2024

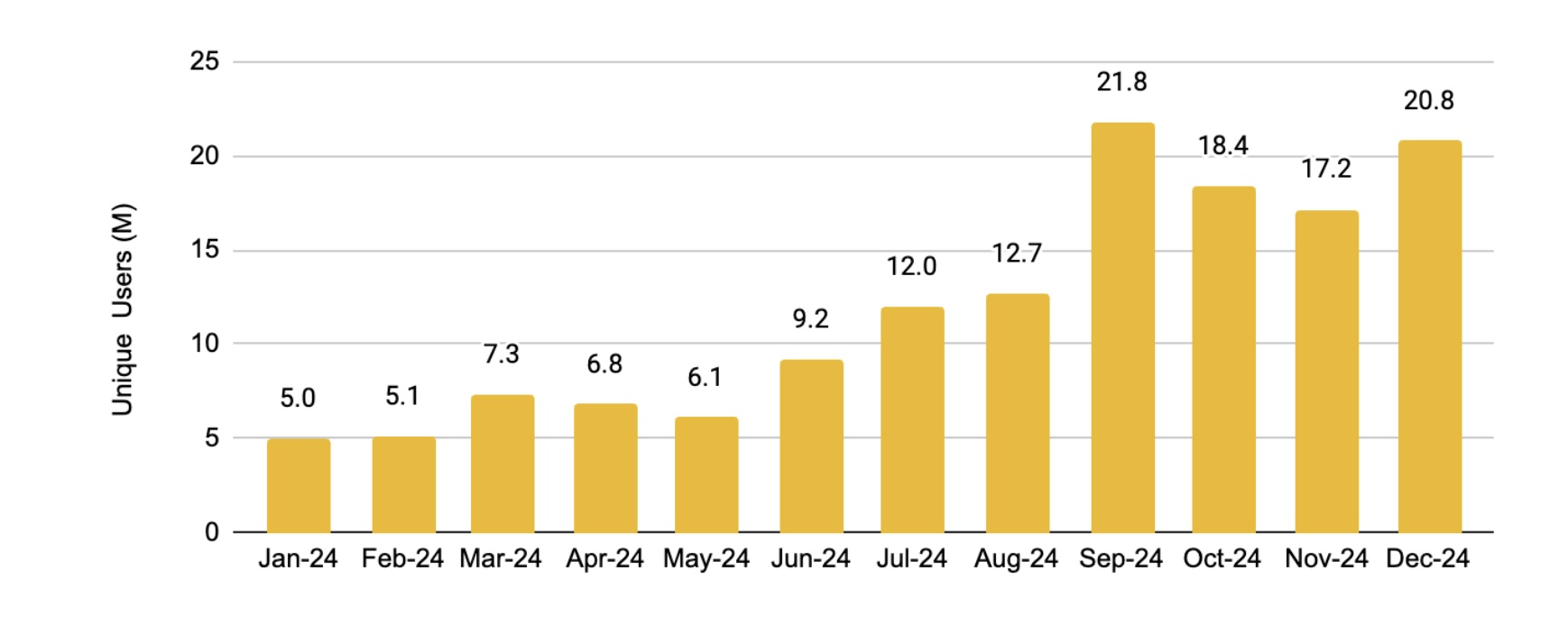

In terms of user adoption, DeFi remains a primary gateway for newcomers on-chain, with the average number of unique monthly users jumping from 5.0M to 20.8M over the past year. While this growth is impressive, airdrops from notable blue-chip DeFi projects have played a role in boosting these figures. Nonetheless, monthly unique users have consistently hit new all-time highs throughout 2024, underscoring the sector’s continued strong engagement.

Figure 48: Unique monthly users across DeFi protocols soared by 314.6% in 2024

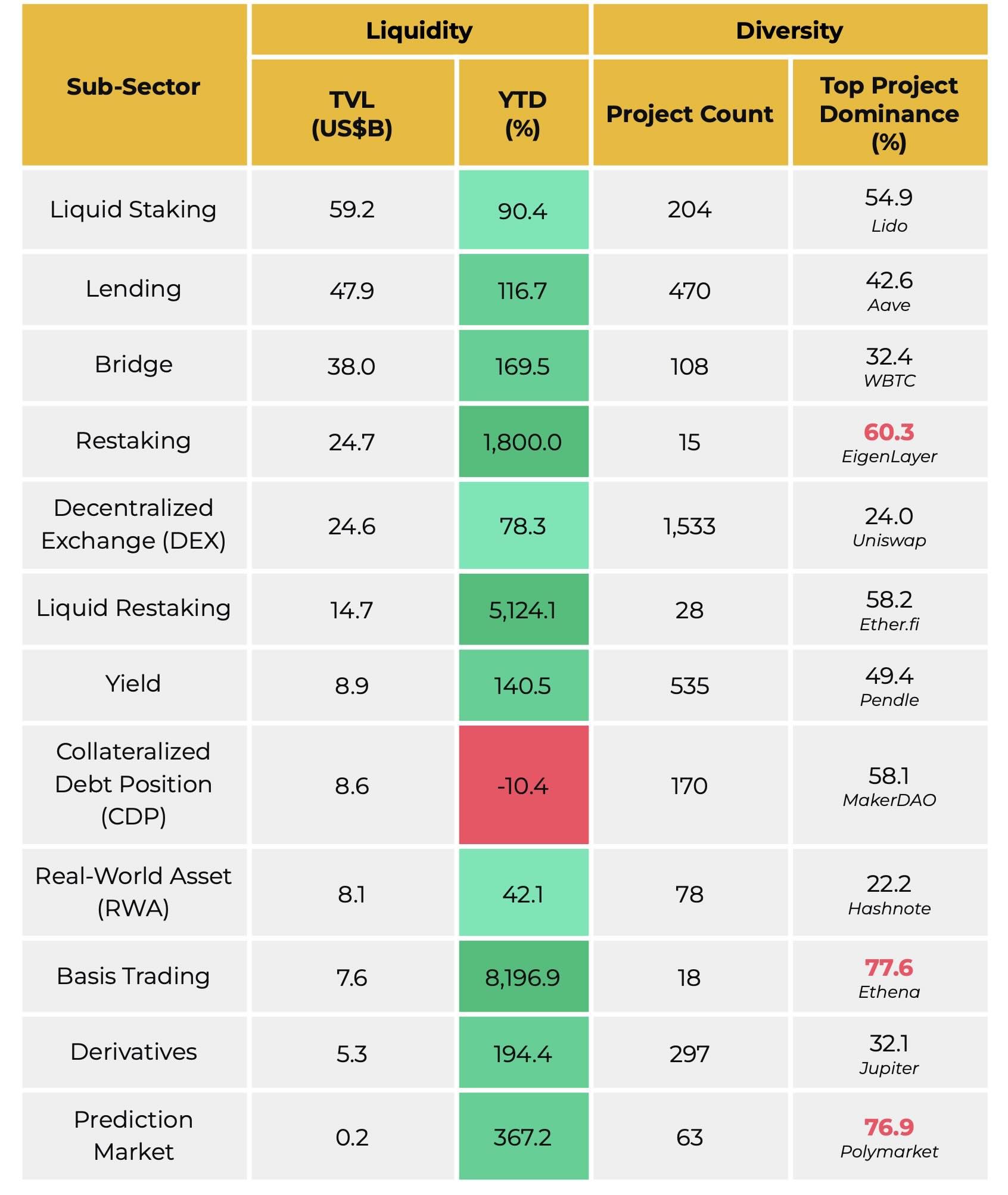

Breaking this down by sub-sector, this year’s capital influx has reached well beyond the traditionally dominant categories, reshaping market dynamics. An analysis of capital distribution reveals significant growth across nearly all DeFi sub-sectors, with particularly large gains in 2024 in emerging areas like Restaking and Basis Trading. Liquid Staking continues to hold the top spot by TVL, followed by Lending, Bridge, Restaking and Decentralized Exchanges (DEXes). Sub-sector diversity has also expanded overall, creating a more competitive on-chain environment. Among these sub-sectors, DEXes boast the highest number of protocols, underscoring their critical role in driving liquidity throughout DeFi markets.

Figure 49: Every major DeFi sub-sector recorded a notable influx of capital in 2024

Sub-Sector Spotlight

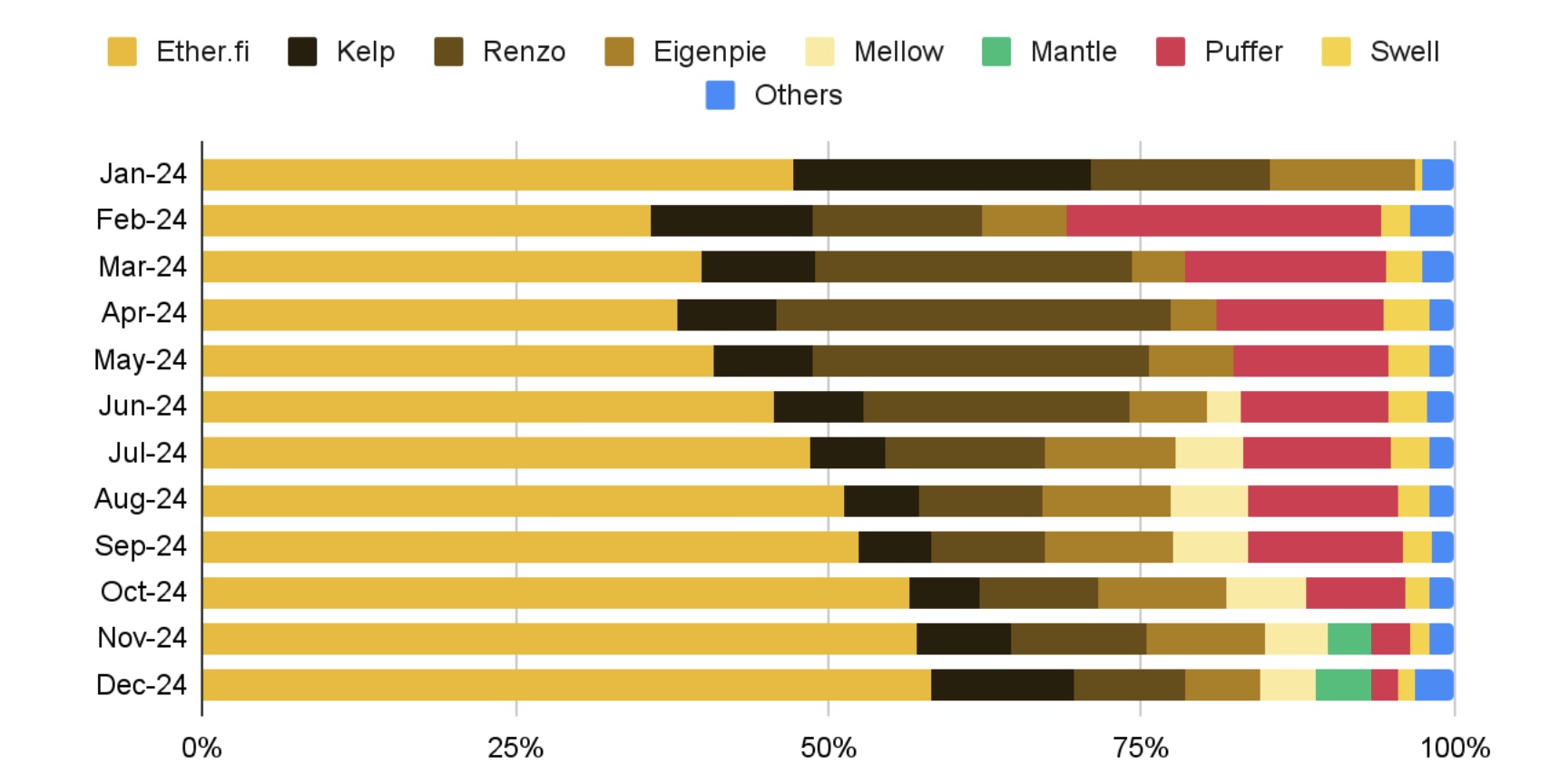

Liquid Staking, Restaking and More

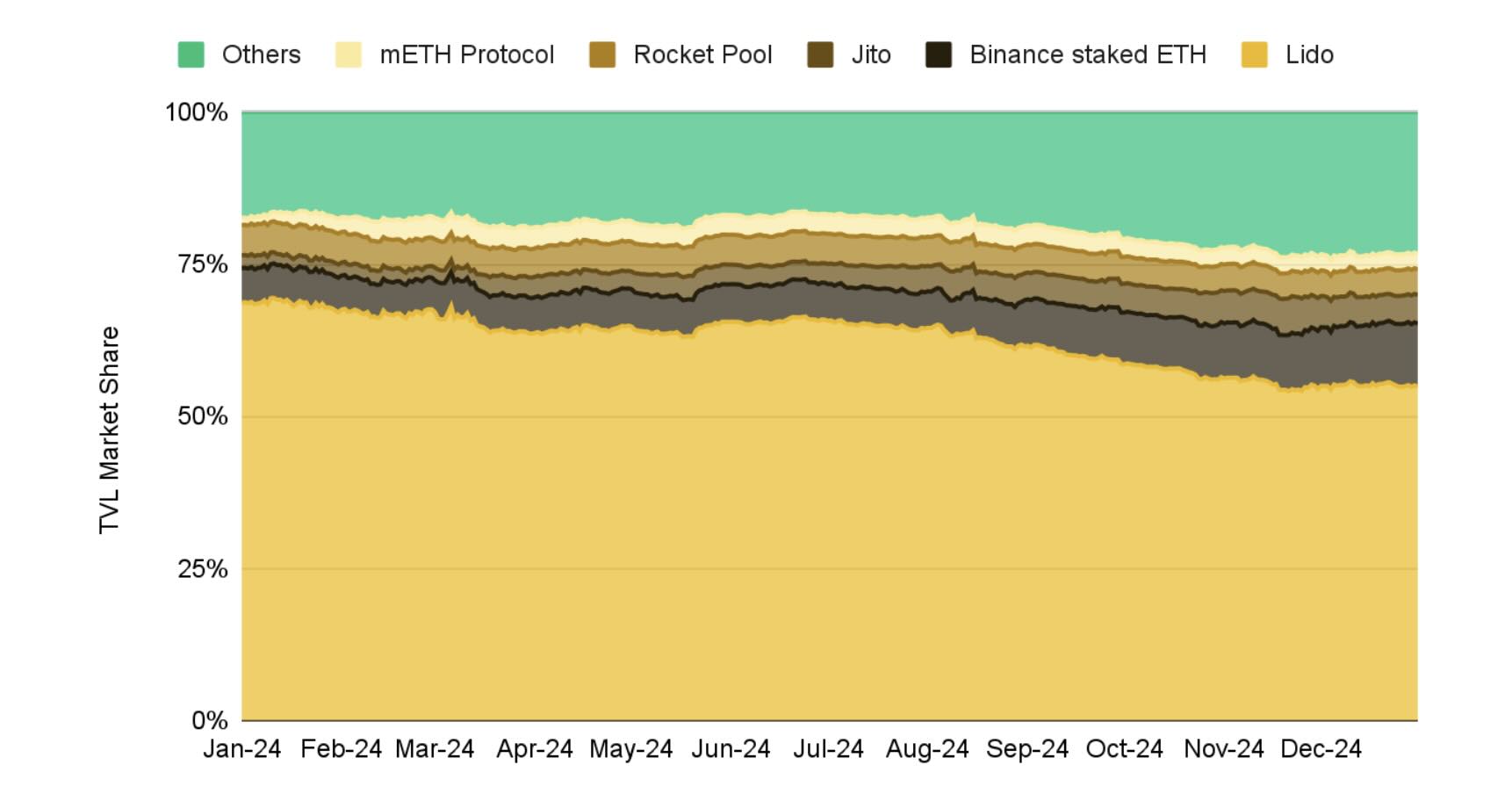

Liquid staking remains the largest sub-sector in DeFi by TVL, with Lido maintaining its position as the market leader. While Lido’s TVL grew by 52.1% YTD, its dominance has experienced a modest decline over the past year. These shifts in market share are primarily driven by staking derivatives expanding to other blockchains — Jito on Solana, for example, recorded a 329.5% YTD growth in TVL — and the emergence of new sub-sectors like restaking and liquid restaking, which provide alternative ways to stake ETH. These developments, combined with the push to decentralize Ethereum’s staking infrastructure, are actively reshaping the liquid staking market.

Figure 50: While still the largest, Lido has seen its market share decline from 68.4% to 54.9% as multiple competing forces emerge

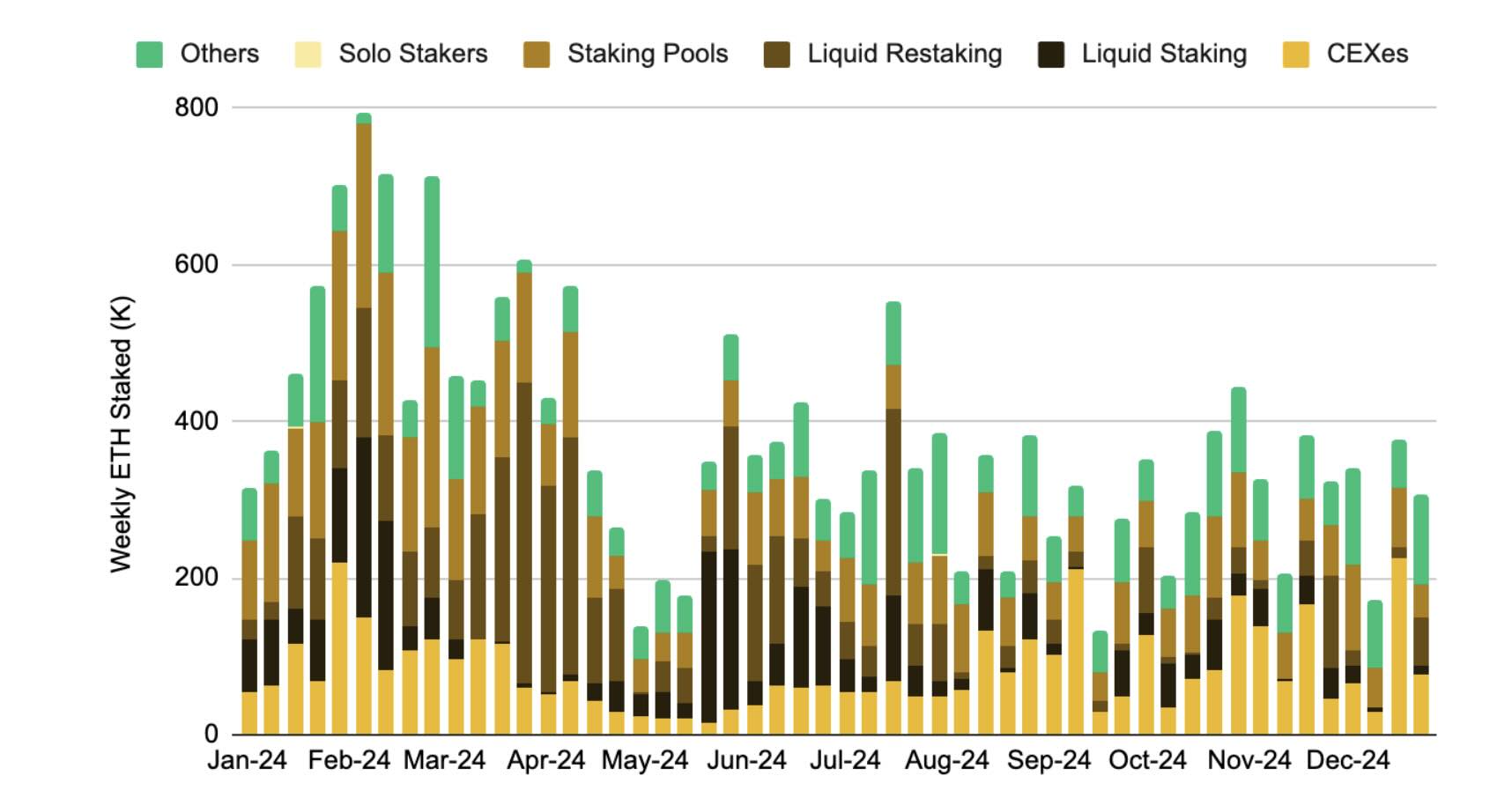

While established protocols like Lido have yet to face significant competition threatening their dominance, the advent of restaking has introduced new competitive pressures from an adjacent sub-sector. Users now have access to multiple layers of Ethereum’s staking ecosystem through various platforms, often accompanied by the prospect of higher yields. The growing interplay between liquid staking and restaking will be a key area of interest in the evolution of the staking derivatives market.

Figure 51: Several alternative and attractive sources for staking ETH, beyond liquid staking, gained traction in 2024

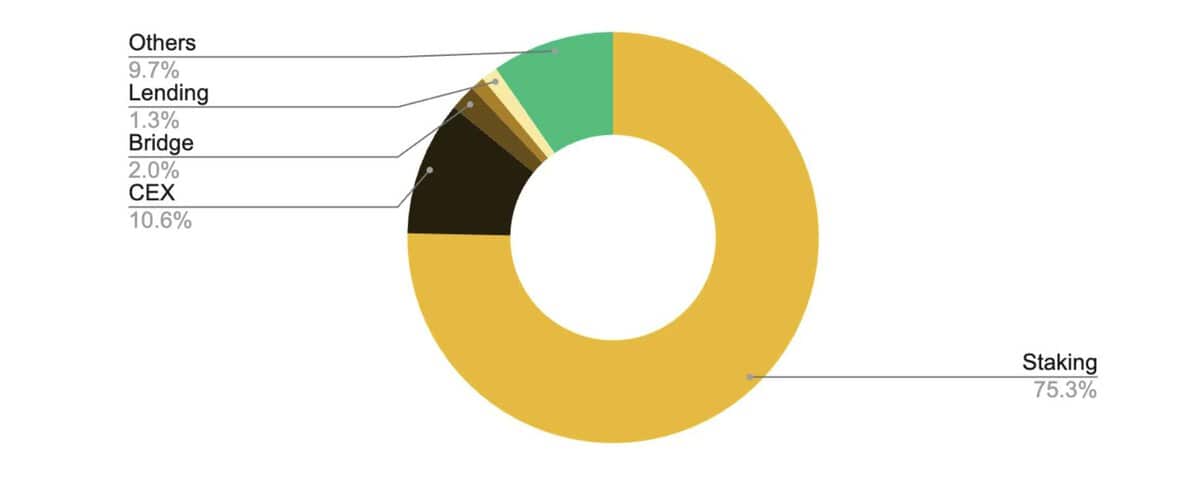

Restaking emerged in 2024 as an innovative method for rehypothecating staked ETH collateral. By allowing staked ETH to secure multiple decentralized infrastructures simultaneously through Proof-of-Stake (PoS), restaking introduced a novel approach to bootstrapping network security while maximizing on-chain yield. Leading the restaking space is EigenLayer, starting the year with US$1.3B in TVL — primarily in liquid staked ETH — and reaching over US$20B at its peak. Although TVL has since declined to US$14.9B, likely due to capital outflows following a retroactive airdrop announcement, EigenLayer remains the third-largest DeFi protocol by TVL, behind only Lido and Aave.

The growth of EigenLayer has paved the way for broader developments in the restaking ecosystem. Emerging protocols like the Paradigm-backed Symbiotic and Karak have started to challenge EigenLayer’s dominance, though currently on a smaller scale. This diversification is widely viewed as a positive step, decentralizing a market fundamentally tied to network security and fostering competition that could drive further innovation within Ethereum’s restaking layer. Moreover, the concept of restaking is expanding beyond Ethereum. For instance, Babylon has become the largest Bitcoin-based restaking protocol, amassing US$5.3B in TVL. Collectively, these developments underscore the underlying demand for on-chain yield generation through shared crypto-economic security .

Figure 52: While EigenLayer has maintained dominance in the restaking space, market share is gradually diversifying, extending to other networks

Despite attracting this TVL growth, restaking remains a relatively nascent sub-sector, with room to develop as the ecosystem matures. Most projects are still in their early stages and not fully operational, with only a few Actively Validated Services (AVSs) showing tangible progress in use cases such as oracles, data availability (DA), shared sequencing, and cross-chain messaging. The services secured by restaking are largely still under development and currently do not generate meaningful yield.

The long-term demand for restaking will ultimately depend on whether the opportunity costs and the additional real yield these services eventually produce justify their associated risks. This balance will be critical in determining the sustained growth and viability of restaking as it evolves.